QUOTE(neo-spider @ Feb 3 2012, 11:03 PM)

Thank Mr. WongMunKeong

.

Yes, the mutual funds are not via EPF cause I don't think they are a good deal. I mean typical EPF interest is about 5%, plus the 3% service charge when you buy the fund, means you need the fund to at least increase by 8% before you break even. Correct me if I'm wrong.

The fact is I'm not a crazy money saver guy, I don't spend much money socially (drinks, clubbing etc) but I have all those recent gadgets (HTC sensation, Ipad 2, xbox360, ps3, computer, big TV etc). It just that bonus from my current company is quite good to cover all those crazy expenses these few years.

I was not doing so well in the investment last year due to massive drop in Public Mutual Equities, manage to switch to bond before I was bled to death but still lose some money there. Luckily the bond was performing quite well last year (about 8%) to cover the lost in Public Mutual Equities. So currently looking for alternative place to invest the money. What do you think about buying properties in 2012? Or Foreign FD? Just to diversify a little bit.

Thank you.

Eh, no Mr Mr here to me pls. Surname = Wong, not Mr.

Ah - these savings / fun spending are inclusive of your bonus? Still good leh - it's near my own personal level of cash savings inclusive of bonus and you've got age/time & growth on your side. I'm a geezer comparatively

Well, your logic of EPF --> Mutual Funds needing 8%pa to break even isnt too right.

Note that that's just for the 1st year, U should take long term into consideration. Please note i'm NOT advocating U should move yr EPF into mutual funds k, just going to share some return i myself managed to eek out.

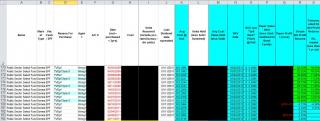

Below are snapshots of Equity funds i hold in Prudential SmallCaps + Public Sector Select Fund (PSSF)

& Bond fund Public Select Bond Fund. Please note i'm my own agent for Public Mutual, thus take the PSSF returns with a pinch of salt due to lowered cost of entry. For PSBF, agents dont get any of the 0.25% commissions (if i'm not mistaken).

Take a look see - worthwhile?

It's not ALL profits yar as U can see from the "untouched-up", other than amount and units lar, snapshots.

Take special note of Prudential's SmallCap which i paid FULL service charges. In those days, i think it was about 6%++.

Worthwhile? It depends on your own selection and methodology i guess. Heck, if U can handle gold's wild runs, this is sup sup water for U i think

U've just got introduced to Asset Allocation indirectly by your bond funds saving the day due to their exceptional returns these 1+ year

.

Properties? It's always a good time OR bad time to buy - it depends on your expertise in the area + target market. This is where specialization can eek out some great deals even in a high market. Personally, i'm not an expert in properties though i do have investment real estate. Just bought based on cost VS rental yield returns + location for easier land-lording.

I'd suggest U look into REITs as a start for diversifying into Real Estate asset class since REITs throws out dividends regularly and has upside potential due to its underlying properties going up in value and/or people chasing the REIT's stocks up. No issues of landlording nor lump sum locked-in BUT not much leverage (which can be a good or bad thing).

Foreign FD? not my cuppa unless my daughter identifies which country's Uni she's targeting - she's a wee bit too young to do that yet though hheheh. Reason = i'd rather own the assets generating the $, than just the $.

Phew - just a (many?) thought.

Jan 9 2012, 03:07 PM

Jan 9 2012, 03:07 PM

Quote

Quote

All that renovation costs....

All that renovation costs....

0.0347sec

0.0347sec

0.32

0.32

6 queries

6 queries

GZIP Disabled

GZIP Disabled