Apr 25 2012, 05:32 PM

Apr 25 2012, 05:32 PM

QUOTE(mango27 @ Apr 25 2012, 09:07 AM)

Dear all, need some advice...

Is it feasible if i get a housing loan of 300k - 350k on a shared loan? I started work just over a year... It is for own stay as planning to get married in the future, so i would live in it around 10-15 years at least... it is also a partial investment as it is a new launch unit and will be located to less than 2km near to a future LRT station... Since its a new launch, within these 3 years im just paying slight interest before the vp... below are the breakdown of my current income and expenses...

INCOME (Self):

1. Salary : RM 3000

2. Fixed Allowance : RM 300

3. Variable Allowance : RM 1300 ~ 1650

INCOME (Partner):

1. Salary : RM 2500

2. Variable Allowance : RM 200 ~ 300

FIXED EXPENSES (Self + Partner):

1. Insurance : RM 260 + RM 160

2. Gym membership : RM 175

3. Telephone bil : RM 150

4. Car noan repayment : RM 550

5. ASB savings loan : RM 631

6. PTPTN loan repayment : RM 300

VARIABLE EXPENSES (Self + Partner):

1. Food : RM 800 ~ RM 1000

2. Transportation : RM 500 ~ RM 600

3. Others : RM 500 ~ RM 600

The rest will be to our savings... So our income after EPF and tax deduction will be Min/Max -> RM 6497/6897... Minus expenses Min/Max -> RM 4026/4426... so monthly we have around RM 2471 to spare... last year my partner have 7 months bonus while i have only 2 months... so that is extra RM 1700 monthly if divided... but not taking that into account as its a bonus...

For RM 2471 to spare, taking a loan of 350k for 35 years would be RM 1613 per month... Since we're still early in our working years, commitment is lower now... but at the same time, in 3 years time when its completed, our income will increase... so is it advisable to take on such huge loan at this stage? im 25 this year btw...

Hi Mango27,Is it feasible if i get a housing loan of 300k - 350k on a shared loan? I started work just over a year... It is for own stay as planning to get married in the future, so i would live in it around 10-15 years at least... it is also a partial investment as it is a new launch unit and will be located to less than 2km near to a future LRT station... Since its a new launch, within these 3 years im just paying slight interest before the vp... below are the breakdown of my current income and expenses...

INCOME (Self):

1. Salary : RM 3000

2. Fixed Allowance : RM 300

3. Variable Allowance : RM 1300 ~ 1650

INCOME (Partner):

1. Salary : RM 2500

2. Variable Allowance : RM 200 ~ 300

FIXED EXPENSES (Self + Partner):

1. Insurance : RM 260 + RM 160

2. Gym membership : RM 175

3. Telephone bil : RM 150

4. Car noan repayment : RM 550

5. ASB savings loan : RM 631

6. PTPTN loan repayment : RM 300

VARIABLE EXPENSES (Self + Partner):

1. Food : RM 800 ~ RM 1000

2. Transportation : RM 500 ~ RM 600

3. Others : RM 500 ~ RM 600

The rest will be to our savings... So our income after EPF and tax deduction will be Min/Max -> RM 6497/6897... Minus expenses Min/Max -> RM 4026/4426... so monthly we have around RM 2471 to spare... last year my partner have 7 months bonus while i have only 2 months... so that is extra RM 1700 monthly if divided... but not taking that into account as its a bonus...

For RM 2471 to spare, taking a loan of 350k for 35 years would be RM 1613 per month... Since we're still early in our working years, commitment is lower now... but at the same time, in 3 years time when its completed, our income will increase... so is it advisable to take on such huge loan at this stage? im 25 this year btw...

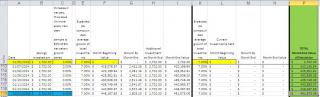

May i bug U for your current rental cost? Hheh - need more complete data to simulate better and bounce ideas with U here.

I noticed U are not staying in your own home (aiming to buy or not buy, thus your post), but no rental costs?

OR is it lumped into the "Others: $500 ~$600"?

BTW, i've also noticed that your "free money" is about $2,071 after taking the minimum $6,497 and LESS maximum costs U stated above for Fixed & Variable Expenses, quite a bit off from $2,471 U stated U should have to spare for paying off a home loan. Heheh - sorry ar, i'm using the least net income VS most variable expenses for prudence sake

This post has been edited by wongmunkeong: Apr 25 2012, 08:56 PM

Quote

Quote

0.0337sec

0.0337sec

0.29

0.29

6 queries

6 queries

GZIP Disabled

GZIP Disabled