QUOTE(DragonReine @ Apr 30 2021, 01:34 PM)

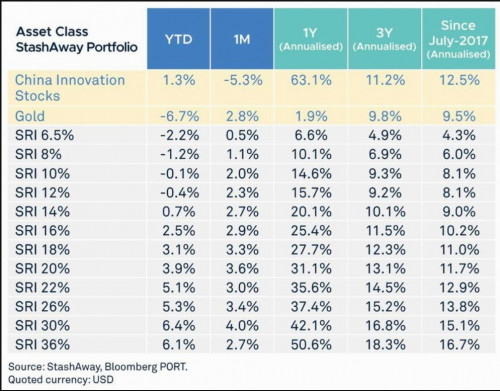

Returns for each SRI vs Asset Class, as of 28 April 2021

Investment StashAway Malaysia, Multi-Region ETF at your fingertips!

|

|

Apr 30 2021, 01:43 PM Apr 30 2021, 01:43 PM

Show posts by this member only | IPv6 | Post

#13941

|

Senior Member

1,617 posts Joined: Mar 2020 |

QUOTE(DragonReine @ Apr 30 2021, 01:34 PM) Returns for each SRI vs Asset Class, as of 28 April 2021 |

|

|

|

|

|

Apr 30 2021, 02:07 PM

Show posts by this member only | IPv6 | Post

#13942

|

Senior Member

2,437 posts Joined: Sep 2016 |

QUOTE(thecurious @ Apr 30 2021, 01:43 PM) Do you know why is there a separate category for Gold and China? i think SAMY just wanna highlight that the short term fluctuation (noise) is nothing n dun panic, try observe it in long term scenario ....hope my guess is right  full article here Why you should stay invested: China’s economy is rebounding, while protective assets insure your portfolio against any short-term volatility. https://www.stashaway.sg/r/chinas-tech-crac...letterApril2021 This post has been edited by ironman16: Apr 30 2021, 02:08 PM Quazacolt, DragonReine, and 1 other liked this post

|

|

|

Apr 30 2021, 02:13 PM

|

|

Junior Member

85 posts Joined: Jan 2009 From: bp - pontian |

Hi all, I just want to get your guys opinion about

which investment I should withdraw for my marriage expenses. Currently I have 57k in Asb (no loans) and around 24k in stash away portfolio. My original plan is to use stashaway portfolio, or better use ASB due to lower return ? I need around 25k maybe. Thank you in advance. |

|

|

Apr 30 2021, 02:28 PM

Show posts by this member only | IPv6 | Post

#13944

|

|

All Stars

14,909 posts Joined: Mar 2015 |

QUOTE(necrox77 @ Apr 30 2021, 02:13 PM) Hi all, I just want to get your guys opinion about My guess is, if your comparison is "due" to lower returns, and your SA has higher returns expectations, then redeeming ASB is a better option.which investment I should withdraw for my marriage expenses. Currently I have 57k in Asb (no loans) and around 24k in stash away portfolio. My original plan is to use stashaway portfolio, or better use ASB due to lower return ? I need around 25k maybe. Thank you in advance. But if you don't like the price volatility of SA but preferred the lesser volatility of returns expectations, then redeeming SA is a better option |

|

|

Apr 30 2021, 03:02 PM

Show posts by this member only | IPv6 | Post

#13945

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(thecurious @ Apr 30 2021, 01:43 PM) Do you know why is there a separate category for Gold and China? Basically explanation of proof why SAMY decided it was good idea to implement the 20% gold ETF into all portfolios, and showed how especially for portfolios heavily weighted with KWEB, gold allocation managed to reduce the impact of KWEB volatility. KingArthurVI and thecurious liked this post

|

|

|

Apr 30 2021, 03:15 PM

Show posts by this member only | IPv6 | Post

#13946

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(necrox77 @ Apr 30 2021, 02:13 PM) Hi all, I just want to get your guys opinion about if me, and I'm less than 35 years old, I'll take 20k ASB and 5k SAMYwhich investment I should withdraw for my marriage expenses. Currently I have 57k in Asb (no loans) and around 24k in stash away portfolio. My original plan is to use stashaway portfolio, or better use ASB due to lower return ? I need around 25k maybe. Thank you in advance. if more than 35, 10k ASB and 15k SAMY one extra factor: Am I on ASB financing and I'm relying on dividends from ASB to service the financing? Then I won't take more than the minimum to allow ASB dividends to cover the financing instalment   This post has been edited by DragonReine: Apr 30 2021, 03:17 PM |

|

|

|

|

|

Apr 30 2021, 04:07 PM

|

Senior Member

3,117 posts Joined: Jul 2005 From: Penang |

QUOTE(DragonReine @ Apr 30 2021, 01:34 PM) Returns for each SRI vs Asset Class, as of 28 April 2021 In the short term its hard to see the bond heavy portfolio getting any better but I will not bet against a bear market appearing at any time, and it will, and there will little warning of this. Its only really up to the investor to choose his poison and drink it. I'm always bullish and there is always a bull market somewhere. As long as my epf and other FI instruments stay steady (sspn, mmf) I see no reason to tilt towards debt investing. ChessRook liked this post

|

|

|

Apr 30 2021, 04:46 PM

|

|

Senior Member

3,117 posts Joined: Jul 2005 From: Penang |

QUOTE(necrox77 @ Apr 30 2021, 02:13 PM) Hi all, I just want to get your guys opinion about If you are non bumi. Sell all your stashaway or most of it. It's OK you can build back later. Asb for non bumi cannot replenish easily or even at all nowadays.which investment I should withdraw for my marriage expenses. Currently I have 57k in Asb (no loans) and around 24k in stash away portfolio. My original plan is to use stashaway portfolio, or better use ASB due to lower return ? I need around 25k maybe. Thank you in advance. If you are bumi then actually try to maintain your original portfolio balance. If you meant to have 60:30 and comfortable with it why change the composition at all? Ie sell both and maintain the ratio. |

|

|

Apr 30 2021, 04:58 PM

Show posts by this member only | IPv6 | Post

#13949

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(lee82gx @ Apr 30 2021, 04:07 PM) Thanks for showing this.It proves what I was blabbering on about bond and low risk portfolio mixes. But I bet you there will still be folks diworseifying with low risk funds after seeing this chart. Many think it's low meaning its cheap. Well it's cheap for a reason. IMO the low SRI of less than 10% SRI are somewhat pointless in Malaysian context because of two main things:In the short term its hard to see the bond heavy portfolio getting any better but I will not bet against a bear market appearing at any time, and it will, and there will little warning of this. Its only really up to the investor to choose his poison and drink it. I'm always bullish and there is always a bull market somewhere. As long as my epf and other FI instruments stay steady (sspn, mmf) I see no reason to tilt towards debt investing. 1) Malaysians already have access to low risk passive investment instruments locally (EPF, SSPN, ASB/ASM) 2) Malaysia having a weak and unstable currency. In SASG probably different because low interest rate environment there and a stable currency. But unless EPF ASNB SSPN all fail sekali, no reason to invest in those low SRIs unless you REALLY dislike giving money to government-controlled investment fund houses Gwynbleidd and Takudan liked this post

|

|

|

Apr 30 2021, 05:07 PM

|

Senior Member

736 posts Joined: Sep 2010 |

QUOTE(DragonReine @ Apr 30 2021, 04:58 PM) IMO the low SRI of less than 10% SRI are somewhat pointless in Malaysian context because of two main things: all rack up to 36% 1) Malaysians already have access to low risk passive investment instruments locally (EPF, SSPN, ASB/ASM) 2) Malaysia having a weak and unstable currency. In SASG probably different because low interest rate environment there and a stable currency. But unless EPF ASNB SSPN all fail sekali, no reason to invest in those low SRIs unless you REALLY dislike giving money to government-controlled investment fund houses |

|

|

Apr 30 2021, 05:27 PM

|

Senior Member

6,427 posts Joined: Jan 2003 From: Autobiography!!! |

QUOTE(PPZ @ Apr 30 2021, 05:07 PM) all rack up to 36% As long as KWEB is hedged by GLD it will be stable and the portfolio should not tank more than 18% overallLooking at RM it is better to buy USD now and wait q3 momo trends riding in  |

|

|

Apr 30 2021, 06:06 PM

Show posts by this member only | IPv6 | Post

#13952

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(PPZ @ Apr 30 2021, 05:07 PM) all rack up to 36% 22% SRI cukup dah for most |

|

|

Apr 30 2021, 06:40 PM

|

|

Senior Member

3,117 posts Joined: Jul 2005 From: Penang |

QUOTE(DragonReine @ Apr 30 2021, 04:58 PM) IMO the low SRI of less than 10% SRI are somewhat pointless in Malaysian context because of two main things: You are a man after my own heart. 1) Malaysians already have access to low risk passive investment instruments locally (EPF, SSPN, ASB/ASM) 2) Malaysia having a weak and unstable currency. In SASG probably different because low interest rate environment there and a stable currency. But unless EPF ASNB SSPN all fail sekali, no reason to invest in those low SRIs unless you REALLY dislike giving money to government-controlled investment fund houses 1. Yes 2. Probably. But remember whether samy or sasg. Both go with igov, bndx, and emb. If anything they are various currency in there. If myr drops they usually rise as they are finally priced in USD. Spore also has CPF. The most logical reason why people invest in low sri is people like to buy things they don't know. Then, investment books always prescribed 60 equity : 40 bonds, but investors don't know this is for americans who don't have epf, and have very very low savings rate. Also US folks are buying mostly municipal bonds which are not callable and have low risk of default. Not a single thing is applicable to Malaysian when it comes to the bond thesis. We should buy bonds in bear market for the alpha, pretty much that's it. Including bonds in portfolios also does wonders for the Sharpe ratio of a fund, thus it reduces the so called value at risk. And reduces the max drawdown etc. However you always sacrifice returns, unless years of very bad bear markets (again). So this is why I urge you guys, run the backrest, play with the allocations. See the drawdown length and amounts, factor in 1% annual fee compounded. Then ask yourself which one is actually suitable for you. |

|

|

|

|

|

Apr 30 2021, 09:01 PM

Show posts by this member only | IPv6 | Post

#13954

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(lee82gx @ Apr 30 2021, 06:40 PM) Then, investment books always prescribed 60 equity : 40 bonds, but investors don't know this is for americans who don't have epf, and have very very low savings rate. Also US folks are buying mostly municipal bonds which are not callable and have low risk of default. Not a single thing is applicable to Malaysian when it comes to the bond thesis. The problem with a lot of investing advice blindly repeating the 60:40 advice is that it's based on data from WEIRD (Western educated, Industrialised, Rich, and Democratic) demographics of people, especially American demographics which are very skewed and not applicable to a lot of countries where there are built in economic safety nets from government and/or benefits like healthcare etc.The fact of Malaysians is, generally speaking, we have pretty decent social security in the form of EPF/ASNB/SSPN with a somewhat underdeveloped economy that has room to grow, so if you are earning well enough to have the spare money to invest, you're already contributing regularly to EPF/ASNB/SSPN, and you're young + are aiming for growth rather than preservation + are willing to tolerate risk, then when it comes to self investing for retirement specifically, one should ideally aim for equities-heavy portfolio. This post has been edited by DragonReine: Apr 30 2021, 09:06 PM Gwynbleidd, encikbuta, and 2 others liked this post

|

|

|

May 1 2021, 01:56 PM

|

Junior Member

42 posts Joined: Nov 2015 |

hi, how many portfolio u guys have? I have 18% and 36%, issit better to migrate my 18% portfolio into 36%?

Seems like 36% portfolio have better return in long term...  |

|

|

May 1 2021, 01:59 PM

Show posts by this member only | IPv6 | Post

#13956

|

|

All Stars

14,909 posts Joined: Mar 2015 |

QUOTE(fulltimekiller86 @ May 1 2021, 01:56 PM) hi, how many portfolio u guys have? I have 18% and 36%, issit better to migrate my 18% portfolio into 36%? Seems like 36% portfolio have better return in long term...  but this 36% portfolio will generally comes with higher volatility in the short term but this 36% portfolio will generally comes with higher volatility in the short term  |

|

|

May 1 2021, 02:06 PM

|

|

Junior Member

42 posts Joined: Nov 2015 |

QUOTE(MUM @ May 1 2021, 01:59 PM) but this 36% portfolio will generally comes with higher volatility in the short term will DCA weekly MUM liked this post

|

|

|

May 1 2021, 02:12 PM

Show posts by this member only | IPv6 | Post

#13958

|

|

All Stars

14,909 posts Joined: Mar 2015 |

QUOTE(fulltimekiller86 @ May 1 2021, 02:06 PM) ya, but i aim for long term investment will DCA weekly   Good for you Good for you |

|

|

May 1 2021, 03:03 PM

|

|

Senior Member

3,117 posts Joined: Jul 2005 From: Penang |

QUOTE(fulltimekiller86 @ May 1 2021, 02:06 PM) ya, but i aim for long term investment You already have your own answer no? will DCA weeklySetting aside the more bond heavy issue, 18% has some different asset classes than 36% for the equities part. And definitely the impetus is on KWEB here which is considered the highest risk among the components. If you think hey, Chinese Internet companies sure more huat then go for 36%. Otherwise scale back down.....sorry my choice could be different from your choice. I can purchase more kweb directly diy, so I prefer those without it. Or less of it. Put it in another way I got greedy last time and I already have a big allocation that is underperformed already. |

|

|

May 1 2021, 03:36 PM

|

|

Senior Member

3,117 posts Joined: Jul 2005 From: Penang |

https://www.marketwatch.com/story/investing...more-2020-06-22

Even the guru of 60/40 is now saying it's not wise anymore and it's coming into negative returns ( my own bind funds certainly indicate so.) |

| Change to: |  0.0536sec 0.0536sec

0.45 0.45

6 queries 6 queries

GZIP Disabled GZIP Disabled

Time is now: 11th December 2025 - 03:52 AM |

Quote

Quote