QUOTE(jimmy.soo @ Jan 15 2014, 12:59 PM)

And I seek advises/recommendations from the pros here

Is it good to hold all of them? I have not much to start off actually, holding more or less (which is better)?

There is no short answer to your question without repeating all my previous posts. So maybe the best advice would be start by reading the previous pages, and then maybe some in other financial website and/or threads in this website, so that we can assumed you have the basic, fundamental facts and concepts; and the charges/fees (the cost/expenses in any investments).

To begin with, you need to know what is your financial objective in putting your savings in mutual funds. Then read the posts with this objective in mind and see whether it is applicable to your situation. There is much difference in savings for, say, 5-10 years for a around-the-world trip, than putting aside savings for 10-20 years for retirement.

Not many people start off with a huge sum (and it is not necessary to wait till there is a pile of money before investing), but it is crucial to know the destination, the financial goal.

1. Estimate how much the final total you will invest.

2. Take a look at a previous post on the Supreme Buy-and-Hold Portfolio Model.

3. The model suggests no more than 5% in any one fund. In general, it is advisable not to have more than 10%.

4. Now, calculate how much is 5% to 10% of the estimated final total you have in mind.

5. Then purchase (using Dollar Cost Averaging method) till that 5-10% limit before diversifying into another fund.

(This is assuming that you can barely meet the initial RM1000 investment into a new fund; and follow up with regular DCA purchases.)

Cheers.

PS. Investing can be emotional; and the kiasu-ness in me makes me think that I'm losing something if I'm not holding the top fund with the best returns. But there is a cost in switching from fund to fund every year in hunting for the best fund. So how? Hold all of them la.

Jan 14 2014, 10:15 AM

Jan 14 2014, 10:15 AM

Quote

Quote

helps needed here to analyse.

helps needed here to analyse.

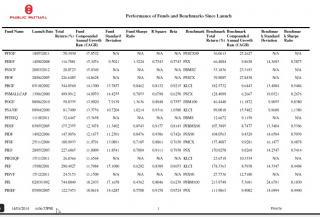

mind one lousy recommend me purchase PBIEF and ever since i bought the fund seem keep decreasing none stop

mind one lousy recommend me purchase PBIEF and ever since i bought the fund seem keep decreasing none stop

0.0308sec

0.0308sec

0.53

0.53

6 queries

6 queries

GZIP Disabled

GZIP Disabled