QUOTE(Wedchar2912 @ Oct 3 2024, 08:16 PM)

btw, EPF using their own definition of B40 and M40 and T20...

QUOTE(nexona88 @ Oct 3 2024, 08:21 PM)

EPF DIVIDEND, EPF

|

|

Oct 4 2024, 08:37 AM Oct 4 2024, 08:37 AM

Return to original view | IPv6 | Post

#121

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(Wedchar2912 @ Oct 3 2024, 08:16 PM) btw, EPF using their own definition of B40 and M40 and T20... QUOTE(nexona88 @ Oct 3 2024, 08:21 PM) |

|

|

|

|

|

Oct 5 2024, 04:38 PM

Return to original view | IPv6 | Post

#122

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(nexona88 @ Oct 5 2024, 12:40 PM) Boss... Don't think so soon.The option features of transferring money from account 3 to account 1 & 2 already live or not??? Can't seem to find the button in i-akaun kwsp 😔 |

|

|

Oct 7 2024, 03:08 PM

Return to original view | Post

#123

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(jasontoh @ Oct 7 2024, 02:59 PM) Reported or removed by Mod for off-topic? What is so butthurt about the definition? Because they twist it.B40 is literally the bottom 40% of the population managed by EPF. M40 is the middle 40%, and T20 is the top 20%. That's all. THIS IS ELEMENTARY STATISTICS. So no need argue for sake of argument. |

|

|

Oct 7 2024, 03:38 PM

Return to original view | IPv6 | Post

#124

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(Wedchar2912 @ Oct 7 2024, 03:26 PM) agree with you about stats... that is math and numbers only. Ya, and to be fair to govt they are doing away with it.however, the phrase B40, M40 and T20 was created by gov to mean something else, which basically most Malaysians understand it as such. so... what does that mean?  marketing gimmick at its best.... if I am being generous. And I've also said before, T20 is based on household income, in Malaysia T20 is roughly around 11k, so husband and wife salary of RM6k each will be deemed as T20. If husband, wife and one working child, rm4k each. So, everyone here is by any standards T20 in Malaysia. But of course reality tells a different story. |

|

|

Oct 11 2024, 04:31 PM

Return to original view | Post

#125

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

Hi all. Stupid question.

Given now I have access to EPF withdrawal, it makes sense that I take out my money from SSPN come Jan 25, park it in EPF and just put it back in Dec 25 right? |

|

|

Oct 12 2024, 08:04 PM

Return to original view | IPv6 | Post

#126

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(PJusa @ Oct 12 2024, 11:54 AM) If you are able to use EPF like CASA (i.e. above 1M) then yes this is an option. But you still bound to the 100k deposit limit p.a. for EPF Mine is the former, so I have access but good point on the 100k, as taking it in and out means I limit my contributions.If you EPF is below 1M you will rely on Account 3 to recontribute to SSPN. If you have enough inside then no problem. However only 10% of the SSPN money you contribute will end in account 3, the rest wil go to 1&2. I have been thinking about it but could not find a suitable way to really move all from SSPN to EPF (above 100k limit) without shooting myself in the foot. I also need some room for self contribution so for me I just keep the money in SSPN, their interest beats FD considering the real interest on my deposits is higher than the published rate due to tax deductable has to be factored in. The tax deduction only needs to be the end year balance > opening so that was initially why I was thinking about this. Thanks for the reply, must do some maths then to see if I'm able to lock in more than SSPN elsewhere. |

|

|

|

|

|

Oct 13 2024, 03:33 PM

Return to original view | IPv6 | Post

#127

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(Wedchar2912 @ Oct 13 2024, 01:22 PM) only if it is optional... not forced on all I believe even now you can actually request monthly withdrawal rather than lump sum right?My theory is if you are relying only on EPF for your retirement, chances are you don't really have the discipline to handle a large sum of money given to you as long term planning isn't really a thing. EPF probably should mandate for those that is qualified to withdraw their savings to undergo a consultation session with their financial planner prior to it, at least the person will understand the risk of lump sum withdrawal. |

|

|

Oct 19 2024, 11:19 AM

Return to original view | IPv6 | Post

#128

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

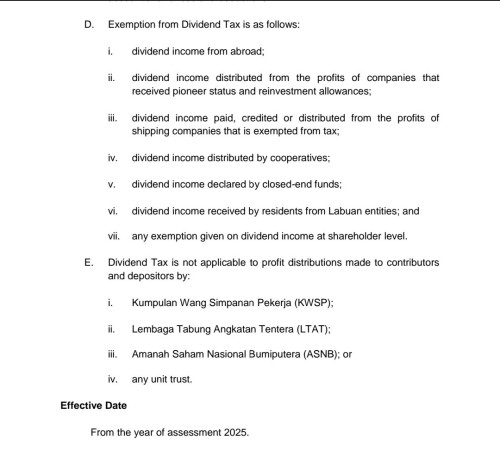

Please stay on topic. It's already said the dividend tax do not apply to EPF. Let it rest there.

Later mods lock thread again. |

|

|

Oct 19 2024, 11:41 AM

Return to original view | IPv6 | Post

#129

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(!@#$%^ @ Oct 19 2024, 11:36 AM) borrowing from another thread. similar but not same. probably but not confirmed yet. It's just the language confusion here. The English copy is clear that it is exempted.  |

|

|

Nov 5 2024, 02:28 PM

Return to original view | Post

#130

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE She claimed the compounding effect accelerated her wealth accumulation, taking ten years to reach her first million but only three years for the second. I think a lot of people miss this part. 10 years to reach first million. Which I guess if you start your career at 7-8k with an average bonus of 3 months + higher EPF + high increament (given she hit RM50k salary after 10 years), it is not impossible but obviously not the typical scenario. Wedchar2912 liked this post

|

|

|

Nov 5 2024, 10:59 PM

Return to original view | IPv6 | Post

#131

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(fuzzy @ Nov 5 2024, 02:28 PM) I think a lot of people miss this part. 10 years to reach first million. Which I guess if you start your career at 7-8k with an average bonus of 3 months + higher EPF + high increament (given she hit RM50k salary after 10 years), it is not impossible but obviously not the typical scenario. Also I just realised, the 100k cap was just introduced last year. So how did she contributed 100k a year for few years back? |

|

|

Nov 6 2024, 12:11 AM

Return to original view | IPv6 | Post

#132

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(adele123 @ Nov 5 2024, 11:57 PM) Actually, dont need to keep analysing this to death It went out of proportion because it's EPF, which is fairly regulated plus the age la.The formula has always been simple, there is no shortcut. Save more, earn more, spend less. And the power of compounding. That's why i hate that 50 30 20 rule. Obviously they also didnt read psychology of money. It revolves around this. I genuinely felt like the post went out of proportion because of the person was a female and 35. It probably would be forgotten if that person was a male. Most fresh grad think about yay, let's buy a car. 12 years ago when i was a fresh grad, i think very hard how to not buy a car. Mindset need to change. Of course luck plays a factor, right job, right industry but at the end of the day, you gotta still work hard. I don't doubt she can achieved it, I've seen many and I'm also a beneficiary of massive luck that propel my income. Just sad that she was forced to delete her post because people became envious and started to be toxic. |

|

|

Nov 10 2024, 02:37 PM

Return to original view | IPv6 | Post

#133

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(nexona88 @ Nov 6 2024, 02:13 PM) Nothing to be jealous or wrong in saying about "tongkat"... In 2014 my EPF was like 50k, it exceeded 1mil 10yrs later.Because it's truth... If one living expenses is being "supported" by others sources... So you can just maximize your EPF monthly deduction to at least 70% to 75%.... And show off you got 2mil in EPF... Only would gain my full respect when you start from zero, your expenses is paid by yourself by monthly salary... And yet you managed to get 1mil in EPF... By mid 30... I don't think it's impossible even without tongkat. |

|

|

|

|

|

Nov 10 2024, 02:46 PM

Return to original view | IPv6 | Post

#134

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(nexona88 @ Nov 10 2024, 02:40 PM) Self contribution to the max yearly?? Rarely self contribute, coz I think S&P500 gives better returns lolYour mandatory deduction percentage?? Standard one or higher?? And standard la, I don't see the point of putting anything more vs putting to equities market. nexona88 liked this post

|

|

|

Nov 11 2024, 11:59 AM

Return to original view | Post

#135

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(gashout @ Nov 11 2024, 06:13 AM) are you still working currently? i am still trying to hit my 1 mil, so congrats on your big milestone Yep, I enjoy my work  and are you continuing to put fund in the us market given how hype the market is currently? i am thinking maybe i should load up my bullet first then attack later if we see some black swan event.  Will continue to put in US markets, I think if we zoom out to a longer runway, all these noises iron out. My issue is actually some of my individual holdings has pumped up so much it's messing up my allocation %. |

|

|

Nov 11 2024, 04:02 PM

Return to original view | Post

#136

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(virtualgay @ Nov 11 2024, 03:56 PM) can we project with minimum pay of RM1750, dividend 5%, increment 5% 36 years.work till how man years before reaching RM1.0M? |

|

|

Nov 11 2024, 05:36 PM

Return to original view | Post

#137

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(virtualgay @ Nov 11 2024, 05:17 PM) so let just say you start at 24 then you work 36 years which means you will be 60 years old and finally you got your 1Million!! Yes, that has been what many here has mentioned before.so basically everyone can be a millionaire! If your salary is RM3,200 and you work around 38 years without ANY increment, not even a sen more in 38 years, you will still have 1mil for your EPF. If you feel motivated and just add an additional RM150 per month, you will reach that figure in 35 years. That is the power of compounding and patience. |

|

|

Nov 12 2024, 11:11 AM

Return to original view | Post

#138

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(nexona88 @ Nov 12 2024, 09:48 AM) Which one needs to look at?? DIV-C = conventionalThe most right side?? That have percentage?? Correct?? Then I see 1 year the payout is 105% yo... DIV-S = syariah DIV-T = total |

|

|

Nov 12 2024, 11:17 AM

Return to original view | Post

#139

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(nexona88 @ Nov 12 2024, 11:15 AM) So the payout ratio is the last one with percentage of 91%... Yep, so the answer is EPF does not necessary pays out 100% of their NI as dividends. They do keep for rainy days or something else.That's the only logical thing I see there.... |

|

|

Nov 13 2024, 10:36 AM

Return to original view | Post

#140

|

|

Senior Member

7,106 posts Joined: Jan 2003 |

QUOTE(Syok Your Mom @ Nov 13 2024, 08:25 AM) One more round should be grateful why would people be grateful that they are jeopordising their retirement? HolyCooler liked this post

|

| Change to: |  0.0479sec 0.0479sec

0.42 0.42

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 4th December 2025 - 05:51 PM |

Quote

Quote