QUOTE(Harddisk @ Dec 5 2025, 09:05 PM)

4.00% on Bonus Pocket

Opens 2x at RM25,000 and keep for 3 months, correct?

Need to play game?

Need to lock up the money.Opens 2x at RM25,000 and keep for 3 months, correct?

Need to play game?

Banking GXBank - First Malaysian Digital Bank (by Grab), UNLIMITED 1% cashback+3% p.a. interest!

|

|

Dec 6 2025, 07:42 AM Dec 6 2025, 07:42 AM

|

All Stars

24,402 posts Joined: Feb 2011 |

QUOTE(Harddisk @ Dec 5 2025, 09:05 PM) 4.00% on Bonus Pocket Need to lock up the money.Opens 2x at RM25,000 and keep for 3 months, correct? Need to play game? |

|

|

|

|

|

Dec 6 2025, 07:43 AM

|

|

All Stars

24,402 posts Joined: Feb 2011 |

QUOTE(Augusta @ Dec 6 2025, 03:40 AM) Sorry didn't follow anything about GX, what is the 91.25x11 about? How GXbank calculate your interest. That way you get RM0.11 x 364/RM1003.75 x100% = 4%p.a |

|

|

Dec 6 2025, 08:10 AM

Show posts by this member only | IPv6 | Post

#4923

|

Junior Member

611 posts Joined: Sep 2022 From: Last member of the tribe |

so its normal right to have zero amount in the main account,with 2 pocket of 25k each..i thought 2% goes to main account and other 2% will realease end of tenure

|

|

|

Dec 6 2025, 08:31 AM

|

All Stars

65,343 posts Joined: Jan 2003 |

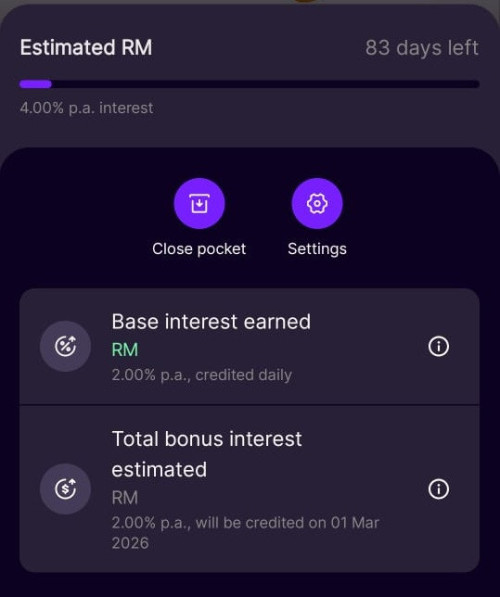

QUOTE(poco loco @ Dec 6 2025, 08:10 AM) so its normal right to have zero amount in the main account,with 2 pocket of 25k each..i thought 2% goes to main account and other 2% will realease end of tenure all happened in bonus pocket, including the 2% base interest, added daily on top of 25k fund |

|

|

Dec 6 2025, 03:30 PM

|

|

Junior Member

699 posts Joined: Aug 2012 |

Have anyone ever experience you make transfer out the system issue receipt they were successful but not received in the receiving party account?

I just realised two credit card payment I made to UOB cc on 3rd not reflect in the UOB cc. |

|

|

Dec 6 2025, 04:53 PM

|

|

Senior Member

5,831 posts Joined: Jun 2017 |

Sorry for asking. Can't follow all these pocket this or bonus that. Just put money into GX bank, how much is the interest now? Thanks my44 liked this post

|

|

|

|

|

|

Dec 6 2025, 07:34 PM

Show posts by this member only | IPv6 | Post

#4927

|

Senior Member

2,967 posts Joined: Jan 2003 |

QUOTE(Ramjade @ Dec 6 2025, 07:42 AM) Need to lock up the money. So as daily interest added to the pocket, can I take them out and leave it at 25k each, or I can't touch it at all? |

|

|

Dec 6 2025, 07:40 PM

|

|

Senior Member

4,684 posts Joined: Jan 2003 |

QUOTE(Ramjade @ Dec 4 2025, 11:49 PM) People there like cash. If you use card, you pay extra 2-3% Yes because it is merchant imposed charges on the consumer itself unless the merchant decide to waive it QUOTE(joshhd @ Dec 5 2025, 12:18 AM) Does the merchant there in New Zealand typically charges such 2-3% fee even for debit cards? Because it is fee imposed from the banks itself to use the EFTPOS payment gateway to the merchants Previously before Covid most merchant will absorbed it but now higher operation costs and lower margins hence why most merchants will self imposed it to cover the charges QUOTE(Ramjade @ Dec 5 2025, 08:47 AM) I guess so cause they cant differentiate credit or debit card. Yes under EFTPOS no distinction on debit or credit just the card provider network itself QUOTE(jasontoh @ Dec 5 2025, 11:37 AM) Shouldn't the card number already can tell whether it is a debit or credit? That is how the card tier is segregated also. I know in some places we have to select either Debit/Credit during the transactions. EFTPOS doesn’t bother whether debit or credit 🤦♀️ it is segregated by the network card provider QUOTE(Ramjade @ Dec 5 2025, 04:58 PM) You tap you think the reader tell the seller it's credit card or debit card? To make it easier, you use card charge extra lo. No need to think of debit or credit card. EFTPOS reader doesn’t need to because it is only defined by savings or card which simplify and for faster transaction QUOTE(jasontoh @ Dec 5 2025, 05:08 PM) No, some countries they allowed to use credit/debit transaction regardless of the card type, I was using credit cards on those machines and those are without charges. Actually, the seller can know the card type easily by just looking the Debit sign there. I'm quite surprise New Zealand actually have charges for credit card transaction, the first time when I watch some of the FB videos. You can’t compare 🤦♀️ because each country payment systems setup differently and charges differ because processing differs based on what it is setup by country central bank Previously Malaysia also have CC or debit charges until BNM decided to take action and imposed blanket mandatory to force the merchant to waive off those charges lerijiso liked this post

|

|

|

Dec 6 2025, 07:42 PM

|

|

Senior Member

4,684 posts Joined: Jan 2003 |

QUOTE(Harddisk @ Dec 6 2025, 07:34 PM) So as daily interest added to the pocket, can I take them out and leave it at 25k each, or I can't touch it at all? When it is already locked up why do you touch it 🤦♀️ unless do you want 2% bonusWhich is why it is different plain old standard 2% pocket otherwise why GX bother to offer 2% top up bonus for it |

|

|

Dec 7 2025, 02:00 PM

Show posts by this member only | IPv6 | Post

#4930

|

|

Senior Member

7,799 posts Joined: Dec 2014 From: Malaysia |

QUOTE(xander2k8 @ Dec 6 2025, 07:40 PM) Yes because it is merchant imposed charges on the consumer itself unless the merchant decide to waive it So Malaysia's Bank Negara forces Malaysian merchants here to absorb the card network charges (where applicable), but that doesn't happen in other countries? Because it is fee imposed from the banks itself to use the EFTPOS payment gateway to the merchants Previously before Covid most merchant will absorbed it but now higher operation costs and lower margins hence why most merchants will self imposed it to cover the charges Yes under EFTPOS no distinction on debit or credit just the card provider network itself EFTPOS doesn’t bother whether debit or credit 🤦♀️ it is segregated by the network card provider EFTPOS reader doesn’t need to because it is only defined by savings or card which simplify and for faster transaction You can’t compare 🤦♀️ because each country payment systems setup differently and charges differ because processing differs based on what it is setup by country central bank Previously Malaysia also have CC or debit charges until BNM decided to take action and imposed blanket mandatory to force the merchant to waive off those charges You're saying that some other countries will still charge a few % of fees (could be network fee or mark-up fee even when DCC isn't applied to a foreign bank card?) regardless if you're using debit or credit card? If that's the case, Malaysia considered very good already?  |

|

|

Dec 7 2025, 03:17 PM

|

|

Senior Member

5,490 posts Joined: Feb 2009 |

QUOTE(joshhd @ Dec 7 2025, 02:00 PM) So Malaysia's Bank Negara forces Malaysian merchants here to absorb the card network charges (where applicable), but that doesn't happen in other countries? Another factor that our merchant is more willing to absorb is also due to BNM implementing PCRF which significantly reducing the interchange fee.You're saying that some other countries will still charge a few % of fees (could be network fee or mark-up fee even when DCC isn't applied to a foreign bank card?) regardless if you're using debit or credit card? If that's the case, Malaysia considered very good already? joshhd liked this post

|

|

|

Dec 7 2025, 04:53 PM

|

|

Senior Member

4,684 posts Joined: Jan 2003 |

QUOTE(joshhd @ Dec 7 2025, 02:00 PM) So Malaysia's Bank Negara forces Malaysian merchants here to absorb the card network charges (where applicable), but that doesn't happen in other countries? Yea BNM forces the merchant acquirer to lower the charges 1st to below 1% which make the merchants able to absorb the charges You're saying that some other countries will still charge a few % of fees (could be network fee or mark-up fee even when DCC isn't applied to a foreign bank card?) regardless if you're using debit or credit card? If that's the case, Malaysia considered very good already? As long as you uses any payment provider in the world there is a charge called Merchant Disount Rate which are imposed on every transaction on any card provider which can only be lowered by each country central bank through the country financial regulation Consider good 🤦♀️ but not as good as EU central bank payment regulation which currently is the gold standard Can’t say for AMEX because the charges are different and higher which why many banks are not willing to offer Also, under the recent US ART deal there isn’t any submission and compliance for financial regulations otherwise it will be another BNM itself QUOTE(Fantasia @ Dec 7 2025, 03:17 PM) Another factor that our merchant is more willing to absorb is also due to BNM implementing PCRF which significantly reducing the interchange fee. Yes through PCRF and interchange centralized process changes they are able to lower the fee as low as 0.2% these days joshhd liked this post

|

|

|

Dec 8 2025, 03:51 PM

|

|

Senior Member

1,142 posts Joined: Oct 2018 |

QUOTE(Harddisk @ Dec 6 2025, 07:34 PM) So as daily interest added to the pocket, can I take them out and leave it at 25k each, or I can't touch it at all? you can't partially withdraw as the only option would be closing the pocket |

|

|

|

|

|

Dec 8 2025, 05:28 PM

|

|

Senior Member

2,967 posts Joined: Jan 2003 |

QUOTE(1mr3tard3d @ Dec 8 2025, 03:51 PM) you can't partially withdraw as the only option would be closing the pocket Thanks for the detailed reply.So I assume the daily interest is compounded, while the additional 2% that pay out at the final of the tenure is not compounded? |

|

|

Dec 8 2025, 07:46 PM

|

Newbie

7 posts Joined: Dec 2007 |

does the 3 months bonus pocket seem like a 2% p.a. multiplied by 2 for the 'hibah'?

|

|

|

Dec 8 2025, 08:43 PM

Show posts by this member only | IPv6 | Post

#4936

|

|

Junior Member

373 posts Joined: May 2019 |

QUOTE(Harddisk @ Dec 8 2025, 06:28 PM) Thanks for the detailed reply. Sounds rightSo I assume the daily interest is compounded, while the additional 2% that pay out at the final of the tenure is not compounded? Harddisk liked this post

|

|

|

Dec 9 2025, 01:19 PM

|

|

Senior Member

1,142 posts Joined: Oct 2018 |

QUOTE(Harddisk @ Dec 8 2025, 05:28 PM) So I assume the daily interest is compounded, while the additional 2% that pay out at the final of the tenure is not compounded? not exactlyreferring to illustration in post #4844 if base interest = daily compounded bonus interest amount = base interest amount which means bonus interest = daily compounded RM 10,000 x 2% / 365 ~ RM 0.55 RM 0.55 x 90 = RM 49.50 it may appear as simple interest but the rounding return RM 49.50 > compound return RM 49.44 QUOTE(cossie @ Dec 8 2025, 07:46 PM) does the 3 months bonus pocket seem like a 2% p.a. multiplied by 2 for the 'hibah'? yeah, because the 3-month bonus interest coincides with base interest 2% cossie liked this post

|

|

|

Dec 12 2025, 11:19 AM

|

Junior Member

919 posts Joined: Aug 2009 |

May I check if it’s worthwhile to use the GX card to pay for overseas hotel accommodations? I usually use credit card to book via Agoda, but I noticed that booking directly thru the hotel’s official website gives a lower rate. I haven’t gone through the T&C yet, would like to ask:

1) Will there be any additional charges if I book and make the partial payment (30% deposit) using the GX card thru the hotel’s website? 2) As long as there is sufficient balance in my GX account, I can use up the money or is there any limit? I can find transfer & QR limit in my account, does this apply to the physical card as well? 3) Since I also need to withdraw cash for the trip + using the card for payment whenever possible, just unsure if it’s a good idea to use the GX card to pay for the hotel stay (cost quite a bit). Any insights would be greatly appreciated. |

|

|

Dec 12 2025, 02:03 PM

|

Senior Member

2,254 posts Joined: Aug 2005 |

QUOTE(starry-starry @ Dec 12 2025, 11:19 AM) May I check if it’s worthwhile to use the GX card to pay for overseas hotel accommodations? I usually use credit card to book via Agoda, but I noticed that booking directly thru the hotel’s official website gives a lower rate. I haven’t gone through the T&C yet, would like to ask: 1) Will there be any additional charges if I book and make the partial payment (30% deposit) using the GX card thru the hotel’s website? GX ZERO markups on exchange rates and ZERO hidden fees on overseas transactions. therefore, definitely its much better compared to CC 2) As long as there is sufficient balance in my GX account, I can use up the money or is there any limit? I can find transfer & QR limit in my account, does this apply to the physical card as well? Its all your money, there is no limit but of course you cannot use more than what you have in there. 3) Since I also need to withdraw cash for the trip + using the card for payment whenever possible, just unsure if it’s a good idea to use the GX card to pay for the hotel stay (cost quite a bit). Unlimited 1% cashback. Get cashback when you pay in-store with your GX Card overseas. But not sure is there a validity for this. Any insights would be greatly appreciated. |

|

|

Dec 13 2025, 05:42 PM

Show posts by this member only | IPv6 | Post

#4940

|

|

Junior Member

877 posts Joined: Feb 2022 |

QUOTE(leanman @ Dec 12 2025, 02:03 PM) Just spend last week in Japan, no CB |

| Change to: |  0.0171sec 0.0171sec

0.52 0.52

6 queries 6 queries

GZIP Disabled GZIP Disabled

Time is now: 16th December 2025 - 01:22 PM |

Quote

Quote