Aug 3 2021, 11:15 AM

Aug 3 2021, 11:15 AM

QUOTE(PortgasDerekAce @ Aug 3 2021, 12:36 AM)

sounds scary

QUOTE(PortgasDerekAce @ Aug 3 2021, 09:35 AM)

what happen when we dont get the projected return? we get less? get nothing? lose capital?

QUOTE(PortgasDerekAce @ Aug 3 2021, 10:48 AM)

if i understand you correctly it is possible to get less/get nothing/lose capital in simple?

right?

what happen when we dont get the projected return? we get less? get nothing? lose capital?right?

if you are refering to Simple,...then YES to all your probabilities...

we get less?

if it did not hit the projected returns,...then YES, we will get less (than the projected returns)

get nothing?

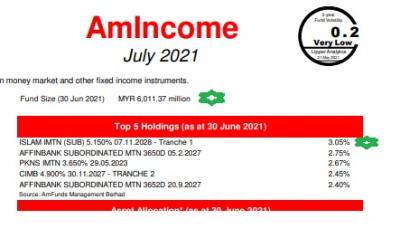

since Simple put our money in Amincome fund and this fund hold xx% of debt papers, in the event of exception of unforeseeable circumstance, there is a rating downgrade of a debt paper, the price of it may fall, thus the NAV will fall too, BUT but since the other holdings of the fund are still getting income, and if the total income obtained from others are equal to the value of fall in the value of the debt paper, then there will be no gain, thus YES, we will get nothing

lose capital?

since Simple put our money in Amincome fund and this fund hold xx% of debt papers, in the event of exception of unforeseeable circumstance, there is a default of a debt paper, thus the NAV will be impacted, BUT but since the other holdings of the fund are still getting income, and if the total income obtained from others are less than the value of defaulted value of the debt paper, then there will be losses to that fund, thus YES, we will lose capital.

Quote

Quote

0.0324sec

0.0324sec

0.38

0.38

6 queries

6 queries

GZIP Disabled

GZIP Disabled