Apr 14 2019, 04:15 PM

Apr 14 2019, 04:15 PMQUOTE(SwarmTroll @ Apr 14 2019, 02:28 PM)

I see. I mean I would assume if you die it would usually be accidents no? Non-accident I am assuming things like terminal cancer, someone kills you (which I think its not an accident? LOL), killed while doing dangerous activities, etc...

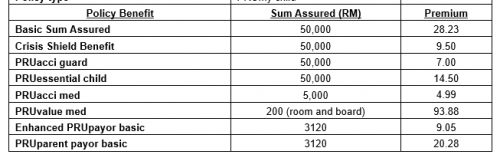

For ILP is it cheaper compared to traditional stand-alone if ILP has multiple bundles? Or is that not true? Generally the premium for ILP will be higher compared to traditional but if you do combo/bundle for ILP it is cheaper because of discounts given?

As posted before, treat it just like buying combo mean vs ala-carte.For ILP is it cheaper compared to traditional stand-alone if ILP has multiple bundles? Or is that not true? Generally the premium for ILP will be higher compared to traditional but if you do combo/bundle for ILP it is cheaper because of discounts given?

Combo - you see it "cheaper" but you need to buy more stuff and pay more.

Eg. buy a combo meal, you get burger + drink + fries = Rm15

Ala-carte - you see it more expensive, but you pay less.

Eg. Buy only burger = Rm10.

In the end of the day, for ala-carte, you have extra Rm5 in your pocket vs the "cheaper" for combo at Rm15.

So you can't say which is cheaper or worthwhile, it depends on the situation.

If you want to invest in UT + buy insurance, then ILP may be a good option.

But if not intended to invest in UT and has more flexibility in cashflow, then standalone may serve a good option.

Please be reminded, the UT portion in ILP, there may be around 5% sales charges incurred as well. And the UT may suffer losses instead gain, those projected return in the ILP proposal is based on previous years market track record, they do not guarantee future will be the same, it can yield a loss instead of gain, or a better gain than in projection in market condition is favourable.

ILP a more simple term = Unit trust (mostly equities) + insurance combo.

Quote

Quote

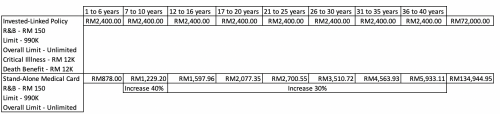

must have completed the comparison table to enable below comment.....(mind showing the table?...interested to find the truth)

must have completed the comparison table to enable below comment.....(mind showing the table?...interested to find the truth)

0.0272sec

0.0272sec

0.65

0.65

6 queries

6 queries

GZIP Disabled

GZIP Disabled