For me, a 'jump' is still required when the renewal term is coming soon.. what to expect when a person was admitted in 2017, but in 2018, when he needs to renew the policy, it becomes rather risky..

Insurance Talk V3, Anything and everything about insurance

|

|

Jan 11 2017, 04:50 PM Jan 11 2017, 04:50 PM

|

Senior Member

1,423 posts Joined: Aug 2010 From: Sarawak |

For my own personal view without bias to any insurance companies, in comparison with Lonpac which is using the General Insurance term, I still feel comfortable with insurance companies who are offering long term contracts in the insurance rather than renewing annually despite being told that the guaranteed renewal is applicable..

For me, a 'jump' is still required when the renewal term is coming soon.. what to expect when a person was admitted in 2017, but in 2018, when he needs to renew the policy, it becomes rather risky.. |

|

|

|

|

|

Jan 11 2017, 04:51 PM

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(smartinvestor01 @ Jan 11 2017, 04:50 PM) For my own personal view without bias to any insurance companies, in comparison with Lonpac which is using the General Insurance term, I still feel comfortable with insurance companies who are offering long term contracts in the insurance rather than renewing annually despite being told that the guaranteed renewal is applicable.. Then go with a life insurance company.For me, a 'jump' is still required when the renewal term is coming soon.. what to expect when a person was admitted in 2017, but in 2018, when he needs to renew the policy, it becomes rather risky..  |

|

|

Jan 11 2017, 05:11 PM

|

|

Senior Member

1,423 posts Joined: Aug 2010 From: Sarawak |

QUOTE(lifebalance @ Jan 11 2017, 04:51 PM) Then go with a life insurance company. Yape, thats my plan.. Anyway, thanks for the sharing and advise from you and anyone here.. Very much appreciated. |

|

|

Jan 16 2017, 12:08 PM

|

Senior Member

2,173 posts Joined: Jan 2012 From: Butterworth, Penang |

Brace yourselves this 2017, the medical cost of insurance is geared to be increased across the board...

This post has been edited by roystevenung: Jan 16 2017, 12:25 PM |

|

|

Jan 16 2017, 01:53 PM

|

Senior Member

3,812 posts Joined: Apr 2009 From: West Malaysia |

QUOTE(roystevenung @ Jan 16 2017, 12:08 PM) Brace yourselves this 2017, the medical cost of insurance is geared to be increased across the board... it is gonna be a tough year.. btw.. approaching 2500 posts.. ready for next version  |

|

|

Jan 21 2017, 09:43 AM

|

|

Junior Member

333 posts Joined: Apr 2008 |

Hello all sifus,

I have some questions about MRTA death claim because my father passed away three weeks ago and I'm in the midst of preparing the documents required. 1)My question is, is there anyone who claimed this before? I tried searching online and through lowyat and get many threads about MRTA vs MLTA instead. 2) One of the documents in the list is Letter of Administration which will take about two months to get done. Is it required by all banks? If so, why do they not put it in the list at their websites? 3) And according to the bank which the property is under loan, I still have to pay the loan while it is processed. Not that I don't want to pay but currently finances haven;t been all that good. And also another question which is under life insurance. How long does it take for a death claim? AIA quoted 3 weeks but I haven't heard from them yet. Online searches reveal it could take about two months to fully process, does it usually take that long? Sorry for the many questions and I hope sifus can patiently answer all of them.  |

|

|

|

|

|

Jan 21 2017, 10:13 AM

|

Senior Member

945 posts Joined: Jun 2012 |

QUOTE(lionelzc @ Jan 21 2017, 09:43 AM) Hello all sifus, Sorry to hear about your lost lionelzc, although death ends a life but it doesn't end a relationship.I have some questions about MRTA death claim because my father passed away three weeks ago and I'm in the midst of preparing the documents required. 1)My question is, is there anyone who claimed this before? I tried searching online and through lowyat and get many threads about MRTA vs MLTA instead. 2) One of the documents in the list is Letter of Administration which will take about two months to get done. Is it required by all banks? If so, why do they not put it in the list at their websites? 3) And according to the bank which the property is under loan, I still have to pay the loan while it is processed. Not that I don't want to pay but currently finances haven;t been all that good. And also another question which is under life insurance. How long does it take for a death claim? AIA quoted 3 weeks but I haven't heard from them yet. Online searches reveal it could take about two months to fully process, does it usually take that long? Sorry for the many questions and I hope sifus can patiently answer all of them. If there wasn't a will, the a Letter of Administration will be required. You can get in touch with the bank customer service you will definitely need to provide your father's death certificate. Until the entire processing from the bank is completed, the installment will need to be paid out. What you found out about the processing timing is about correct however you need to ensure all the documents are in order. Best, Jiansheng |

|

|

Jan 21 2017, 10:36 AM

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(lionelzc @ Jan 21 2017, 09:43 AM) Hello all sifus, 1. The mrta will be paid to the bank I have some questions about MRTA death claim because my father passed away three weeks ago and I'm in the midst of preparing the documents required. 1)My question is, is there anyone who claimed this before? I tried searching online and through lowyat and get many threads about MRTA vs MLTA instead. 2) One of the documents in the list is Letter of Administration which will take about two months to get done. Is it required by all banks? If so, why do they not put it in the list at their websites? 3) And according to the bank which the property is under loan, I still have to pay the loan while it is processed. Not that I don't want to pay but currently finances haven;t been all that good. And also another question which is under life insurance. How long does it take for a death claim? AIA quoted 3 weeks but I haven't heard from them yet. Online searches reveal it could take about two months to fully process, does it usually take that long? Sorry for the many questions and I hope sifus can patiently answer all of them. If there is any extra it will go to your father estate 2. Yes 3.it will take some time but normally within 3 weeks You'll have to service the mean while as it doesn't relief you immediately of your responsibility to service the loan while the insurance is processing for a payout |

|

|

Jan 21 2017, 11:05 AM

|

Senior Member

4,724 posts Joined: Jul 2013 |

Quick question, agents are allowed to represent 2 general insurance companies?

|

|

|

Jan 21 2017, 11:21 AM

|

|

Junior Member

333 posts Joined: Apr 2008 |

QUOTE(Holocene @ Jan 21 2017, 10:13 AM) Sorry to hear about your lost lionelzc, although death ends a life but it doesn't end a relationship. I see. If there wasn't a will, the a Letter of Administration will be required. You can get in touch with the bank customer service you will definitely need to provide your father's death certificate. Until the entire processing from the bank is completed, the installment will need to be paid out. What you found out about the processing timing is about correct however you need to ensure all the documents are in order. Best, Jiansheng Thanks QUOTE(lifebalance @ Jan 21 2017, 10:36 AM) 1. The mrta will be paid to the bank Okay....but I'm not sure the bank will give back the extra for MRTA insurance claim since the beneficiary is the bank.If there is any extra it will go to your father estate 2. Yes 3.it will take some time but normally within 3 weeks You'll have to service the mean while as it doesn't relief you immediately of your responsibility to service the loan while the insurance is processing for a payout Thanks |

|

|

Jan 21 2017, 11:29 AM

|

|

Senior Member

945 posts Joined: Jun 2012 |

QUOTE(adele123 @ Jan 21 2017, 11:05 AM) Quick question, agents are allowed to represent 2 general insurance companies? Ya. |

|

|

Jan 21 2017, 11:38 AM

Show posts by this member only | IPv6 | Post

#2472

|

Senior Member

801 posts Joined: May 2010 |

QUOTE(adele123 @ Jan 21 2017, 11:05 AM) Quick question, agents are allowed to represent 2 general insurance companies? YesUsually, they are the typically financial planner who represent a few insurance agencies. They might not be biased in giving out financial advises, just IMHO. This post has been edited by you90: Jan 21 2017, 11:39 AM |

|

|

Jan 21 2017, 11:45 AM

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(adele123 @ Jan 21 2017, 11:05 AM) Quick question, agents are allowed to represent 2 general insurance companies? Yes you're right QUOTE(lionelzc @ Jan 21 2017, 11:21 AM) I see. No it will be automatically entered to the person's estate so if it's not written in any will then it will go to the unclaimed money Thanks Okay....but I'm not sure the bank will give back the extra for MRTA insurance claim since the beneficiary is the bank. Thanks |

|

|

|

|

|

Jan 24 2017, 11:51 PM

|

Senior Member

2,866 posts Joined: Sep 2008 From: Wangsa Maju, KL |

anyone know the schedule of benefits for tokio marine iHealth+?

i send an email to tokio marine but to no avail, i cant get any info on that. anyone here can provide me if u have? |

|

|

Jan 26 2017, 03:31 AM

Show posts by this member only | IPv6 | Post

#2475

|

Senior Member

9,616 posts Joined: Dec 2013 |

Hi guys, I've few questions regarding this AIA investment plan I've mentioned in tgis thread (few months ago). Regarding insurance: 1) What's Basic Cash value? Do I get it when I decided to stop this plan? 2) How much of money that I can get if I surrender as at 33 years old? 3) Why this investment plan (projection returns) like not growing money? Regarding money invested vs Returns: 4) How it's calculated? I feel like I would "lose more money" if I didn't surrender asap... 5) I've do many calculations before (based on my shallow knowledge). The returns of my plan is worse than I park my money in FD = 5915.5 x 10 years FD (3.5% per annum) 6) Should I surrender it ASAP to "admit lose" to cut lose? Thanks everyone for read this, good night.  |

|

|

Jan 26 2017, 08:21 AM

|

|

Senior Member

945 posts Joined: Jun 2012 |

QUOTE(heavensea @ Jan 26 2017, 03:31 AM)

Hi guys, I've few questions regarding this AIA investment plan I've mentioned in tgis thread (few months ago). Regarding insurance: 1) What's Basic Cash value? Do I get it when I decided to stop this plan? 2) How much of money that I can get if I surrender as at 33 years old? 3) Why this investment plan (projection returns) like not growing money? Regarding money invested vs Returns: 4) How it's calculated? I feel like I would "lose more money" if I didn't surrender asap... 5) I've do many calculations before (based on my shallow knowledge). The returns of my plan is worse than I park my money in FD = 5915.5 x 10 years FD (3.5% per annum) 6) Should I surrender it ASAP to "admit lose" to cut lose? Thanks everyone for read this, good night. 2) please refer to the non guarantee section of your surrender value. Again this is a projection it could differ but the guarantee portion will be guaranteed. So to speak. 3) You sure this is an investment plan? Seems more like a saving plan to me 4) What was your intention when you signed up? Investment or saving? 6) If you can comfortably save the amount then there is no point surrendering it. A successful saving plan is not because of the RM40 you earn interest on but the fact that you actually saved RM1000. If you are saving only 10% of your annual income into these saving plan I would say that's quite manageable however if you are saving 50% of your income here... then that might be a problem for your financial growth. Best, Jiansheng |

|

|

Jan 26 2017, 08:25 AM

|

|

Senior Member

4,724 posts Joined: Jul 2013 |

QUOTE(heavensea @ Jan 26 2017, 03:31 AM)

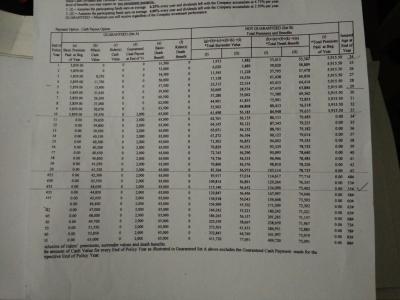

Hi guys, I've few questions regarding this AIA investment plan I've mentioned in tgis thread (few months ago). Regarding insurance: 1) What's Basic Cash value? Do I get it when I decided to stop this plan? 2) How much of money that I can get if I surrender as at 33 years old? 3) Why this investment plan (projection returns) like not growing money? Regarding money invested vs Returns: 4) How it's calculated? I feel like I would "lose more money" if I didn't surrender asap... 5) I've do many calculations before (based on my shallow knowledge). The returns of my plan is worse than I park my money in FD = 5915.5 x 10 years FD (3.5% per annum) 6) Should I surrender it ASAP to "admit lose" to cut lose? Thanks everyone for read this, good night. 2) Minimum 39550. If you wait long enough and get the cash payment, another 2000. (there might be some pro-rate if you pay in monthly mode, etc, or deduct some in return, but this is the general idea) + you may get dividends projected at additional 15k to 20k (the 61k and 56k is inclusive of the 39k and 2k mentioned above). 3) Cause you get back the RM2000. you need to take into account the RM2000 that you get back 4) the later you surrender, the bigger quantum of money you lose. but if you continue to keep the money with AIA, you are projected to get 400k when you are 88. 5) so based on my calculation of 5915.5 for 10 years, and getting back that 400k when you are 88, plus the in between the 2k you get every year, your return is about 4.6%. Refer attachment. 6) depends. you need to do a cost-benefit analysis. My advice is your analysis, should take a greater focus on what you can do with the money now. (but in a nut shell, if you bought this policy for 9 years already, of course, just pay the final year, keep it until you are 88, but if just bought for 1 year, then you want better returns, i think plenty out there) This post has been edited by adele123: Jan 26 2017, 08:28 AM Attached File(s)  IRR.pdf ( 23.43k )

Number of downloads: 11

IRR.pdf ( 23.43k )

Number of downloads: 11 |

|

|

Jan 26 2017, 08:27 AM

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(heavensea @ Jan 26 2017, 03:31 AM)

Hi guys, I've few questions regarding this AIA investment plan I've mentioned in tgis thread (few months ago). Regarding insurance: 1) What's Basic Cash value? Do I get it when I decided to stop this plan? 2) How much of money that I can get if I surrender as at 33 years old? 3) Why this investment plan (projection returns) like not growing money? Regarding money invested vs Returns: 4) How it's calculated? I feel like I would "lose more money" if I didn't surrender asap... 5) I've do many calculations before (based on my shallow knowledge). The returns of my plan is worse than I park my money in FD = 5915.5 x 10 years FD (3.5% per annum) 6) Should I surrender it ASAP to "admit lose" to cut lose? Thanks everyone for read this, good night. 2. Look at the year 33 surrender value 3. How much return are you expecting when you're just pumping in money for the next 10 years only instead of whole life? 4. The returns is definitely higher than FD in the long run as it offers insurance protection which FD doesn't and you are able to nominate that money to someone compared to FD which will be frozen upon death and you're able to claim income tax rebate which FD doesn't 5. No you should not surrender the policy |

|

|

Jan 26 2017, 08:31 AM

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(adele123 @ Jan 26 2017, 08:25 AM) 1) Basic Cash Value is when you surrender, that's the minimum you will get. There's also the dividends, which are not guaranteed. This is not even a good advise at all to ask a person to surrender a policy solely based on the returns without giving a full picture of why the policy is bought in the first place. 2) Minimum 39550. If you wait long enough and get the cash payment, another 2000. (there might be some pro-rate if you pay in monthly mode, etc, or deduct some in return, but this is the general idea) + you may get dividends projected at additional 15k to 20k (the 61k and 56k is inclusive of the 39k and 2k mentioned above). 3) Cause you get back the RM2000. you need to take into account the RM2000 that you get back 4) the later you surrender, the bigger quantum of money you lose. but if you continue to keep the money with AIA, you are projected to get 400k when you are 88. 5) so based on my calculation of 5915.5 for 10 years, and getting back that 400k when you are 88, plus the in between the 2k you get every year, your return is about 4.6%. Refer attachment. 6) depends. you need to do a cost-benefit analysis. My advice is your analysis, should take a greater focus on what you can do with the money now. (but in a nut shell, if you bought this policy for 9 years already, of course, just pay the final year, keep it until you are 88, but if just bought for 1 year, then you want better returns, i think plenty out there) |

|

|

Jan 26 2017, 08:51 AM

|

|

Senior Member

4,724 posts Joined: Jul 2013 |

QUOTE(heavensea @ Jan 26 2017, 03:31 AM) 6) Should I surrender it ASAP to "admit lose" to cut lose? QUOTE(lifebalance @ Jan 26 2017, 08:31 AM) This is not even a good advise at all to ask a person to surrender a policy solely based on the returns without giving a full picture of why the policy is bought in the first place. While i admit i didn't use the word surrender, i might i have implied so. that was my bad. Now, the general rule of thumb is when you surrender, it's not good for you. but given how the person who asked, used words like 'AIA investment plan', my advice was based on someone who bought this with the intention of investing/savings. and already compared using FD return. like i mentioned, it is very true if you want investment, there's plenty out there which will give you better return, without having to lock in someone until he is 88. 88 leh, not 68 leh. that is if i'm still alive at 88. these savings plan was never designed for investment. PS: (to the other guy) actually in the long run, par savings plan can outgain FD returns. i'm not saying will, but can, with not a low chance. |

|

Topic ClosedOptions

|

| Change to: |  0.0312sec 0.0312sec

0.64 0.64

6 queries 6 queries

GZIP Disabled GZIP Disabled

Time is now: 4th December 2025 - 11:33 AM |

Quote

Quote