QUOTE(stormseeker92 @ May 7 2020, 05:46 AM)

If im not mistaken it's 36% chance for you to lose money.

well no,https://www.stashaway.my/r/which-stashaway-...ould-you-choose

it just means that 99% chance of not losing more than 36%

Investment StashAway Malaysia, Multi-Region ETF at your fingertips!

|

|

May 7 2020, 08:58 AM May 7 2020, 08:58 AM

Return to original view | Post

#1

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(stormseeker92 @ May 7 2020, 05:46 AM) If im not mistaken it's 36% chance for you to lose money. well no,https://www.stashaway.my/r/which-stashaway-...ould-you-choose it just means that 99% chance of not losing more than 36% |

|

|

|

|

|

May 16 2020, 10:13 AM

Return to original view | Post

#2

|

|

Senior Member

761 posts Joined: Aug 2006 |

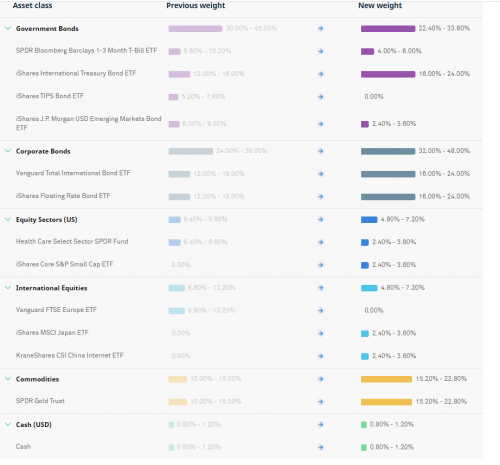

Not sure if others posted this already, but if anyone's curious, 8% risk reoptimizations:

Some highlights I can see: 1) more into treasury bonds 2) more into corp bonds 3) more into Gold (:shrug) |

|

|

May 17 2020, 07:51 AM

Return to original view | Post

#3

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(honsiong @ May 16 2020, 06:39 PM) The 3 ETFs at the top are all US treasuries, they are actually cutting that down and consolidate to just use 1 ETF to get that exposure. But overall they are reducing position in US treasuries. Ah I see, thanks for the correction on my observation, i just took the name for granted :bow |

|

|

May 26 2020, 03:24 PM

Return to original view | Post

#4

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(ironman16 @ May 26 2020, 02:07 PM) PM sales charge more higher compare to others platforms like fsm, eunitrust,..... 😁😁😁 PM and CIMB Principal both charge quite a bit of fee for purchasing if you go through their agents, instead of FSM (Though I dont think PM funds are available on FSM), I think it's about ~5% or so compared to ~2% on FSM. The annual management fee stays the same. |

|

|

Jun 15 2020, 10:50 AM

Return to original view | Post

#5

|

|

Senior Member

761 posts Joined: Aug 2006 |

huh, 4-5 days of processing. I pulled out my highest risk portfolio and dumped it into Simple. Let's see what happens

|

|

|

Jun 15 2020, 12:40 PM

Return to original view | Post

#6

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(cl.t @ Jun 15 2020, 12:13 PM) Wouldn't it be too risky to park everything with SA? What about looking into high yield savings acc like OCBC and SC? Granted, both are up to a max of 100k, but that's 200k in combination ( though, provided you execute their conditions monthly)I have 70% of non-FD investment with SA, and another 30% with eToro. My FD portfolio is 2 times more than non-FD investment, yielding shitty return @ 2.10% but at least protected by PIDM. Hesitating if wanna switch to SA-Simple just for the sake of additional 0.30%.  |

|

|

|

|

|

Jun 16 2020, 10:04 PM

Return to original view | Post

#7

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(000022 @ Jun 15 2020, 10:50 AM) huh, 4-5 days of processing. I pulled out my highest risk portfolio and dumped it into Simple. Let's see what happens Quick update on this, somehow things were transacted pretty quick, all my funds from portfolio is now deposited into Simple. |

|

|

Jun 27 2020, 11:18 AM

Return to original view | IPv6 | Post

#8

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(joshtlk1 @ Jun 27 2020, 09:03 AM) Any started to put in a substantial amount of savings into simple yet? Well, I transferred the entirety of my high risk portfolio into this Simple. And then am planning to DCA back again into it the coming few months. It's a sizeable chunk for me, definitely less than 100k, but I'm not sure what you mean by substantial. The transfer was done on 16 June, and I'm seeing very very minute returns. Like single digit (absolute value, not percentage), which makes sense, considering the projected rate and proratesThis post has been edited by 000022: Jun 27 2020, 11:19 AM |

|

|

Jun 27 2020, 04:49 PM

Return to original view | Post

#9

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(MNet @ Jun 27 2020, 01:54 PM) I see. How about the rest of ur portfolio? or u only have high risk? I keep a 8% portfolio as well, which i’m still regularly depositing into monthly. I’m partial to more government and company bonds now |

|

|

Jun 29 2020, 09:53 AM

Return to original view | Post

#10

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(cyanbleu @ Jun 28 2020, 04:58 PM) I'd like to think no investments are risk free.. with the exception of FD. They mentioned volatility, but with no clear elaboration. 1% chance of your losses 20% and above in a single year's performance.According to the introductory post, I understand the higher the risk profile, the higher the projected returns. And you were right, these 'expected returns' are definitely higher than FD rates (even ASB for that matter). However, in the unfortunate event that the markets go downhill, what kinds of losses am I looking at if I set my risk profile to be, say, 20%? The website says if your profile is set at 20% there's a 1% chance you have 20% losses, which sounds pretty alarming.. Let me know if I misunderstood incorrectly.. There is no limitations to losses in the end, this is an investment, not a guarantee. |

|

|

Jul 27 2020, 10:37 PM

Return to original view | IPv6 | Post

#11

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(!@#$%^ @ Jul 27 2020, 10:33 PM) not saying they are not wrong but actually, emergency funds shouldn't be in SAMY in the first place. I think that's the whole issue; Money which should not be invested ARE being moved, without the consent of the owner. It really could be that someone hits into a string of bad luck, and need taht sum of money immediately, to which all are in SAMY now. :shrugI'm hoping for a better explanation than just a "technical glitch" throwaway line. |

|

|

Dec 26 2020, 10:03 PM

Return to original view | Post

#12

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(Oklahoma @ Dec 26 2020, 12:39 PM) Ok apologies. Anyhow how's your experience with stashaway? I put 36% risk, so far so good. Personally, I would think that if you have to ask that question, then it is a solid no. I dont have a solid number on the ratio, but I think 3-6 months of expenses should be in "safe and easily liquidated investments" like high interest savings account and the likes. After which the ratio in how much to diversify between low risk investments like money market fund or ASB/ASM and high risks ones like SA is up to you.I placed all my hard earned money in stashaway, is it wise? WhitE LighteR liked this post

|

|

|

Jan 25 2021, 02:38 PM

Return to original view | Post

#13

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(vanitas @ Jan 25 2021, 11:52 AM) And that's with up to 5.5% sales charge, and up to 2% annual management fee. I would be very interested if SA would be transparent on their profitability. It would be scary leaving assets with them if they are continually in the redAny idea on how much AUM does StashAway need to have for sustainable business? Quazacolt, walnut6363, and 1 other liked this post

|

|

|

|

|

|

Jan 25 2021, 06:57 PM

Return to original view | Post

#14

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(MUM @ Jan 25 2021, 02:41 PM) are you buying SA stocks or investing your money thru SAMY? Doesnt matter, if they go down, we will be affected regardless, much like Smartly:https://www.youtube.com/watch?t=1677&v=L7Kj3iMK7cM |

|

|

Jan 25 2021, 08:11 PM

Return to original view | Post

#15

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(backspace66 @ Jan 25 2021, 07:06 PM) I am more concern in force liquidation during unfavourable time and delay to get the liquidated fund. Yea, it's what happened with customers of Smartly. QUOTE(MUM @ Jan 25 2021, 07:10 PM) if really concern of forced liquidation in time of unfavourable time....be it ex: (war inclusive) Consider during the period of March of 2020, when Smartly promptly announce that they are closing down. If the same were to occur, one would have a high chance of being forced to liquidate at a loss. Compared to other instruments, which may suffer paper losses, but overall, will recover in future (as it is example with 2020), and one can cash out later for profit instead of loss.so are your money in EPF, money in unit trust, gold and all other investments..... Therefore it would certainly be good to know more about SA's financial health. |

|

|

Jan 25 2021, 08:47 PM

Return to original view | Post

#16

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(MUM @ Jan 25 2021, 08:13 PM) forced liquidation can come in many form.....valid or not is up to each perspective... Hence why this chance can be better reasoned about with more information in regards to a company's financial health. So you see why I mentioned that it would be preferable to have that disclosed, unlikely as it is.believing of the chances of it to happens is also each perspective wanting to invest in SA or any other form be it stock or CIS etc etc...always has the chances of forced liquidation. |

|

|

Feb 6 2021, 09:07 PM

Return to original view | Post

#17

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(ironman16 @ Feb 6 2021, 04:50 PM) Wrong wrong wrong As some have already pointed it out, lump sum investing in most cases outperform DCA, with enough time in market. I think someone posted some research a few pages back, can go look it up.Got money oso dca, unless u timing the market very pro 😜 |

|

|

Feb 6 2021, 09:19 PM

Return to original view | Post

#18

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(littlegamer @ Feb 6 2021, 09:07 PM) Do you mean like having 22 26 30 36 distributed across them? Personally think that this 6 months emergency savings can go into less risky vehicle like FD. I would not recommend dumping all your emergency savings into higher risk investment. If your investment strategy may cause you to be stressed out or emotional about it, I dont think you should be following it.My situation now is I know I'm not getting married, buying a car or house. Say this lumpsum today is gone crash and burn. My current employment with frugal saving can recoup this amount in 2 years time. My thoughts are, Yolo this lumpsum I have (keep 6 month emergency fund), from today till next 5 years, save up this amount, and contribute say a smaller sum each month (lumpsum +smaller dca), and the leftover I keep somewhere like FD. Assuming within this 5 years, there is a crash, the FD can be instantly use to buy the low. Therefore offset the drop. I really have no idea what I should do or am I overthinking. I just don't want my cash get eaten away from inflation. Before I got all over the place. Example, Now dump 100k in stashaway. Each month I normally contribute 2k,but instead I dca 1k, the other 1k keep in FD. Continue dca 1k to SA monthly, 1k the FD. When crash, FD to SA to call buy the dip. Advantage I can think of 1. My current lumpsum get to stay in market the longest time 2. Still get to DCA, but amount reduce to halves ,thr DCA amount can still get the gains in the market 3. Should it crash, my FD that I set aside should be able to boost back the lost. Disadvantage 1. It be Hella scary having 100k drop 20 30%. 2. In case some thing in life happen needed cash, I will have very little Liquidity 3. I have to boost my income in order to keep the investment aggressive. In any case, maybe 3 months of savings can suffice for now, depending on your dependents and situation, and you can go ahead and put those in high interest savings acc , and then the other 3 months into SA or other higher risk investments. The thing about buying the dip? If you already know when to do so, I dont think you'll need to be asking in thread anyway. honsiong liked this post

|

|

|

Feb 6 2021, 10:52 PM

Return to original view | Post

#19

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(littlegamer @ Feb 6 2021, 09:49 PM) What I mean is the 6month emergency is already set aside. This 6month fun is nothing to do with stashaway, it will always be in Fd like a break glass if shit goes south kinda piggy bank. Well, I guess all good then. The problem with the dip is, you do not know how low the dip is, but then again, it's moot if you're using funds that are very much disposable, you prolly wont get panic if it ever drops and cut your losses on a frenzy.Regarding the dip, no one can predict. But I'm thinking if there is a dip then I will have some amount ready. Quazacolt and WhitE LighteR liked this post

|

|

|

Jan 21 2024, 09:45 PM

Return to original view | Post

#20

|

|

Senior Member

761 posts Joined: Aug 2006 |

QUOTE(siaush @ Jan 18 2024, 02:37 PM) Any other suggestions other than Versa, GO+ and KDI? A few weeks ago i lifted majority of my holds on 36% and 22% to stash away simple to realize profit and slowly DCA back into the portfolios, with the recent announcement, I've made request to withdraw all from simple. Will be placing all of it in Rize for 4% until March. After that? well, hopefully someone has some other place to recommend. |

| Change to: |  0.6079sec 0.6079sec

0.54 0.54

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 1st December 2025 - 03:22 AM |

Quote

Quote