thank you guys/girls for posting informative and useful replies and keeping this channel open for more information clarification and sharing.....

Insurance Talk V5!, Anything and everything about Insurance

Insurance Talk V5!, Anything and everything about Insurance

|

|

Dec 23 2018, 12:11 PM Dec 23 2018, 12:11 PM

Return to original view | Post

#1

|

Senior Member

8,188 posts Joined: Apr 2013 |

thank you guys/girls for posting informative and useful replies and keeping this channel open for more information clarification and sharing.....

|

|

|

|

|

|

Jan 13 2019, 12:08 PM

Return to original view | Post

#2

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(shodan11 @ Jan 13 2019, 10:28 AM) Not saying this for sure. Currently most CI products/riders are based on 36 CIs. Hence if there's any add-on coverage, the customer might lose out on the additional benefits offered. I might need to check on this later, while we may wait for experienced agents to come and explain further. just checking with you.......last week I had a brief encounter with my friend.....However, by doing endorsements (adding up coverage/new benefits), the client will get to enjoy the new expanded CI benefits.  he mentioned that his son was admitted to a hospital and had a surgery........ it was something like pancreas covering the liver (sort of like that)..... he mentioned that it was a "heaven born" (Chinese translation)...natural occurrence.... thus his insurance does not cover that "heaven born"..... is it true that natural occurance are not covered by insurances?  |

|

|

Jan 20 2019, 04:37 PM

Return to original view | Post

#3

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(lustman @ Jan 20 2019, 03:12 PM) Zurich Takaful has increased my son's annual premium for medica2015 M250 plan from rm980 to rm1891 for 2019, which just doesn't make f8888ing sense. It's more than 100%. Anyways, am looking for others takaful companies now, any recommendations? tqvm  why is it increase by so much? why is it increase by so much?for my case,....both my sons insurance bought since age 1, had their insurance premium reduced by about 40% when they reached age 6 or 7....if I am not mistaken... |

|

|

Jan 21 2019, 10:35 AM

Return to original view | Post

#4

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(woonsc @ Jan 21 2019, 09:48 AM) I see, as I am still at my teens, Would it be advisable to purchase, a PA plan, a medical card and critical illnless coverage with term insurance? I suggested to my niece to buy PA for her 1st insurance...for she rides bike to work in the city center.This post has been edited by yklooi: Jan 21 2019, 10:36 AM |

|

|

Feb 18 2019, 07:32 PM

Return to original view | Post

#5

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(alexkos @ Feb 18 2019, 07:21 PM) So...whats the suggested annual limit for medical card? Is 200k enough? I think it all boils down to depends....depends on your expectation depends on your budget depends on your income depends on your "wish' to haves. depends on your lifestyles depends on your family medical history depends on your experiences encountered on those that has medical situations depends on your experience and the satisfaction encountered at the Govt hospitals.... etc etc.... just like yesterday my family asked me what should they have for lunch...is RM 40 enough for a family of 4? |

|

|

Feb 22 2019, 11:53 PM

Return to original view | Post

#6

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(NosaJC @ Feb 22 2019, 11:49 PM) Hi guys, may i know which plan have the best coverage for critical illness now?? while waiting for responses on the undefined criteria for "BEST"......try this?Best Critical Illness Insurance in Malaysia https://ringgitplus.com/en/health-insurance...itical-illness/ This post has been edited by yklooi: Feb 22 2019, 11:54 PM |

|

|

|

|

|

Feb 25 2019, 05:02 PM

Return to original view | Post

#7

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

the older a car, the chances of breakdown become more,

the older one gets, the chances of sickness become more. Attached thumbnail(s)

|

|

|

Mar 9 2019, 11:25 AM

Return to original view | Post

#8

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(blibala @ Mar 9 2019, 11:17 AM) Maybe my ge agent is not keen on small increase in premium for medical plan upgrade. I can afford a RM500/mth life insurance plan but i just dont need that as i already have sufficient coverage and own planning. a friend of mine suggested to me...to get over the counter cholesterol pills for a few months....get the blood test, get the good result then pass to the insurance company...Anyway, thanks for your advise. I will start to exercise from now on. Hopefully will improve my cholesterol level. Fatty liver has no cure so far according to GP. Need to maintain healthy lifestyle. the "loadings" on cholesterol if any is way to much ...he said. that applies to high blood pressure too. This post has been edited by yklooi: Mar 9 2019, 11:31 AM |

|

|

Mar 15 2019, 08:41 PM

Return to original view | Post

#9

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(ollamigo @ Mar 15 2019, 08:32 PM) Hi all sifus, did the doctors there mentioned which is the "easiest" to claim?I'm having dilemma in choosing new company for my life insurance and medical card. May i have few thoughts in which company is most reliable? My current is with pru bsn prudential (already 9 months). I went to KPJ at my place and supposed to be admitted but the doctors there mentioned there is high possibility that i wont be covered and have to pay myself as they are having a lot of issues pru bsn not covering their patients. And i can see their worried face when i mentioned that my insurance is pru bsn. can check with them? since they are the going thru all those claims almost daily and after some years, they must know the answers....can you find out and let us know? answers from here are or may not be so reliable for there maybe "vested" interest in each responses. |

|

|

Apr 1 2019, 07:18 PM

Return to original view | Post

#10

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(scriptkiddie44 @ Apr 1 2019, 05:34 PM) Look at the premium difference, in 6 years, she lost almost RM6k on the cash value. It looks like I can sustain much more longer in the long run (I'm not an insurance expert, I'm just doing some simple calculation). this was what was shown to me too...If I saved up that difference in premium paid, when the time the premium increased, I can just top up using the saving right. Some more, I can use that amount if in any emergency need of money. So I explain the whole situation to my friend, ask her to consult with her agent, and do the math again to her agent. Guess what her agent said? "If you insists to pay less and have more coverage, dont blame me if your premium increase in the future." Then my friend tell the agent that if the premium increased, can just use the difference in premium paid to top up back right? Then the agent did not reply. This looks like some con job if you ask me. Not saying that insurance is a con job, but I'm just doing some math. So my point is, what's the point of putting so much portion in cash value if saving in FD can yield more return? I know the high risk high reward thingy, but look at the performance of the fund. 6 years ald losing 6k. Even if it doubles in 5 years, still not making any profit with the fund. How to sustain long? Expert here can educate me if I'm wrong, as I'm not an insurance expert. it is like....pay more now or pay more later.... any which way also have to pay....it is either pay more premium now to accumulate more money (saved inside) to pay for the increase of premium in future years.... or pay lesser premium now (and accumulate DIY cash variance), and use the DIY accumulated cash to pay for higher premium later years. either way...do you want a peace of mind of knowing that your premium will not increase over the year? or grumbles at each increases in which the duration and quantum of large increases? i decided to stay off buying new insurances due to budget contraints..... not enough money...lesser headach to decide..... |

|

|

Apr 14 2019, 03:49 PM

Return to original view | Post

#11

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(HoNeYdEwBoY @ Apr 12 2019, 01:53 AM) You don't take investment-linked insurance plan (ILP) as an actual "investment". The actual benefit of ILP is to handle future increment of insurance charges thus see what I posted before this. QUOTE(MUM @ Apr 12 2019, 08:44 AM) ever made the comparison by calculation?assuming "everything" is the same, except the premium.... getting the non ilp and putting the differences of premium into a 6% pa vehicle, then getting that accumulated saving + % returns to pay for the cost differences of the premium increases in future..... in the end, will it generate more "saving" than that similar ILP product? QUOTE(HoNeYdEwBoY @ Apr 12 2019, 06:25 PM) Non ILP plan aka standalone alone medical card are most likely has increment in price from time to time. Therefore, you might pay even more in future. I will try roughly make a comparison table for everyone, but please don't refer to it at 100%. must have completed the comparison table to enable below comment.....(mind showing the table?...interested to find the truth)QUOTE(HoNeYdEwBoY @ Apr 14 2019, 03:36 PM) ILP is cheaper in the long run because even so insurance charges increase the "cash value" inside the ILP mostly can cover up it compare to stand-alone, it has no cash value or additional add on; eg: Critical Illness with Early Payout (Great Eastern). Mostly standalone medical card cannot add on a lot of stuff one, usually you need to take ILP only can have such privilege to add on more. |

|

|

Apr 14 2019, 06:06 PM

Return to original view | Post

#12

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

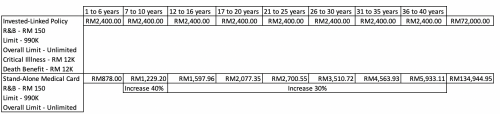

QUOTE(HoNeYdEwBoY @ Apr 14 2019, 04:32 PM)  This is base on 25 years old male, non smoking. Take this as reference, different company has different price increment. I just roughly do a simple comparison chart, and there's actually a lot of other factors will take in count on this. can confirm the maths? if the true variance is just 20k.....then the ILP is not as 'untung" as stand alone???? Attached thumbnail(s)

|

|

|

Apr 15 2019, 10:55 AM

Return to original view | Post

#13

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(attentional @ Apr 15 2019, 10:50 AM) So if means if i can afford it, it's ok? 2% just for this plan?Around 2% of my salary. what is the total household budget used for insurance? yes, if can afford it...go get it,....but then is "that" coverage enough  |

|

|

|

|

|

Apr 20 2019, 10:49 AM

Return to original view | Post

#14

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(Ilnov @ Apr 20 2019, 10:45 AM) Still not so understand how does this co insurance work. Assuming my monthly premium quoted from both GE and Pru around RM250 monthly, wouldn’t GE medical card seems stronger because no co insurance? is "EVERYTHING Else are the same" except the co insurance part? |

|

|

Apr 20 2019, 12:10 PM

Return to original view | Post

#15

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(Ilnov @ Apr 20 2019, 11:18 AM) Yes, it seems everything else is the same except Pru have co insurance. read this tnc on one of the site....of MVP bonus....1. Annual limit: GE - RM1,320,000 and Pru no annual limit when I asked my agent 2. Lifetime limit: GE unlimited and Pru goes by MVP RM1mil, is that my lifetime limit with Pru? 3. Both also same room and board of RM200 How do you state that having full coverage can end up being expensive? Maybe I am zero knowledge about this insurance thing. I seeing both monthly premium of med card is the same amount. "Med Value Point increases at 2% of the initial Med Value Point at the end of every 2 policy years provided no claim has been incurred during the 2 policy years. Applicable to plans with Hospital Daily Room & Board of RM300 and above" just not sure if this is applicable to your mentioned plan..... https://www.prudential.com.my/en/our-produc...y-medical-plus/ |

|

|

Apr 29 2019, 12:04 PM

Return to original view | Post

#16

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(sheahann @ Apr 29 2019, 11:41 AM) Why is “Guaranteed Renewable” important? just a note to consider....Guaranteed renewable means that as long as you pay for the policy on time and you want to continue with the insurance, the insurance company is obliged to renew the policy (if the lifetime claim limit has not been exceeded). The insurance company, however, can raise insurance price as long as the change affects everyone and does not single you out. For non-guaranteed renewable insurance (where policies are renewable on yearly basis), the renewal of these policies is subject to the insurers’ approval. This is bad because when you have an illness that is likely to happen again, the insurance company will deny you the renewal. Now, when you want to buy insurance from a different company, it will be difficult to get, because you have a past illness that you need to disclose. An illness in the past, is also called pre-existing condition. The new insurance company will either load your premium (the insurance is more expensive) or will exclude the illness from the new medical card. This means that when the illness happens again, the insurance company will not pay for any treatment. This is why it is important to buy medical insurance early in life so that when you start buying medical insurance you do not have any pre-conditions and can be fully covered by a medical card. if you had a haemorrhoids claim at age 30......they will (most probably will) excludes haemorrhoids, ANY diseases or disorder of colon/large bowel (Diverticulosis sac) from the coverage on the NEXT renewal..... so in the end one nay not be fully covered even with full guaranteed renewal.... |

|

|

Jun 2 2019, 09:14 AM

Return to original view | Post

#17

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(matyrze @ Jun 2 2019, 01:27 AM) Why there is very few discussion on Takaful Malaysia? Checking their website, their basic plan for TPD/Death with RM500k coverage is priced at RM80/month only. Any bad feedback/review on their services? have you check also, is that amount of premium paid is for a PA sort of insurance? |

|

|

Jun 2 2019, 11:29 AM

Return to original view | Post

#18

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(matyrze @ Jun 2 2019, 11:16 AM) They have separate plan for PA. This plan is for Death/TPD, and can be customized to include critical illness if the applicant wishes. Refer to link below, can try get quotation and seems like can straight away apply. A bit weird as application usually will require proper medical check up right? https://online.takaful-malaysia.com.my/term-myClickTerm so this RM80/month only premium is for death / Total and Permanent Disability (TPD) only? then if want to add in other coverage it will be more then. yes,...normally for critical illness plan after a certain age and value....they needs medical assessment to determine eligibility but mentioned in their FAQs Pre-existing illness __Not covered TERMINATION OF THIS ANNEXURE The coverage under this Annexure shall automatically terminate upon occurrence of any of the following: (f) when there is fraud or misrepresentation of material fact during application. EXCLUSIONS We will not be liable to pay any benefit under this Annexure for Critical Illness resulting directly or indirectly from any of the following causes: 4.1 Critical Illness which has existed at the Effective Date ..... https://online.takaful-malaysia.com.my/Docu...e%20Wording.pdf This post has been edited by yklooi: Jun 2 2019, 11:43 AM |

|

|

Jun 4 2019, 12:20 PM

Return to original view | Post

#19

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(matyrze @ Jun 2 2019, 02:18 PM) Yes, I haven't tried adding up coverage for CI. But I am pretty sure that for a plan only covering TPD/Death, this is already considerably cheaper than most other insurance out there. Its just that they do not have many agents to promote it. I guess this is why they are cheaper, lower operating cost. I was wondering about their stability as a company, but I think they are hardly a newcomer in the industry. I got my PA insurance from AIA covers 500k too at monthly RM75Should be common for insurance not to fully cover for predetermined illness correct? Or if they do, the premium will be increased quite significantly. I guess this plan is suitable is for those that really2 young and healthy, but lower on budget my insurance plans does not covers pre existing illness.... some of my insurance plans also has to add in extra loadings for my high blood pressure....  I liked to have agent when buying insurance.....for the ease of contact, claim procedures and follow up (not only for me but my dependents/beneficiaries too) my point for my previous post was to say...even they did not insist on medical examination.......there is a risk of non payment incidents when the insurance company found out that there was a non disclosure of illness at time of buying. (at times, a none noticed, none painful, had been there years already (inside/outside of body)....may turn out to be a factor for non disclosure/non payment disputes) This post has been edited by yklooi: Jun 4 2019, 12:37 PM |

|

|

Jun 12 2019, 03:28 PM

Return to original view | Post

#20

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(JuneResources @ Jun 12 2019, 02:52 PM) If I'm not wrong, CIMB mainly sub insurance by Berjaya Sompo. If not, then Berjaya Sompo is under which bank?  googled and found this too....per attached image https://www.berjayasompo.com.my/_uploads/fi...0Dec%202018.pdf Then main consider as under "Khazanah Nasional Berhad", am I right? i think the legal buck stops at Avicennia Capital Sdn. Bhd...eventhought it is a fully owned Khazanah Nasional Berhad investment holding company, Attached thumbnail(s)

|

|

Topic ClosedOptions

|

| Change to: |  0.1259sec 0.1259sec

0.22 0.22

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 30th November 2025 - 11:40 AM |

Quote

Quote