Hi people. I know there is already a sticky of this topic but I was thinking of gathering all the info and compiling it all into 1 so that it is easier to check the rates.

So Lets get started.

CHOOSING THE IDEAL LOAN

There are hundreds of different loan packages out there that offers different rates and different features. Therefore, when choosing a home loan package the 1st question that pops up in your head should not be:

"Which bank offers the lowest interest rate?"

Interest rate should not influence you so much to the extend that you do not consider other factors. The 1st question that you should ask is:

"Which bank can offer me a good loan package under these circumstances?"

Reason why I would advise such is:

1. Service is just as important.

You can choose the best rate in town but if the person serving you is lazy or rude or with an attitude, your loan will most probably get delayed as the staff might have pushed your loan application aside/ When there is something wrong with the loan eg: the loan package that you got is not the one you requested, you can't find or call the person that served you... Actually there's thousand and 1 things that can happen so even if the rates is BLR0.05% better than another bank, I'd rather pay abit for the good service.

2. Are you a risk taker

There are 2 different types of rate that I can think of:

a) Fixed rate

Fixed rate have higher BLR. This is more for those that are risk adverse. Reason is that BLR can fluctuate. Within your 30 years tenure, BLR can shoot up to as high as 12.77% (the highest it went back in 1997).

:: ProsWhen interest rates rise, your repayments won’t

:: ConsIf interest rates fall, your repayments won’t

Restrictions on prepayments

No redrawing permitted

b) Variable rate

Variable rate has a lower BLR and this are more for people who are willing to take a bit of risk as nobody can predict what the BLR would be in the coming years. Great example would be the latest decrease in BLR. What was predicted before BLR went down was that it would go up to 7% but instead.. it went down.

:: ProsWhen interest rates fall, repayments fall

You enjoy very low interest rates during the initial years

May allow prepayments (subject to conditions)

May have redrawing features (subject to conditions)

:: Cons When interest rates rise, so do your repayments

3. Xtra charges

Certain banks have hidden cost or extra charge. So remember to ask again and again what charges they have. Eg: Some banks will charge you for every transaction you make. So be xtra careful on that.

Another one would be the "ZERO COST" packages. Do ask the sales staff if all legal fees, stamp duty and valuation fee will be fully absorbed by the bank. Eg: Certain banks will state that it is zero cost however you have to pay 0.5% of the legal fee

or it could be free legal documentation but you have to pay for valuation fee.

4. Term Loan or Flexi Loan

a) Term loan

May offer you the best rate but keep in mind that if you want to pay xtra to clear off your principal, you have to inform the bank in advance. Any xtra payment that you make, you cannot request to withdraw it.

b) Flexi Loan

With the current account, you can deposit money in as a payment for our principal which will help you reduce the interest AND you have the option to withdraw the money at anytime. There are certain banks that has add on features that can link your loan to your savings and offers you additional bonus credit to offset your loan.

Note: Usually there is a set up fee of RM200 and maintenance fee of RM10-RM15 depending on the bank. That's another thing that you should check.

These are a few that I can think about at the moment. Any xtra help would be much appreciated.

Added on December 12, 2008, 11:55 amDOCUMENTATIONGeneral documents to be prepared.

1) Photocopy of IC

2) Land Title/ S&P

3) Latest 3 months salary slip

4) Latest Bank statment that your salary is credited into

5) BE form & tax receipt

6) Any fixed deposit/ addtional savings you have frm other banks

7) Loan statement (for refinancing cases)

8) Borang A & D (for sole proprietor & partneship- self employed)

9) Borang 24 & 49 (for companies- self employed)

10) 6 months current account (for self employed)

These are the documents that are normally required depending on different circumstances. So you can be prepared. Any bankers around that wants to add on?

There is no harm applying with a few banks as the rates shown are Board Rates which can be negotiated. It is all subjected to management approval

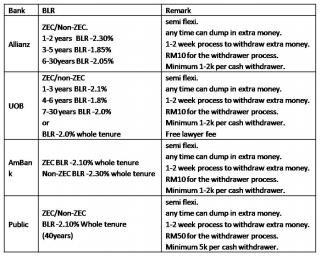

Added on December 12, 2008, 12:00 pmPUBLIC BANKPublic Home PlanZERO COST PACKAGE (ZC)Normal Term Loan PackageLoan Amount :150k - 350k

Interest: BLR-2.0 Whole Tenure

Loan Amount :350k - 500k

Interest: BLR-2.1

Loan Amount :>500k

Interest: BLR-2.2

Full Flexi Package*

Loan Amount :200k - 400k

Interest: BLR-2.0 Whole Tenure

Loan Amount :400k - 500k

Interest: BLR-2.1

Loan Amount >500k

Interest: BLR-2.2

* Take note of this. I have checked with public bank but this is not the rate. For their flexi loan Package, the rate is higher. Any PB banker here please clarify on this. Or is this NON ZERO COST (NZC)?

Public Bank Commercial PlanLoan Amount :200k - 300k

Interest: BLR-1.5 Whole Tenure

Loan Amount :300k - 400k

Interest: BLR-1.6 Whole Tenure

Loan Amount : > 400k

Interest: BLR-1.7 Whole Tenure

Person to contact: HK Law

H/P number: 0166199989

Added on December 12, 2008, 12:14 pmCIMB BANKZERO COST PACKAGE (ZC)Flexi Home Loan PackageLoan Amount : < RM300k

Interest:

Under Construction - BLR-1.65% Whole Tenure

Completed - BLR-1.75% Whole Tenure

Loan Amount : >RM300k, <RM500k

Interest:

Under Construction - BLR-1.75% Whole Tenure

Completed - BLR-1.85% Whole Tenure

Loan Amount >500k

Interest:

Under Construction - BLR-1.85% Whole Tenure

Completed - BLR-1.95% Whole Tenure

Additional BLR-0.1% for MRTA

NON ZERO COST PACKAGE (ZC)Flexi Home Loan PackageLoan Amount : < RM300k

Interest:

Under Construction - BLR-1.85% Whole Tenure

Completed - BLR-1.95% Whole Tenure

Loan Amount : >RM300k, <RM500k

Interest:

Under Construction - BLR-1.95% Whole Tenure

Completed - BLR-2.05% Whole Tenure

Loan Amount >500k

Interest:

Under Construction - BLR-2.05% Whole Tenure

Completed - BLR-2.15% Whole Tenure

Additional BLR-0.1% for MRTA

Person to contact: Can contact me and I'll look for a CIMB banker for you

H/P number: 0123871138

Added on December 12, 2008, 12:25 pmEON BANKZERO COST PACKAGE (ZC)Loan Amount : > RM200k

Interest:

Completed - BLR-2.2%- 2.3% Whole Tenure

Note:

1. This is not a completely zero cost package. Customer will have to bear 0.5% of the legal fees.

2. I need someone to confirm if it is a flexi package or term loan as I'm getting 2 diff answers frm 2 diff staff.

For those who wants their penalty fees up to 3% absorbed as well:

Interest: 1st 8 years - BLR-1.6%

Thereafter - BLR-2.4%

Lock-in-period = 8 years

Added on December 12, 2008, 12:40 pmPRICE SOLUTION (subgroup of Std Chartered Bank)Mortgage One (flexi)ZERO COST PACKAGE Under Construction

1st to 5th year: BLR-1.6%

Thereafter: BLR -2.00%

Completed

1st to 5th year: BLR-1.65%

Thereafter: BLR -2.00%

NON ZERO COST PACKAGE (NZC)Under Construction

BLR-2.00% Whole Tenure

Completed

BLR-2.00% Whole Tenure

Rates are negotiable

Person to contact: Can contact me and I'll look for a PS banker for you

H/P number: 0123871138

Added on December 12, 2008, 12:47 pmUNITED OVERSEAS BANKINTELLIGENT HOME LOAN ( i H L )NON ZERO COSTUnder Construction < 40%

1st year: 0%

2nd year onwards: BLR -1.60

Under Construction

1st - 3rd year: BLR -2.00

4rd year onwards: BLR -1.60

ZERO COSTUnder Construction or Completed

Whole Tenure: BLR -1.75

MRTA:

MRTA can register 1 person name only although house owner have 2 person...

the loan amount 100% bear on 1 person that registered...

Person to contact: Wayne

H/P number: 012- 517 1210

Added on December 12, 2008, 1:04 pmHONG LEONG BANKIf I'm not mistaken this is term loan

NON ZERO COSTUnder Construction

1st year: 2.38%net

2nd year onwards: BLR 2.88%net

thereafter:-1.30%(with MDTA)

ZERO COSTUnder Construction

1st year: 2.88%net

2nd year onwards: 3.88%net

thereafter:-1.30(with MDTA)

Person to contact: JohnChew2002@hotmail.com/ Me!!

H/P number: 012-2498060/ 012-3871138

This post has been edited by DriedIce: Dec 29 2008, 10:30 PM

May 22 2008, 08:54 AM, updated 15y ago

May 22 2008, 08:54 AM, updated 15y ago

Quote

Quote

This applies to cc as well.

This applies to cc as well.

0.2873sec

0.2873sec

0.55

0.55

6 queries

6 queries

GZIP Disabled

GZIP Disabled