QUOTE(prescott2006 @ Apr 5 2020, 12:15 PM)

Ya, I know that. But 4% PrivilegeSaver is > 3.75% interest. I know the saving might be little, but heh free money right. 😆

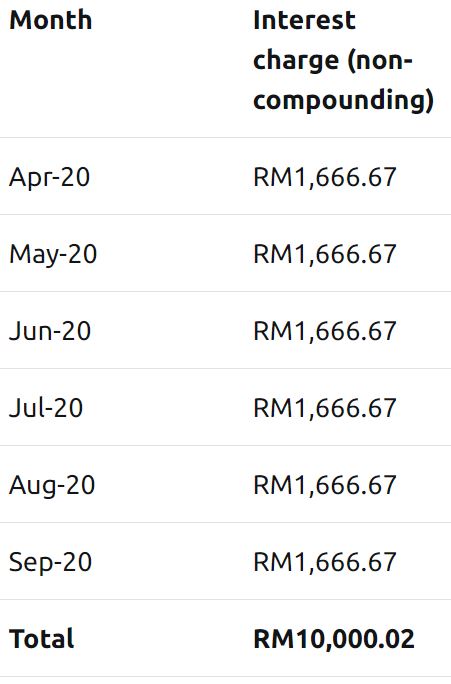

Using RP example of principal amount of RM 500k with loan interest of 4% and monthly repayment is RM 2390.52.

At end of September, your accrued interest is RM 10,000.02.

Let's say you're to divert the 6-month repayment into PSA, the total amount is RM 14343.12.

The total interest earned at 4% is RM 167.92 for the period from 1/4/2020 to 30/9/2020.

| April 2020 | 2390.52 | 7.86 |

| May 2020 | 2390.52 | 16.24 |

| June 2020 | 2390.52 | 23.58 |

| July 2020 | 2390.52 | 32.48 |

| Aug 2020 | 2390.52 | 40.61 |

| Sep 2020 | 2390.52 | 47.16 |

| | TOTAL | 167.93 |

Worth it?

And where is the free money comes from?

Your housing loan is still accruing interest (not no interest at all).

This post has been edited by GrumpyNooby: Apr 5 2020, 12:40 PM

Apr 3 2020, 07:53 AM

Apr 3 2020, 07:53 AM

Quote

Quote

0.0255sec

0.0255sec

0.28

0.28

6 queries

6 queries

GZIP Disabled

GZIP Disabled