QUOTE(turtle_onrage @ Feb 20 2017, 12:53 AM)

Hi, thanks for your advise! If i were to drop the bond fund, any recommendation of fund that can complete my portfolio? In terms of optimal diversification and good risk reward ratio. Thanks!

1) For a start you can follow the fsm recommended portfolio. To ignore the bond fund or not is up to you. I just think, you don't need it as a counter balance drag in a portfolio of 25 yrs time frame. Also a 10% "less volatile" bond fund in a portfolio will not do much to mitigate the risk of an aggressive portfolio that much. (for a portfolio drops of 10%, with a 10% FI fund in it ...it just dropped 1% less)

2) Then, you need to monitor yr portfolio during the bad times...yes the bad times like corrections. That is the only time you will really be able to feel it emotionally whether you can really continue with UT investment for the longer terns of 25 yrs.

These cycles of bad times will always return periodically with different intensity n duration. If you cannot stand the heat go for some other not so aggressive portfolio or just plain FD, nothing to be ashamed of or bad of it......as long as you can sleep peacefully during those bad times.

3) There is really no optimal portfolio or funds to have permanently. You need to monitor and drop it, exchange it, increase or reduce its allocations from time to time....1 way is follow the fsm star rating or recommended portfolio or funds. Ut investment is not a buy and forget for 25 yrs...

(just look at the number of changes made to the FSM recommended portfolios all these years, you will see, it is not a static affair)

4) what were suggested here in tis forum or by other professionals or fsm website is just a guide....you can start it then make adjustment along the way and yearly do a rebalancing check up.

Happy UT investing adventure....YES, it is to me an adventure. For i learnt, still learning, more be explored, feel, see n etc, etc. Just monitor the journey periodically and make provisions/corrections adjustment if necessary.

on this "any recommendation of fund that can complete my portfolio? In terms of optimal diversification and good risk reward ratio."......my suggestion or perhaps from others too may not be suitable to your likings or my or their likings too. What is now optimal may not be optimal few months later.......what was a good risk reward ratios may not look good few years later.....

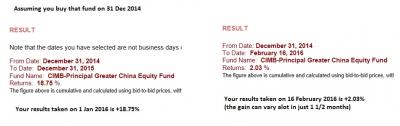

Do You Use Your Rear-View Mirror To Invest?

August 14, 2015

Extrapolating historical performance can sometimes be detrimental to investing; we suggest investors avoid relying too much on their “rear-view mirrors” when they invest.

Author : Fundsupermart

https://www.fundsupermart.com.my/main/resea...gust-2015--6172This post has been edited by T231H: Feb 20 2017, 08:10 AM

Feb 16 2017, 10:02 PM

Feb 16 2017, 10:02 PM

Quote

Quote

0.8089sec

0.8089sec

0.20

0.20

7 queries

7 queries

GZIP Disabled

GZIP Disabled