Hi sifus,

Sorry for the long post-

I'm new to insurance and I'm looking to get my first policy and been researching around:

Basic background, 24yo female, single, office job

QUOTE(hamjipeng @ Jun 8 2019, 10:43 AM)

1. Currently focusing on medical with higher coverage as main concern as medical costs are increasing day by day.

QUOTE(hamjipeng @ Jun 8 2019, 10:43 AM)

2. From what I understand, life is compulsory in all ILP plans so is it OK if I just get the minimum sum assured to stretch my ringgit? Is it necessary to get like 50k as per initial quotes by the agents(premiums of rm250/month)? Or maybe I can purchase separately in the future?

What you are referring to is the Sum Assured Multiple Allowable which is affected by the annual premium and the riders attached. Whether it is necessary to get RM50k depends on each company. QUOTE(hamjipeng @ Jun 8 2019, 10:43 AM)

3. Is it necessary/important for me to get CI? I understand that it is to act as income replacement, if the amount is like 50k, I would probably have savings around that amount too, not sure whether I need this rider? Or I can purchase a standalone for higher coverage in the future?

Whether it is necessary or important is up to you. Get an agent to do a Needs Analysis for your review. Also, when it comes to Critical Illness coverage do take note of the following:

- Survival Clause

- Type and stages of CI covered (Early to Advance or only Advance)

- Payout %

QUOTE(hamjipeng @ Jun 8 2019, 10:43 AM)

4. ILP are structured that cash value compensates the high COI in the future right? So if now I pay a larger portion of premium with less riders and moore allocation into the fund, the higher acc value will sustain longer and I'm less likely to receive letter for topup next time? My dad's family history has long age and healthy, so I'm looking to cover up to at least 80 yo.

You got it!QUOTE(hamjipeng @ Jun 8 2019, 10:43 AM)

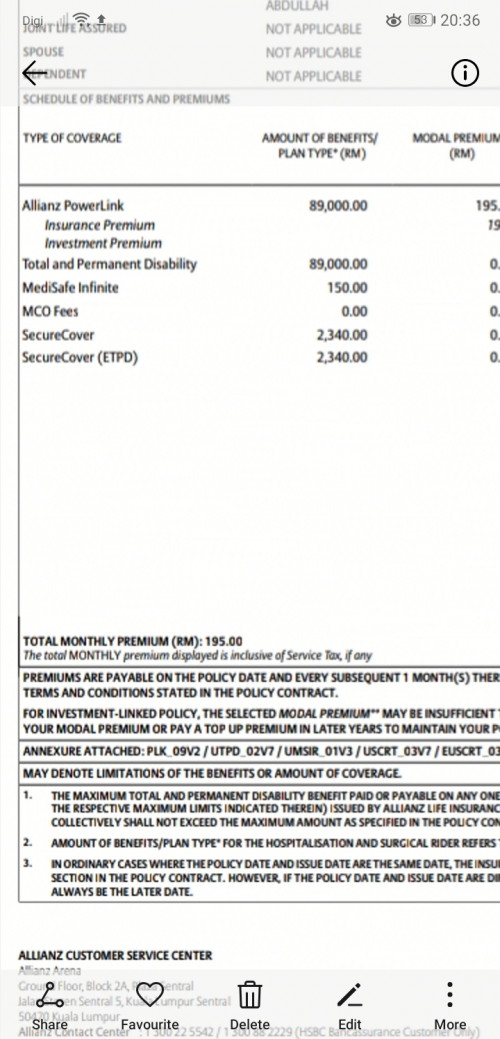

5. Had a comparison with all big 3 agents which I have tweaked a little to exclude the CI first, budget is around rm150-200:

Prudential-rm160 annual 1.38m coverage deductible 300, life/tpd 20k, Ci 20k, sustainability 64-72yo

GE-rm180, 50k life/tpd, 50k CI, coverage 90+900k no deductible (why separate?), sustainability 99 yo

AIA-rm186, life/tpd 10k, coverage 1.5m deductible 300, sustainability 100 yo

Let me throw in Allianz for your consideration:

- Life/TPD: RM5k

- CI (Early - Advance): RM100k

-- Cancery Recovery: RM35k

-- Diabetes Recovery: RM20k

-- Catastrophic CI: RM20k

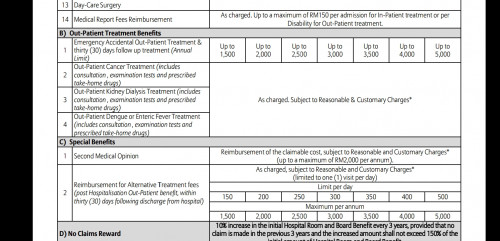

- R&B200 - Until 91 years old

-- Annual Limit: RM1mil

-- Lifetime Limit: None

- Waiver of Premium

RM196/month

Sustainability: 62 - 70 years old.

P/S: This quote is done based on your existing proposals.

PP/S: Suggest you get the full quotation for AIA and GE.

QUOTE(hamjipeng @ Jun 8 2019, 10:43 AM)

Appreciate if anyone could give some advice for my case.. Not sure whether I'm on the right track or I'm just cutting everything off to get the possible lowest premium lol...

You are on the right track. What you need to do next is a Needs Analysis where the agent will run through your risk and how they can manage the risk via insurance. Once you know what you need, then you can discuss premium. QUOTE(hamjipeng @ Jun 8 2019, 10:43 AM)

Now on to my dad and sis... Haha...

My dad is looking to upgrade his plan, 57yo, however he is pilot which is class 4 occupation quoted by all agents.

Current standalone plan is coverage 90k, 2k+/year, which will definitely increase up to 8k-10k+ in future.

He wants to get a medical card similar to mine, any ways to play around so he can get a lower quote? He has company insurance which is unlimited coverage currently and he wants to utilise personal insurance after retirement only. Health is definitely no problem also as their industry have very vigorous checkups half yearly and his family history is like very long age.

Given your dad's age and occupation he will be looking at a premium north of RM8k a year if he gets a medical card similar to yours. Once he retires, he can inform the insurance company and get his premium revised.QUOTE(hamjipeng @ Jun 8 2019, 10:43 AM)

For my sister, 19yo student, my mom intends to purchase a same medical as mine for her, however the concern is few years back then they went to KPJ for an xray because my sister's spine abit "senget", the doctor said 15 degrees and didn't suggest any treatment etc, just said 2yrs later can do a follow up which my sis nvr went back.. If want to buy now, need to declare? What are the risks? One agent suggested not to declare as it is small case only normal check up and if declare, they will definitely exclude spine related problems. My mom's concern is later if insurance company find out and reject her claims next time then my sis will not have insurance for the rest of her life..

One word. Declare. Then wait for deferment/offer from the company. If not satisfied with what you get, appeal. Your mum concern is very real in the sense that the insurance company has the right to void the contract.QUOTE(hamjipeng @ Jun 8 2019, 10:43 AM)

Appreciate the response on this long winded post..

Sorry and Thank you so much!

Apr 12 2019, 10:38 PM

Apr 12 2019, 10:38 PM

Quote

Quote

0.1349sec

0.1349sec

0.82

0.82

7 queries

7 queries

GZIP Disabled

GZIP Disabled