Apr 30 2021, 09:01 PM

Apr 30 2021, 09:01 PM

QUOTE(lee82gx @ Apr 30 2021, 06:40 PM)

Then, investment books always prescribed 60 equity : 40 bonds, but investors don't know this is for americans who don't have epf, and have very very low savings rate. Also US folks are buying mostly municipal bonds which are not callable and have low risk of default. Not a single thing is applicable to Malaysian when it comes to the bond thesis.

The problem with a lot of investing advice blindly repeating the 60:40 advice is that it's based on data from WEIRD (Western educated, Industrialised, Rich, and Democratic) demographics of people, especially American demographics which are very skewed and not applicable to a lot of countries where there are built in economic safety nets from government and/or benefits like healthcare etc.The fact of Malaysians is, generally speaking, we have pretty decent social security in the form of EPF/ASNB/SSPN with a somewhat underdeveloped economy that has room to grow, so if you are earning well enough to have the spare money to invest, you're already contributing regularly to EPF/ASNB/SSPN, and you're young + are aiming for growth rather than preservation + are willing to tolerate risk, then when it comes to self investing for retirement specifically, one should ideally aim for equities-heavy portfolio.

This post has been edited by DragonReine: Apr 30 2021, 09:06 PM

Quote

Quote

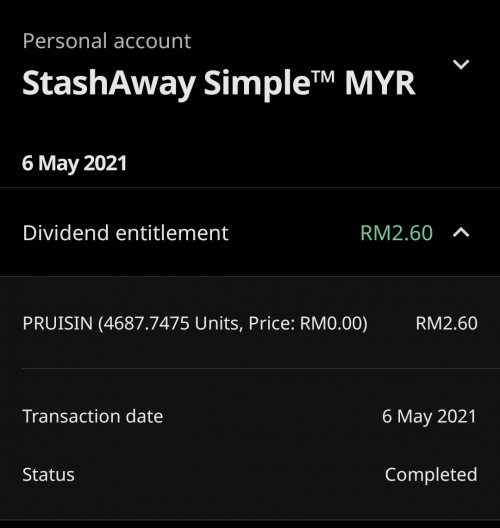

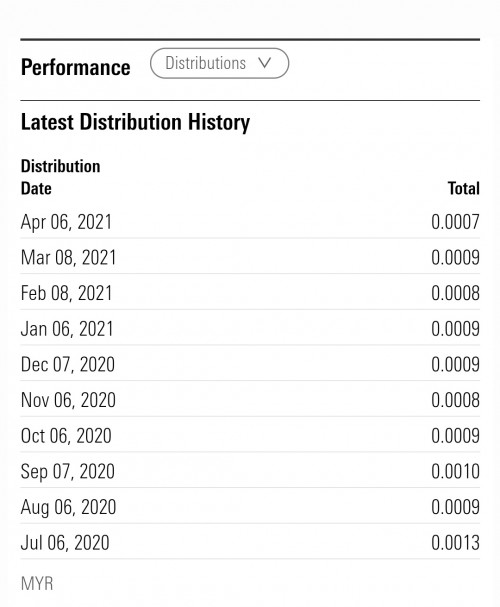

MMF dividends fluctuate, don't base entirely on SA's projected rates. PRUISIN is going on a downward trend at least for next few months while OPR remains low, following information from Morningstar:

MMF dividends fluctuate, don't base entirely on SA's projected rates. PRUISIN is going on a downward trend at least for next few months while OPR remains low, following information from Morningstar:

Similarly no one expected China to suddenly so swiftly clamp down on market enough to push those same stocks down.

Similarly no one expected China to suddenly so swiftly clamp down on market enough to push those same stocks down.

0.4220sec

0.4220sec

0.70

0.70

7 queries

7 queries

GZIP Disabled

GZIP Disabled