QUOTE(AIYH @ Feb 12 2017, 10:41 PM)

Prehaps you could share where do you stuck in analyzing?

You could start with recommended funds and portfolio

You could also use fund selector and chart center to pick funds based on their RRR within their asset class, region and sector

You could also just tailgate

xuzen or other sifu portfolio, subscribe to them for their kind public analysis

Sounds good, I like to analyse myself , I have already been through spoonfed education system, don't want to be spoonfed personal finance..( well spoonfeed a bit also can la, but too much hand holding--> dependent on others). Thanks ya!

QUOTE(skynode @ Feb 12 2017, 11:39 PM)

I ain't expert but I'm emulating FSM recommended Aggressive portfolio. Not the entire portfolio though. Swapped a couple of funds according to my belief and risk appetite. Ultimately, no one knows what would happen in the future. No point timing the market. Just stay invested and top up regularly with value-cost averaging. Buy at a discount whenever possible. This is what I believe in.

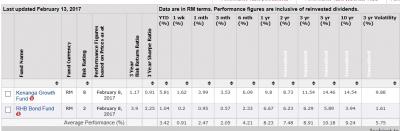

QUOTE(Ramjade @ Feb 13 2017, 07:46 AM)

You look at the following:

(i) can it beat the benchmark? (over min 3 years period)

- If yes why? Is the fund good or because of exchange rate?

(ii) compare it with it's peers (other funds which invest in the same region)

- Did it beat them? (over min 3 years period)

- If no, better pick the winning team

(iii) Choose returns/stability

Good questions! Thanks ya!

QUOTE(xuzen @ Feb 13 2017, 10:27 AM)

Where got so many variables?

Only need to know the following parameters only, that is:

Return of Investment (1),

Standard Deviation of Mean (2),

Correlation Coefficient ratio (3),

Forward Price earning ratio of benchmark (4),

Four variables only .... mah!

Xuzen

Ugh I though need to look at the fund manager etc etc

went through the whole prospectus also

Back to the drawingboard for me then.. Thanks!

Feb 13 2017, 09:34 AM

Feb 13 2017, 09:34 AM

this may not be him...

this may not be him...

Quote

Quote

)

)

0.0199sec

0.0199sec

0.51

0.51

6 queries

6 queries

GZIP Disabled

GZIP Disabled