QUOTE(JustcallmeLarry @ Jun 13 2019, 10:39 AM)

Hey guys there 2 types of insurance plan right, ilp and standalone one??? Wta which one is cheaper or are both the same over time?

googled and found this....

Medical insurance comes in two forms – a no-frills standalone medical plan, and a medical rider attached to a life policy such as an investment-linked plan (ILP).

The former covers hospitalisation and surgical expenses, while the latter also does that, in addition to paying a lump sum in the event of death and/or total and permanent disablement.

How to decide

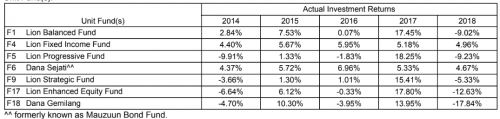

So what should a policyholder do? When choosing between a standalone medical plan and a medical rider, one way is to assess your financial habits. FA Advisory’s Liau points out that premiums for both plans are not fixed as they are subject to reviews and increments in future.

“If a person has proper financial planning, and the discipline to invest the premium difference between a standalone medical plan and an ILP with medical rider, then a standalone medical plan may be more suitable,” he says. By contrast, if a person doesn’t have the discipline to save and invest regularly, an ILP may be a better option as it is a form of forced savings/investment. The plan, he adds, could help the person invest the additional premium to offset future increment in health premiums.

http://www.focusmalaysia.my/Income/when-to...ne-medical-planhttps://www.google.com/search?source=hp&ei=...i21.OekAqEtEP-0

i think many had mentioned that in normal economic sense....standalone is better than ILP.....

but many had complaint too, that standalone insurance premium can / will increase termendously especailly at/after retirement age brackets....when that is the time we usually needed both of them (insurance) and money most

Jun 12 2019, 09:26 PM

Jun 12 2019, 09:26 PM

Quote

Quote

0.0195sec

0.0195sec

0.76

0.76

6 queries

6 queries

GZIP Disabled

GZIP Disabled