QUOTE(BrookLes @ Aug 30 2022, 09:57 PM)

RM are there just to sell you their stupid banking products that's all.

Trust me, most of them really are just there to earn your commission that's all.

Unless you are worth 10s of millions of dollars and you put money into goldman sachs or something.

But if you do not buy their stupid banking product, the RM dun even want to bother interacting with you or helping you.

That guy obviously dunno what he is talking about. Most people working in the finance sector really are almost useless unless they are really working in the inside. I am referring to the guy you just replied to.

But they think they are "smart" just because they know certain terms.

Do you have RMs? My RMs are ok, they offer me their products, i say no, they wont kacau me.

I say ok, they send me details and i bought, they happy me happy.

Cant say they only sell stupid products , who so stupid wanna buy?

Recently i bought the CIMB CIRA coupon rate 5.5% , paid 3 monthly

Bank Islam Bonds 5.16% , paid 6 monthly

Without RMs how to buy?

But i agree with you Ramjade sapu that MD without giving him face at all.

QUOTE(honsiong @ Aug 30 2022, 11:37 PM)

Whether its 1m, 6m, 12m, 60m... the compounded int rate is almost the same. If you think the int rate will rise just set 1-2 months term auto-renew for your FD.

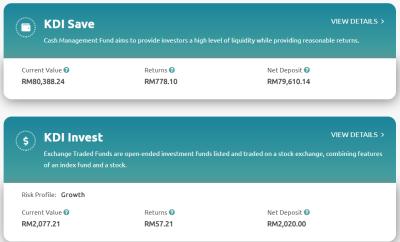

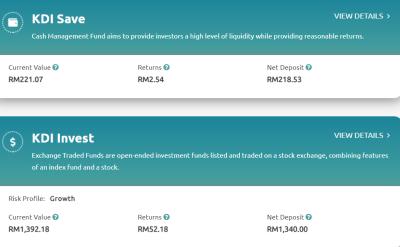

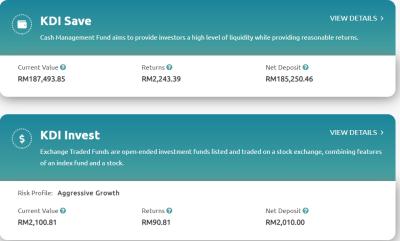

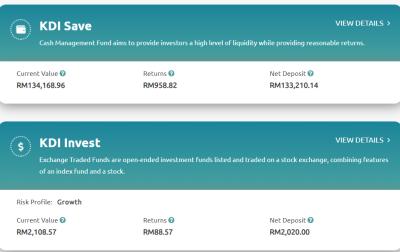

FD is almost always lower than MMF. When FD goes up, KDI save would have gone up also, likely.

Are you sure FD rate is almost always lower than MMF??

takda logik la Bro.

FD tie your money down , to get good rate must tie longer , withdraw kena cut back no interest.

MMF can withdraw any working day ,no penalty, especially pay daily interest type

So how can FD pay lower than MMF, everyone run to MMF lo like that.

as per my records, my FDs are always higher than MMF(PMMF, SA, Versa), KDI included.

Note KDI is not you usual MMF, and i doubt next year can maintain same 3%

l

Jul 8 2022, 11:05 PM

Jul 8 2022, 11:05 PM

Quote

Quote

)

)

0.0388sec

0.0388sec

0.62

0.62

7 queries

7 queries

GZIP Disabled

GZIP Disabled