Oct 5 2008, 05:36 PM, updated 16y ago

Oct 5 2008, 05:36 PM, updated 16y ago

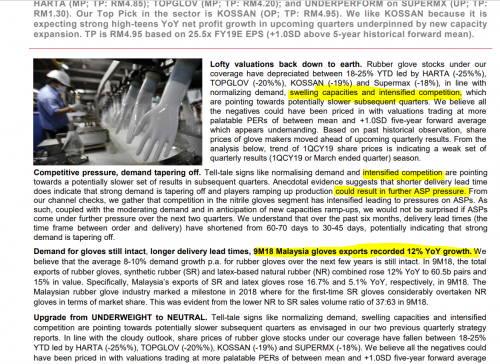

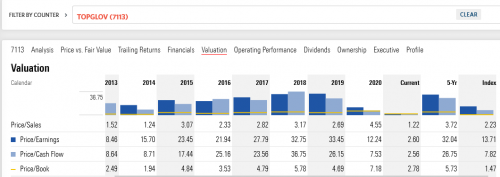

I studied her financial statement found this counter is jet-speeding in growth from the past 6 years.

1) Sales 44%

2) Profit after tax 39%

2) EPS growth 34%

3) Nett Assest 32%

4) Cash grow 60%

People suggested that her fair value should be around triple of current price at RM4 which is about RM12+. Is it too good to be true ? How come the transaction volumn is so low ? I think it is neglected.

What all sifus comment here ?

This post has been edited by rayloo: Nov 16 2008, 02:38 PM

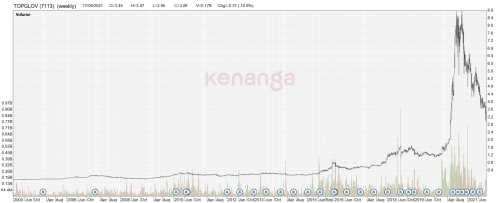

Top Glove 7113, High speed growth

Quote

Quote

will it be better to put your money in FD??

will it be better to put your money in FD??

Hmm....making sense...O.K, keep an eye on it.

Hmm....making sense...O.K, keep an eye on it.

to RM 9 that time and I had no bullet to masuk

to RM 9 that time and I had no bullet to masuk

0.2690sec

0.2690sec

0.32

0.32

6 queries

6 queries

GZIP Disabled

GZIP Disabled