QUOTE

yeah still a good card in fact, but RM50 cash back other card can easily achieve, RM60 max only +10 and need spend RM2500+

SC JOP is because previously RM85 attractive

it still a good card..... for those who didn't actually do the transaction with BP for full CB. just that the CB cap from 85 drop to 60

QUOTE(cybpsych @ Jun 7 2019, 07:05 PM)

working atm/cdm list in post 1.

others, assume not able to.

even those from post 1, sometimes limited to notes availability.

of course can assume so but no 1 could 100% sure those not mentioned wasn't working as the way you want.

QUOTE

i dont think they can do so specially to BP. except BNM does allow. else it would just like an bias toward BP

QUOTE(cybpsych @ Jun 7 2019, 07:09 PM)

wrong to assume that.

you think everyone using JOP for bigpay exclusively?

it's simple as this: can you spend rm200 on petrol/autobill (insurance, mobile, utilities)?

if yes, 200 on those + the remaining 2300 can be loaded into bigpay as what you've been doing now.

yaya

QUOTE(tan_aniki @ Jun 7 2019, 08:45 PM)

sure can call for waive one, if can't waive then just cancel lo, the operator will plea you not to cancel by offering AF waiver in the end

most of the time yes..... but not for some of the time

QUOTE(sl3ge @ Jun 7 2019, 09:16 PM)

what if i call the operator say cant waive,

but the annual fee RM250 already charge in my bill,

and will the bank force me to pay?

because last time i apply a credit card,didnt activate it(regretted apply it),

few weeks later being charged RM25 sst,

i called CS say i dont want the card (since i didnt activate it),

but the CS insist i need to pay the sst eventhough i dont want the card and also havnt activate it.

Does the CS is right?

for SST part, the CS was right if not mistaken. as the SST was charged by government but not the bank. once they approved the card, it would be recorded into Credit Bureau

QUOTE(limeuu @ Jun 7 2019, 09:40 PM)

BNM rule is that sst will be charged the month after activation of card, or if not activated, on the 4th month after issuance of card....

thanks for sharing the knowledge

QUOTE(geekfiredog @ Jun 7 2019, 10:33 PM)

For those credit with annual fee (or uncertain AF waiver criteria), DO NOT use it for installment or balance transfer to the card - you are tying your own hands for the bank to decline your AF waiver request! Stop using the card before the card anniversary date (or a week or so before your statement date prior to expire month), then wait for the bank to charge AF and call to ask for waiver - cancel the card if the bank rejects your request.

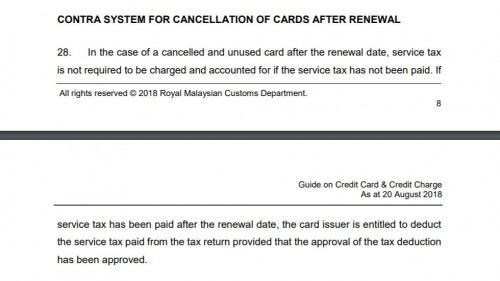

That was before the SST time, SST & GST are charged on the same date now. AF is easy to deal with (cancel card if can't waive) but SST is more complicated. "Service Tax 2018 : Guide on Credit Card" stated SST need not be paid if the card is unused after renewal date, and the bank is entitled to deduct from tax return if it has been paid. I've not done it personally to not paying SST if the card is not used after SST is charged - so no experience in dealing with banks on this yet. Maybe someone have done that before can share their experiences!

Service Tax 2018: Guide on Credit Card

Service Tax 2018: Guide on Credit Card1st time read on those SST guide. so this mean once it near to the renewal month and if i plan to waive the Annual Fee, then i shall stop using the card and try to call for Annual Fee waiver and cancel it if not waive with no SST (but still need to pay the annual fee right once it has been charged and go for call for waiver)

QUOTE(zenquix @ Jun 7 2019, 10:48 PM)

if you are working in Singapore, I recommend you open an account with both CIMB SG and CIMB MY. Via CIMB Clicks Singapore you can transfer from your CIMB Singapore account to your CIMB Malaysia account at very good rates (even better than Midvalley). Just don't make it your main account due to poor ATM coverage island-wide.

Ugh and I just got the card this month.

The RM30 cap online spending, as mentioned by others, is really not much of an issue. Just move RM200 spending to autobills and petrol and you can max out the RM60 cashback loading RM2300 to bigpay (until they declare quasi cash as non earning like Singapore).

The hurt is really the RM85 -> RM60 cap and non auto-waiver of AF. If AF is not waiveable, you are basically burning close to 5 months of max cashback for AF + SST

so this mean you actually can use it for foreign exchange and earn difference in exchange rate ? i mean it is possible right?

ya the CB cap hurt the most

May 18 2019, 09:13 AM

May 18 2019, 09:13 AM

Quote

Quote

Win-Win

Win-Win

didn't go try it out night haiz...

didn't go try it out night haiz...

0.0964sec

0.0964sec

0.62

0.62

7 queries

7 queries

GZIP Disabled

GZIP Disabled