QUOTE(MUM @ Mar 11 2019, 04:49 PM)

to redeem all...try this steps...hope it works

Thanks! It works!I selected ALL like you've pointed out.

Now available funds are 0.

Public Mutual Funds, version 0.0

|

|

Mar 11 2019, 04:54 PM Mar 11 2019, 04:54 PM

Show posts by this member only | IPv6 | Post

#1661

|

Senior Member

1,218 posts Joined: Jan 2010 From: Today 06.09 am |

QUOTE(MUM @ Mar 11 2019, 04:49 PM) to redeem all...try this steps...hope it works Thanks! It works!I selected ALL like you've pointed out. Now available funds are 0. |

|

|

|

|

|

Mar 12 2019, 08:28 PM

|

Junior Member

38 posts Joined: Dec 2008 |

Dear all sifus,

What is your opinion on Public E cash deposit? It function like REPO. Min investment is suitable for newbie like me.. |

|

|

Mar 12 2019, 09:01 PM

|

|

All Stars

14,856 posts Joined: Mar 2015 |

QUOTE(babyphie @ Mar 12 2019, 08:28 PM) Dear all sifus, The fund is suitable for short-term investors who seek capital preservation. What is your opinion on Public E cash deposit? It function like REPO. Min investment is suitable for newbie like me.. Notes: This is neither a capital guaranteed nor a capital protected fund. Short term refers to a period of less than 3 years. looking at the returns....it looks like almost similar with Bank's Fixed Deposit board rates.... Minimum initial investment*: RM100. Minimum additional investment*: RM10.  for some people for some peoplehttps://www.publicmutual.com.my/LinkClick.a...M%3D&portalid=0 This post has been edited by MUM: Mar 12 2019, 09:01 PM |

|

|

Mar 12 2019, 09:26 PM

|

|

Junior Member

38 posts Joined: Dec 2008 |

QUOTE(MUM @ Mar 12 2019, 09:01 PM) The fund is suitable for short-term investors who seek capital preservation. Should i go for 3 yrs or try my luck for 1 yr?Notes: This is neither a capital guaranteed nor a capital protected fund. Short term refers to a period of less than 3 years. looking at the returns....it looks like almost similar with Bank's Fixed Deposit board rates.... Minimum initial investment*: RM100. Minimum additional investment*: RM10. for some peoplehttps://www.publicmutual.com.my/LinkClick.a...M%3D&portalid=0 |

|

|

Mar 12 2019, 09:28 PM

|

|

All Stars

14,856 posts Joined: Mar 2015 |

QUOTE(babyphie @ Mar 12 2019, 09:26 PM) Should i go for 3 yrs or try my luck for 1 yr? try your luck?what is the targeted Total ROI (in 3 yrs time or 1 yr time) do you intent to get before you can consider if your luck is good or not good? This post has been edited by MUM: Mar 12 2019, 09:29 PM |

|

|

Mar 12 2019, 10:34 PM

|

|

Junior Member

38 posts Joined: Dec 2008 |

QUOTE(MUM @ Mar 12 2019, 09:28 PM) try your luck? Brought China Pacific Equity fund before... 10 yrs losing money. Only manage to get back capital. Since that, i don't buy anymore. Yes. I'm kiasu and kiasi.. 😅 Blame myself for not equipped with the knowledge..Need all the sifu here to enlighten me. 🙇♀️what is the targeted Total ROI (in 3 yrs time or 1 yr time) do you intent to get before you can consider if your luck is good or not good? |

|

|

|

|

|

Mar 19 2019, 07:02 PM

|

Junior Member

590 posts Joined: Dec 2015 |

I requested to switch funds on 16/3/19.

Until now, transaction status still floating. How many days Public mutual process normally? |

|

|

Mar 19 2019, 07:36 PM

|

|

All Stars

14,856 posts Joined: Mar 2015 |

QUOTE(engyr @ Mar 19 2019, 07:02 PM) I requested to switch funds on 16/3/19. while waiting for experienced sifus responses,Until now, transaction status still floating. How many days Public mutual process normally? my wild guess is.... you apply to sell on 16/3 (Saturday) depending on the fund itself, the actual sell may just trigger on Monday. (18/3) the Nav of Monday will only be known most probably on Tuesday 19/3 the fund house can just do the transaction based on the known Monday's Nav |

|

|

Mar 19 2019, 09:06 PM

|

|

Junior Member

590 posts Joined: Dec 2015 |

QUOTE(MUM @ Mar 19 2019, 07:36 PM) while waiting for experienced sifus responses, Yes, I expected transaction is clear today. Till now, it is still floating transaction.my wild guess is.... you apply to sell on 16/3 (Saturday) depending on the fund itself, the actual sell may just trigger on Monday. (18/3) the Nav of Monday will only be known most probably on Tuesday 19/3 the fund house can just do the transaction based on the known Monday's Nav |

|

|

Mar 19 2019, 09:07 PM

Show posts by this member only | IPv6 | Post

#1670

|

|

All Stars

52,874 posts Joined: Jan 2003 |

QUOTE(engyr @ Mar 19 2019, 09:06 PM) Yes, I expected transaction is clear today. Till now, it is still floating transaction. I don't think it'll be so fast.I'll expect to complete by T+3 days. This post has been edited by David83: Mar 19 2019, 09:08 PM |

|

|

Apr 30 2019, 06:34 PM

Show posts by this member only | IPv6 | Post

#1671

|

|

All Stars

52,874 posts Joined: Jan 2003 |

Public Mutual declares RM91m distributions for eight funds

The gross distribution per unit for Public Far-East Telco & Infrastructure Fund was one sen per unit and for Public Select Mixed Asset Growth Fund 0.25 sen unit. As for the Public Select Mixed Asset Conservative Fund, it was one sen. Public Mutual said the distribution for the Public Islamic Dividend Fund was 0.5 sen. As for the Public Islamic Asia Dividend Fund, Public Ehsan Mixed Asset Growth Fund and Public Ehsan Mixed Asset Conservative Fund it was 0.25 sen per unit for each of the funds. It declared a gross distribution of seven sen per unit for the PB Dynamic Allocation Fund. Read more at https://www.thestar.com.my/business/busines...aVAMXKBGtgkp.99 |

|

|

May 14 2019, 09:35 PM

|

|

Newbie

3 posts Joined: Jan 2017 |

QUOTE(ChessRook @ Feb 22 2019, 01:45 PM) Thats why you need to Point #3 is very important. Thank you for sharing.1) Keep emergency funds of 3-6 months (or even more depending on your age and dependents that you have). This can be a 1 month FD and some money in savings account. 2) A portfolio of investments. Some X percentage in safe assets such as ASN, FD, and bond funds, and a large % in EPF. Then Y percentage in more risky assets such as equity UT, and P2P. 3) Important to rebalance every year. Every time your equity fund goes above a certain percentage that you plan. Then sell part of your equity UT to the % that was planned and invest that amount into safer options such as bond funds and FD. You do this vice versa also when UT equity drops and then sell part of your safe investments and then buy the more risky assets. Thus, you follow the saying buy low and sell high. One also rebalances due to changes in our lives and as we age closer to retirement. As we get closer to retirement. We want to increase X% and reduce Y%. Number 1, 3 and X% in safe investments are meant to protect our risky investments. One only invest in Y% of risky investments when one can afford to hold until a better situation. For more information, you can check youtube videos on emergency funds, how to invest in mutual funds, unit trust rebalancing, asset allocations etc. |

|

|

May 21 2019, 10:55 PM

Show posts by this member only | IPv6 | Post

#1673

|

Senior Member

4,228 posts Joined: Jan 2009 |

Hi All, side track a bit. I purchased a new fund recently from my agent. I used EPF withdrawal for this purpose.

Since finger print and signature is required, he advised me to do the same in 2-3 forms in case there is issue on my finger print. The additional forms are for backup purposes. Is this practice normal and safe? I believe the form is only for EPF withdrawal for unit trust investment and will be directly creditted to my unit fund account. Should I be concern at all? |

|

|

|

|

|

May 21 2019, 11:00 PM

|

|

All Stars

14,856 posts Joined: Mar 2015 |

QUOTE(1282009 @ May 21 2019, 10:55 PM) Hi All, side track a bit. I purchased a new fund recently from my agent. I used EPF withdrawal for this purpose. the money from EPF to EPF MIS is quite save...for it has transaction tracking....Since finger print and signature is required, he advised me to do the same in 2-3 forms in case there is issue on my finger print. The additional forms are for backup purposes. Is this practice normal and safe? I believe the form is only for EPF withdrawal for unit trust investment and will be directly creditted to my unit fund account. Should I be concern at all? the number of forms "Pre signed" will be more of a concern when the agent "auto" periodic withdraw from yr EPF for repurchase/top up of EPF MIS funds. Investors must never pre-sign or place their thumbprints on investment forms to transfer funds from the EPF account to the PRS or unit trust fund under the MIS, he said. “Some unscrupulous consultants are using the forms to further invest without telling the investor,” he said, adding that the FIMM has a complaints management and disciplinary committee that gathers evidence whenever a complaint is lodged. Read more at https://www.thestar.com.my/news/nation/2016...1dTxtOz8rzgc.99 This post has been edited by MUM: May 21 2019, 11:03 PM |

|

|

Jun 4 2019, 07:27 PM

|

|

Junior Member

590 posts Joined: Dec 2015 |

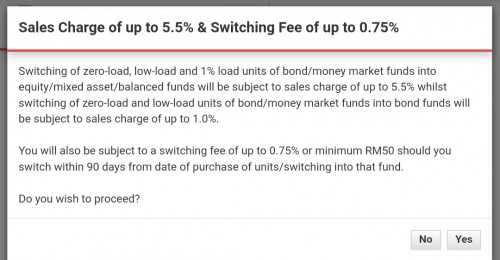

QUOTE(ChessRook @ Feb 22 2019, 01:45 PM) Thats why you need to 3) Important to rebalance every year. Every time your equity fund goes above a certain percentage that you plan. Then sell part of your equity UT to the % that was planned and invest that amount into safer options such as bond funds and FD. You do this vice versa also when UT equity drops and then sell part of your safe investments and then buy the more risky assets. Thus, you follow the saying buy low and sell high. One also rebalances due to changes in our lives and as we age closer to retirement. As we get closer to retirement. We want to increase X% and reduce Y%. Number 1, 3 and X% in safe investments are meant to protect our risky investments. One only invest in Y% of risky investments when one can afford to hold until a better situation. QUOTE(basSist @ Feb 22 2019, 01:39 PM) Keyword: TP- take the god damn profit. And bond/fixed income portion comes into the play which provide you income and cushion when you need to take out the cash during red market.  Many people recommend buy equity fund. Change equity fund to bond fund when economic is bad. Change bond fund to equity fund when economic is good. From the screenshot, we need to pay sales charge when change from bond fund to equity. My understanding is You invest RM1000 to equity fund, sales charge 5.5% When you change from equity fund to bond fund, you need to pay up to 0.75%. When you change from bond fund to equity fund, you need to pay up to 5.5%. Do you think it is better we redeem/sell the units when the market is bad, and buy back again when we want to invest again? This post has been edited by engyr: Jun 4 2019, 08:49 PM |

|

|

Jun 4 2019, 09:32 PM

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(engyr @ Jun 4 2019, 07:27 PM) ........ Do you think it is better we redeem/sell the units when the market is bad, and buy back again when we want to invest again?  usually most would buy more when the markets are low and sell when the markets are high usually most would also buy from those that does charge lower sales charges. well unless those that does not mind about the above at all....then it does not matter |

|

|

Jun 13 2019, 12:34 PM

Show posts by this member only | IPv6 | Post

#1677

|

|

Junior Member

34 posts Joined: Oct 2008 |

QUOTE(yklooi @ Feb 22 2019, 11:49 PM) just an analogy like things...."what if we do the right thing and all is green. You keep the fund there for 10 years. And then suddenly the market crash and you lose the job or something and you need to get some cash. But due to the red market, all the funds that are doing well in 10 years has now plundered. " assuming all green at 7% pa for 10 yrs your invested money will be doubled...... if mkt crashed 50% at that moment......looks like you may still have back your initial investment amount. but if you were to do as per suggested in the earlier posts (above posts), you may lose not that much....  |

|

|

Jun 13 2019, 01:09 PM

|

|

Senior Member

8,188 posts Joined: Apr 2013 |

QUOTE(max291 @ Jun 13 2019, 12:34 PM) You forgotten the 5.5% service charge. That analogy is for 10 yrs...Thus 5.5% over 10 yrs is how much ammortized % ? |

|

|

Jun 14 2019, 05:40 PM

|

Junior Member

790 posts Joined: Sep 2013 From: Selangor |

QUOTE(yklooi @ Jun 4 2019, 09:32 PM) usually most would buy more when the markets are low and sell when the markets are high usually most would also buy from those that does charge lower sales charges. well unless those that does not mind about the above at all....then it does not matter Yet most people play UT like buying stocks, market down sell, market up buy. UT has to be treated as long terms investments with our extra non urgent cash. |

|

|

Jun 26 2019, 03:33 PM

|

All Stars

10,859 posts Joined: Jan 2003 From: Sarawak |

anyone know why there is a drop in public select bond fund earlier this month? from 1.05 to 1.02..

sorry saw the distribution news, but maybe not yet ex-date. This post has been edited by ben3003: Jun 26 2019, 03:41 PM |

| Change to: |  0.0320sec 0.0320sec

0.64 0.64

6 queries 6 queries

GZIP Disabled GZIP Disabled

Time is now: 30th November 2025 - 08:34 PM |

Quote

Quote