Jan 24 2024, 02:09 PM

Jan 24 2024, 02:09 PM

QUOTE(Davidtcf @ Jan 24 2024, 01:40 PM)

may I know which PRS fund is good? which is the best for my RM3k for claiming income tax returns?

I actually got to know it from Versa ads (as I am using Versa save), but I don't have confidence much in the things they invest in after reading their breakdown of the low, medium, and high risk PRS funds.

The only good prs fund that have as little possible exposure to Malaysia and China.I actually got to know it from Versa ads (as I am using Versa save), but I don't have confidence much in the things they invest in after reading their breakdown of the low, medium, and high risk PRS funds.

The only 2 exist which you can get from FSM for free

AIA Pam growth and principal retire easy 50 series. They stil leave exposure to china. But they are among the one with best returns.

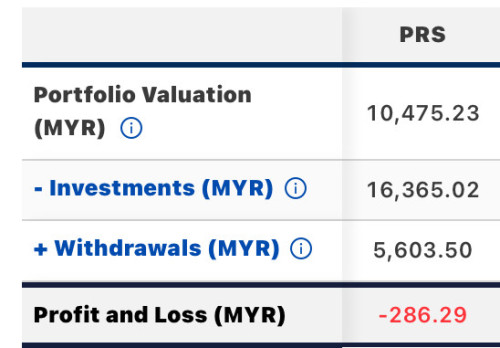

Forget versa. Lousy prs from affin hwang.

Of course my returns and my risk level may not match yours. So what works for me may not work for you.

This post has been edited by Ramjade: Jan 24 2024, 02:09 PM

Quote

Quote

0.1346sec

0.1346sec

0.82

0.82

7 queries

7 queries

GZIP Disabled

GZIP Disabled