QUOTE(mango27 @ Apr 25 2012, 09:07 AM)

» Click to show Spoiler - click again to hide... «

Dear all, need some advice...

Is it feasible if i get a housing loan of 300k - 350k on a shared loan? I started work just over a year... It is for own stay as planning to get married in the future, so i would live in it around 10-15 years at least... it is also a partial investment as it is a new launch unit and will be located to less than 2km near to a future LRT station... Since its a new launch, within these 3 years im just paying slight interest before the vp... below are the breakdown of my current income and expenses...

INCOME (Self):

1. Salary : RM 3000

2. Fixed Allowance : RM 300

3. Variable Allowance : RM 1300 ~ 1650

INCOME (Partner):

1. Salary : RM 2500

2. Variable Allowance : RM 200 ~ 300

FIXED EXPENSES (Self + Partner):

1. Insurance : RM 260 + RM 160

2. Gym membership : RM 175

3. Telephone bil : RM 150

4. Car noan repayment : RM 550

5. ASB savings loan : RM 631

6. PTPTN loan repayment : RM 300

VARIABLE EXPENSES (Self + Partner):

1. Food : RM 800 ~ RM 1000

2. Transportation : RM 500 ~ RM 600

3. Others : RM 500 ~ RM 600

The rest will be to our savings... So our income after EPF and tax deduction will be Min/Max -> RM 6497/6897... Minus expenses Min/Max -> RM 4026/4426... so monthly we have around RM 2471 to spare... last year my partner have 7 months bonus while i have only 2 months... so that is extra RM 1700 monthly if divided... but not taking that into account as its a bonus...

For RM 2471 to spare, taking a loan of 350k for 35 years would be RM 1613 per month... Since we're still early in our working years, commitment is lower now... but at the same time, in 3 years time when its completed, our income will increase... so is it advisable to take on such huge loan at this stage? im 25 this year btw...

QUOTE(mango27 @ Apr 26 2012, 10:16 AM)

Added on April 26, 2012, 10:34 am» Click to show Spoiler - click again to hide... «

Now staying with my mom.. No rental cost.. Hehe.. Others is for entertainment etc..

I have enough to pay off home loan.. But is it wise to do so? A 35 years loan interest would cost around 300k.. Even if pay of early to 25 years still would cost around 200k.. Not so good of an investment I would say.. its a condo so appreciation won't be much. So would investing in asb better?

Also now my expenses is low cause still young. Driving a 9yo paid off car. So it would last me for another few year then new commitment comes. Then other thing like marriage and etc need big amount of money. Thus the dilemma now.

May i take a stab at this?

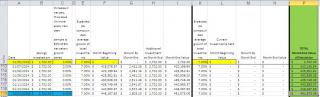

Hm.. let's go by the numbers first shall we (based on attached ZIPped Excel file which U can play with to see "what if"):

Mango.zip

Mango.zip ( 276.31k )

Number of downloads: 42Please keep in mind, i'm taking your "higher" expense variables and "lower" net income just to be prudent

% of net income

% of net income

VS

1. Spending on "Feel Good" is about 16.55% of your net, which IMHO, is a wee bit too high

2. NOW you're doing well with 41.59% savings & investment

3. WITH HOME your savings & investment will drop to $964 or 14.84% of net income - impact, please see 2nd part of opinion/feedback

4. WITH HOME your net income % allocated to monthly loan repayment + fixing + cukai pintu/tanah is about 26.75%, which is slightly high for comfortable level

5. However, since your partner & U are just starting out and can see increments coming in by the dollops, should not be a prob if U decide to buy a $300K home

Savings & Investments extrapolated to 01/01/2025 based on 7%pa growth

VS

a. Please note that i did not extrapolate how much EXTRA per year you'll save, just to keep it simple.

If U wish to simulate, please change cell C3 of "NetSalarySave&Invest-NoHome" and "NetSalarySave&Invest-WithHome" worksheet

b. There is a variance of about $290K between both scenarios, about 64% difference.

Note: I did not include the worth of your house into the scenarios since it's a home, not investment/rental property, making U $ or easily disposed

c. As U anticipated earlier.. whoa.. buying a home MAY not be a good idea in terms of growing investment returns

IMHO, bottom line:+Buying a home is NOT an investment per se UNLESS... maybe if there is a huge property market crash when U buy and U intend to rent out a few rooms heheh.

The main objective of buying a home is to have a place to be yours, grow roots, etc. and totally be yourself.

+Since you've thought it out well (location of your $300K home) and reasoned it well + we didn't include ANY bonuses nor average increments... it is safe enough to consider buying.

Combined net income for the loan & operations of the home looks ok - 26%ish excluding net income growth AND bonuses.

-IF consider buying now, before getting married, be wary of "joint" purchase.

er.. sorry to be a wet blanket.. your current squeeze may not turn out to be your future partner/spouse.. then how ar?

awkward like heck man + may be forced to sell at a loss

Hope some of the ideas/items above + the Excel is of use

Just a thought

This post has been edited by wongmunkeong: Apr 26 2012, 01:05 PM

This post has been edited by wongmunkeong: Apr 26 2012, 01:05 PM

Apr 24 2012, 11:46 AM

Apr 24 2012, 11:46 AM

Quote

Quote

/etc.?

/etc.?

0.0358sec

0.0358sec

0.32

0.32

6 queries

6 queries

GZIP Disabled

GZIP Disabled