Dec 31 2019, 09:10 AM, updated 3y ago

Dec 31 2019, 09:10 AM, updated 3y ago

| No. | Licensed Insurance Companies | Category of License, Approval, or Registration |

| 1 | AIA Berhad | Life Insurance Business |

| 2 | AIG Malaysia Insurance Berhad | General Insurance Business |

| 3 | Allianz Life Insurance Malaysia Berhad | Life Insurance Business |

| 4 | AmMetLife Insurance Berhad | Life Insurance Business |

| 5 | Berjaya Sompo Insurance Berhad | General Insurance Business |

| 6 | Chubb Insurance Malaysia Berhad | General Insurance Business |

| 7 | Etiqa Life Insurance Berhad | Life Insurance Business |

| 8 | FWD Insurance Berhad (formerly known as Gibraltar BSN Life Bhd) | Life Insurance Business |

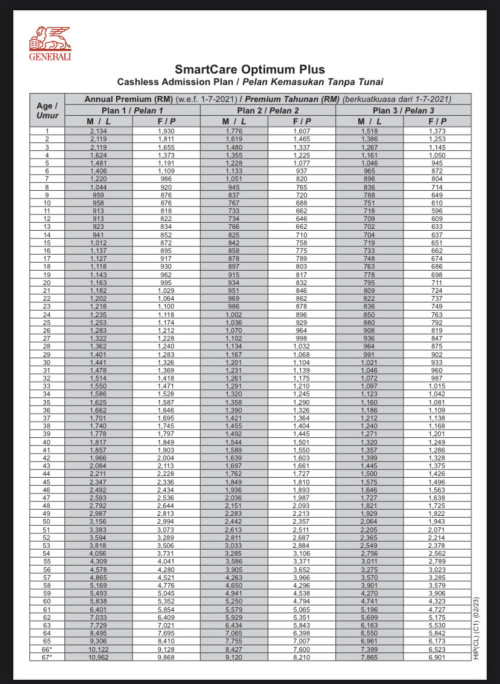

| 9 | Generali Life Insurance Malaysia Berhad (formerly AXA Affin Life) | Life Insurance Business |

| 10 | Great Eastern Life Assurance (Malaysia) Berhad | Life Insurance Business |

| 11 | Hong Leong Assurance Berhad | Life Insurance Business |

| 12 | Liberty General Insurance Berhad (formerly AmGeneral Insurance) | General Insurance Business |

| 13 | Lonpac Insurance Berhad | General Insurance Business |

| 14 | Manulife Insurance Berhad | Life Insurance Business |

| 15 | MCIS Insurance Berhad | Life Insurance Business |

| 16 | MSIG Insurance (Malaysia) Bhd | General Insurance Business |

| 17 | Pacific & Orient Insurance Co. Berhad | General Insurance Business |

| 18 | Pacific Insurance Berhad | General Insurance Business |

| 19 | Progressive Insurance Berhad | General Insurance Business |

| 20 | Prudential Assurance Malaysia Berhad | Life Insurance Business |

| 21 | QBE Insurance (Malaysia) Berhad | General Insurance Business |

| 22 | RHB Insurance Berhad | General Insurance Business |

| 23 | Tokio Marine Life Insurance Malaysia Bhd | Life Insurance Business |

| 24 | Tune Insurance Malaysia Berhad | General Insurance Business |

| 25 | Zurich Life Insurance Malaysia Berhad | Life Insurance Business |

| No. | Takaful Insurance Company | Category of Business |

| 1 | AIA PUBLIC Takaful Berhad | Family Takaful Business |

| 2 | AmMetLife Takaful Berhad | Family Takaful Business |

| 3 | Etiqa Family Takaful Berhad | Family Takaful Business |

| 4 | Etiqa General Takaful Berhad | General Takaful Business |

| 5 | FWD Takaful Berhad | Family Takaful Business |

| 6 | Great Eastern Takaful Berhad | Family Takaful Business |

| 7 | Hong Leong MSIG Takaful Berhad | Family Takaful Business |

| 8 | Prudential BSN Takaful Berhad | Family Takaful Business |

| 9 | Sun Life Malaysia Takaful Berhad | Family Takaful Business |

| 10 | Syarikat Takaful Malaysia Am Berhad | General Takaful Business |

| 11 | Syarikat Takaful Malaysia Keluarga Berhad | Family Takaful Business |

| 12 | Takaful Ikhlas Family Berhad | Family Takaful Business |

| 13 | Takaful Ikhlas General Berhad | General Takaful Business |

| 14 | Zurich General Takaful Malaysia Berhad | General Takaful Business |

| 15 | Zurich Takaful Malaysia Berhad | Family Takaful Business |

No. Name Ownership

1 AIA Berhad

USA company

2 AXA Affin Life Insurance Berhad

affin bank group

Dear Valued Customer

On 30th August 2022, Generali Asia completed the purchase of the remaining 51% of MPI Generali shares adding to its existing 49% share ownership, making Generali the sole owner of MPI Generali (Find out more) .

On the same day, Generali also acquired approximately 53% of AXA Affin Ge neral Insurance Berhad (AAGI), whilst Affin Bank owns the remaining 47%. Generali has submitted a proposal to integrate the business of MPI Generali into AXA Affin General Insurance Berhad.

This business transfer is in accordance with Bank Negara Malaysia (BNM)’s single presence policy, where a shareholder can only own one General and one Life Insurance license.

We had previously communicated that this is expected to take effect on 28th February 2023.

However, we are now working towards a new date; 1st Apri 2023 or such a date as may be approved by the Court. When this happens, then the integrated company will be fully reremaining 30% branded “Generali”.

Upon the completion of this integration, Generali will hold 70% of the combined business and Affin Bank will hold the We would like to assure you that the benefits and terms of your insurance policies with us will not be affected as we undergo proposed business transfer and name change. Your rights and obligations under MPI Generali’s insurance policies wil to you.

I remain the same. We are committed as ever to be of service Once the business transfer is approved, our documents will showcase the new company name and inclusion of “formerly known as AXA Affin General Insurance Berhad” as is required by the regulations.

Following the launch of the newly branded company, the remaining integration activities will take place over an extended period of time. e insurer in Malaysia.

The future combined company and unified brand will form the second largest general insurer and an emerging lif This is yet another significant milestone for us and we are delighted as we countdown to introducing Generali to all Malaysians.

Generali is one of the largest global insurance and asset management providers.

Established in 1831, it is present in over 50 countries in the world, with a total premium income of € 81.5 billion in 2022.

192 years !!!!!

With 82,000 employees serving 68 million customers, the Group has a leading position in Europe and a growing presence in Asia and Latin America.

Generali is Italian company

Global Fortune 500 (#72);

Generali has a direct presence in 34 countries.

3 Allianz Life Insurance Malaysia Berhad

Germany company

4 AmMetLife Insurance Berhad ambank group

MetLife, Inc. is the holding corporation for the Metropolitan Life Insurance Company, better known as MetLife, and its affiliates.

USA

5 Etiqa Life Insurance Berhad

Maybank group

6 Gibraltar BSN Life Berhad

bank simpanan nasional

It's Now Known As BSN Life

30 Apr 2014

HERE COMES GIBRALTAR BSN LIFE

KUALA LUMPUR - After just over a decade in operation, life insurer Uni.Asia Life Assurance Bhd (UAL) has ceased to exist, and is now known as Gibraltar BSN Life Bhd, following the entry of new owners Prudential Financial, Inc (PFI) of the US and Bank Simpanan Nasional (BSN).

PFI holds a 70% stake in Gibraltar BSN Life through its subsidiary, The Prudential Insurance Company of America (PICA), and BSN the remaining 30%, following a RM518 million acquisition of UAL which was completed in January 2014.

7 Great Eastern Life Assurance (Malaysia) Berhad

ocbc group singapore

8 Hong Leong Assurance berhad

HONG LEONG FINANCIAL GROUP BHD

KLSE (MYR): HLFG (1082)

9)MCIS Insurance Berhad

sanlam group

South africa

10 Manulife Insurance Berhad

Canada company

11 Prudential Assurance Malaysia Berhad

Uk company

12 Sunlife Malaysia Assurance Berhad

Sun Life Financial Inc. is a Canadian financial services company

13 Tokio Marine Life Insurance Malaysia Bhd

Japan company

14 Zurich Life Insurance Malaysia Berhad

Switzerland company

15 Syarikat Takaful Malaysia Keluarga Berhad

TAKAFUL (6139)

But nowadays no much more medical card that is not ILP

A lot of people find this hard to accept. Maybe when they bought their cards, their advisor or agent told them, “This is cheap, right?”

After that, we think the 5 years, normally, the cost of this medical card increase every 5 years, there is one rate, the next 5 years, there is a different rate to pay.

Then, you say, “Hey, how come it keeps on increasing?”

That is how a

standalone medical card

is structured, and you must be prepared for that.

Bersusah-susah dahulu, bersenang-senang kemudian

=

ILP medical card

Renewal Conditions

Most standalone policies provide a guarantee that your policy will be renewed even though you’ve been diagnosed with an illness before your next renewal date.

This is good to have. Here’s the reason why. Say if you were diagnosed with diabetes this year, and your policy is not a guaranteed renewal policy, the company has every right to reject your renewal.

Now, you’re left with zero coverage for next year. Adding to that, other insurance companies won’t accept your application either, because now you have diabetes and it’s a risk they are usually not willing to take.

Bersenang-senang dahulu, Bersusah-susah kemudian =

Standalone medical card

This post has been edited by plouffle0789: Nov 20 2023, 01:17 PM

Quote

Quote

RM1 million medical protection per year

RM1 million medical protection per year

bleeding for every month

bleeding for every month

0.1717sec

0.1717sec

0.37

0.37

5 queries

5 queries

GZIP Disabled

GZIP Disabled