QUOTE(riceuball @ Oct 25 2020, 07:27 PM)

» Click to show Spoiler - click again to hide... «

Hi sifus, would really appreciate some advice here.

I purchase an investment-linked medical insurance plan from GE for RM210/month at the beginning of this year before I turned 24yo. AL ~1.3mil, no lifetime limit, sum assured 50k until age 90. Below is the breakdown for reference:

SMARTPROTECT ESSENTIAL 3

IL CRITICAL ILLNESS BENEFIT RIDER

IL PREMIUM WAIVER EXTRA RIDER

SMARTMEDIC XTRA

SMART EXTENDER 120K (R&B200)

I went for a lower sum assured as I currently have no dependents and 50k is enough for my family to pay off my student loans. My priority was to get a good medical plan while I'm young and don't think about it IMO. However, just recently my insurance agent has been promoting a CI rider that is allegedly the only CI plan in the market that provides multiple pay-outs up to 8 times, including early, intermediate and advanced stages. I believe it's called Smart Multi Critical Care?

Okay so the thing is, I'm interested in this plan however it will be another RM150/month for 150k sum assured. To me it's absurd to be paying a total of RM360/month for my age. I asked my agent if it's possible to drop the CI benefit rider and replace this instead however they told since I locked this 50k "earlier", it's better to buy as a separate plan instead of withdrawing my rider, i.e. if I want my sum assured to be 200k, they recommend topping up 150k and keep the old rider. They also said if I were to make any changes to my current plan, the premium price might increase due to my age (I've turned 24yo) and the waiting time will be refreshed. I honestly doubt that the premiums will increase significantly because to me, it seems redundant to pay for a second ILP plan, wouldn't I be paying more insurance charges as well?

Also, I kinda regretted buying this insurance plan because few months into my job, I found out that my company's group insurance provides an opt-in deductible medical plan on top of our current existing medical plan, and it provides coverage even after I left the company with deductible waived after I reach retirement age. The employee benefits also included Life term insurance and it's higher than what I have for my personal plan lol. Only downside is that the max. renewal age for the group medical plan is 79yo. If I knew about this earlier I would have not purchased my personal insurance so early and would only get one medical/life term insurance after I reached my 30s as a backup.

I raised these concerns to my agent but y'know, they told me to keep my personal insurance because it's a waste to surrender or change bla bla bla, and it's good to buy early because I'm still young with no pre-existing illness

1) Should I keep my current personal plan and reduce the sum assured for the Smart Multi Critical Care for lower premiums? If so, should I insist on removing the CI benefit rider? Is Smart Multi Critical Care really necessary for my age at all?

2) Should I consider purchasing the additional group insurance scheme and lower my current plan's AL to reduce premiums? I know standalone medical plans will increase more as compared to ILPs but will it be the same for group insurance schemes?

3) Would it be better for me to opt-in for the group insurance scheme, surrender my current plan and only get one when I'm in my 30s? Yes the premiums will be higher by then but at that age, I will be more financially well to afford it right? I would have also saved more over the years by paying lesser premiums, right...?

Fyi I'm a 24f, single, non-smoker. Sorry for the long essay but I feel really lost right now

you came to right place to ask this.

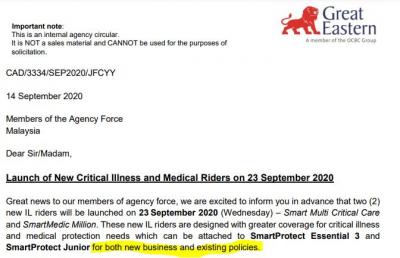

1a) You mentioned that you bought your plan SPE3 early this year. So, this SMCC was only launched in September this year. FYI, your agent is "BS-ing" you. You dont need to purchase a separate SPE3 to add on to the SMCC. purchasing another plan of course will be more costly. it's like buying 2 quarter chicken set from nandos but why should you when you can just order half chicken? So, what your agent didn't tell you is, you can just add SMCC to your current plan. there is NO DOWNSIDE at all on doing so.

i repeat no DOWNSIDE. You can keep your current CI Benefit rider AND just add on SMCC at 150k or 200k (not sure which amount you want). Of course, when you add the rider, unlikely it will be RM210 per month. Maybe RM250 per month or more but definitely not gonna reach 360 per month at your age. if yes, please come back and report here. email and complaint to GE

. IF your agent insist on you purchasing another plan, just write email to GE to complaint.

Since you didn't cancel anything, THERE IS NO refresh of waiting time. Everything else is still as per previous policy. It's like ordering a 3rd scoop of ice cream to add-on to your 2 scoop ice cream with waffle. the 2 scoop with waffle is still fine and sudah makan already. you didnt cancel the waffle.

You are right to doubt that premium will increase significantly at your age (read my earlier paragraph) AND yes it will be redundant to pay for another ILP policy. You dont exactly pay more insurance charges per se because insurance charges is based on the coverage amount you have selected. HOWEVER, each ILP policy comes with a policy fee. So if you buy 2 policies, you get charged double the policy fee.

1b) Is SMCC necessary? i would say early critical illness coverage is important, i won't call it necessary but that's based on my own person history. i know someone whose family has a history of breast cancer. to her, she believes it is necessary. the normal CI coverage, is too hard to claim, it's like super serious only then you will get the money. which is why GE comes up with product like this (and many other insurance companies too).

2) lowering AL (ie removing smart extender and/or lowering the coverage from R&B200 to 150) unlikely to bring a lot of savings but there will be savings. just fyi. group insurance scheme is always going to be cheaper but i'm not too familiar with the T&C and price to comment. i'm guessing this one is from Syarikat Takaful Malaysia Berhad, was in THE SUN newspaper sometime ago when i used to pick up the paper.

the group plan probably has a deductible because they assume you already have your own coverage from employee benefit. NOW, if you opt for this and cancel your current medical plan coverage, there's a few issues to take note

a) can you continue to stayed employed (i assume your employer is providing the medical coverage up to the deductible amount which is why they are promoting this to the staff) or can you afford to pay the deductible amount on your own? if either of the answer is yes, then you MAY save some money by buying this "group" plan

b) you mention the deductible will be waived when you retire. What is the retirement age? What if you retire earlier? How much is the premium you have to pay if and when you retire? (i'm not looking for the answer to these questions but you should, because it matters)

c) since this is group insurance plan, who will assist if you need to make a claim?

Summary to answer Q2: you need to spend time to calculate how much you may save and how much you may gain from these but i'm not getting paid to do it. so you gotta figure out certain things on your own.

3) What you think is correct, to a certain extent but i dunno the price. So, how much savings again? There will be few issues to take note

a) the group insurance plan covers medical only and some life coverage (as mentioned by you). NO CI coverage if you surrender your current plan

b) if for whatever reason (i know the chances is low but it's not zero) that you may have some condition from now until you are 30+, maybe the insurance companies wont open their doors to you to let you purchase the insurance policy. i agree there's savings but there's no free lunch in this world, you are giving up something too.

your Question 1 is easier to answer and there's a clear solution (just need to show your angry face to your agent) and dont kena tipu by your agent. Just show the attachment i have attached to your agent if he insist that you buy another policy. i repeat, attach SMCC to your existing policy, NOT buy new policy.

Q2 and 3, i dont know much on group plan harder to comment.

Attached thumbnail(s)

Oct 22 2020, 03:03 PM

Oct 22 2020, 03:03 PM

Quote

Quote

0.0348sec

0.0348sec

0.64

0.64

6 queries

6 queries

GZIP Disabled

GZIP Disabled