QUOTE(honsiong @ Feb 6 2021, 06:55 PM)

IMO lump sum easier if you put it into a diversified portfolio like stashaway

Do you mean like having 22 26 30 36 distributed across them?

My situation now is I know I'm not getting married, buying a car or house. Say this lumpsum today is gone crash and burn. My current employment with frugal saving can recoup this amount in 2 years time.

My thoughts are, Yolo this lumpsum I have (keep 6 month emergency fund), from today till next 5 years, save up this amount, and contribute say a smaller sum each month (lumpsum +smaller dca), and the leftover I keep somewhere like FD.

Assuming within this 5 years, there is a crash, the FD can be instantly use to buy the low. Therefore offset the drop.

I really have no idea what I should do or am I overthinking. I just don't want my cash get eaten away from inflation.

Before I got all over the place.

Example,

Now dump 100k in stashaway. Each month I normally contribute 2k,but instead I dca 1k, the other 1k keep in FD. Continue dca 1k to SA monthly, 1k the FD. When crash, FD to SA to call buy the dip.

Advantage I can think of

1. My current lumpsum get to stay in market the longest time

2. Still get to DCA, but amount reduce to halves ,thr DCA amount can still get the gains in the market

3. Should it crash, my FD that I set aside should be able to boost back the lost.

Disadvantage

1. It be Hella scary having 100k drop 20 30%.

2. In case some thing in life happen needed cash, I will have very little Liquidity

3. I have to boost my income in order to keep the investment aggressive.

Feb 6 2021, 05:41 PM

Feb 6 2021, 05:41 PM

Quote

Quote

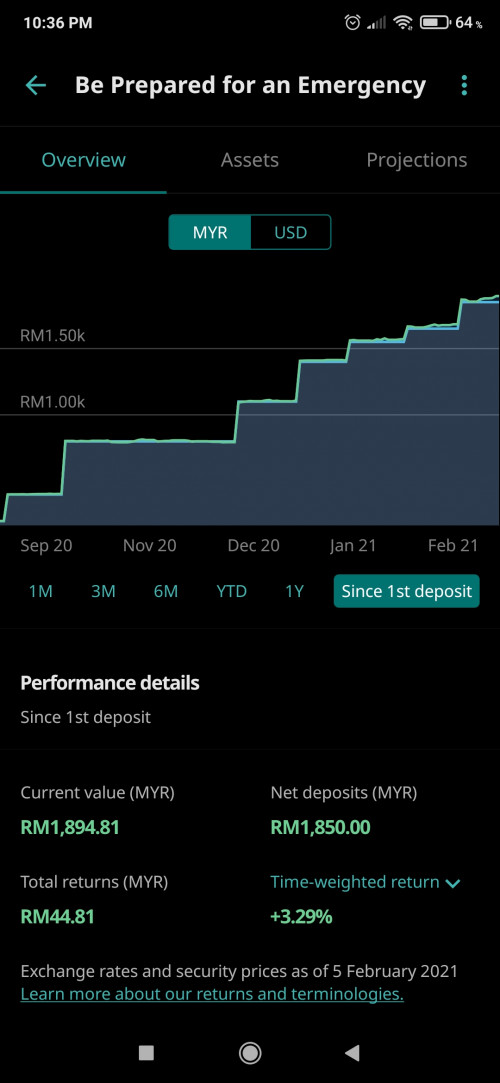

if in USD it's been only +ve growth since November 2020

if in USD it's been only +ve growth since November 2020 ).

).

0.0455sec

0.0455sec

0.52

0.52

6 queries

6 queries

GZIP Disabled

GZIP Disabled