i found below article from buffet lover forum, anyone knows how to calculate intrinsic value of a company? we hav lots of stock mentioned as case study on this thread & any can be use as example. Coz i no idea where to get projections of company cash flows, which discount rate to apply and to arrive at their present value

http://www.mechanical-investing.com/warren-buffett.html

http://www.mechanical-investing.com/warren-buffett.html Investing: Price Vs Value

“Our favourite holding period is forever.†- Warren Buffett

This is the wisdom that has flowed from one of the greatest investors of our times. The man is talking, but who is listening? The bigger question to be asked of those few listening is - ‘who is applying’? The richest man, second only to Bill Gates, has time and again proved that value buying always pays off in the long term. His mantra has been to invest in ‘businesses’ not ‘stocks’. The rationale – “If a business does well, the stock followsâ€. In this article, we delve a bit deeper into the principle of value buying and discuss the concept of ‘circle of competence’ as originally defined by Mr. Buffett.

For beginners, ‘value investing’ is about buying stocks that are selling ‘cheap’. In a sense, a value buyer is a bargain hunter. This, however, does not mean that one should buy any stock that is selling cheap. Value buying is about buying stocks of companies that are trading lower to their intrinsic value (this is what we mean by the term - ‘cheap’). Thus, it is not the price of the company’s stock that determine weather it is a value buy, but the potential value that the company has. As such, value investing is about being able to invest in companies with a conviction of the value being realised or unlocked over a period of time.

Valuing stocks

The most common method used to find the intrinsic value of a company is the discounted cash flow method, where projections are made of a company’s cash flows and a discount rate is applied to these to arrive at their present value. If the value arrived at is higher than what the share is presently trading at, it is a value buy else not. Many a times, to make comparative analysis between companies, the ‘price to earnings’ ratio (P/E) is used. An investor has a target P/E in mind and will buy a stock as long as it is trading below its target P/E. When share prices rise without a corresponding increase in earnings or when a company’s earnings are declining without any corresponding changes (or small change) in stock price, it will automatically lead to a rise in the company’s P/E, thus signaling the increased risk levels. This automatic mechanism, which is built into the P/E ratio, is what endears it to the investor community.

Information flow

Value investing, although sound simple on paper, is not so simple to apply practically. This is on account of innumerable factors that affect the stock price movements. While on one hand we have news that apply to the broad market as a whole, on the other there are news that are sector or company specific. The markets are efficient enough to factor in the news flow into the stocks prices. As such, being in coherence with the ‘right’ kind of news is what is the basis for sound (and safe) value investing.

Circle of competence

For a value investor, the most crucial thing is his ability to pick up value stocks. However, this is easier said the done. While the use of different rates to discount cash flows affect the perception on whether a stock is a value buy or not, it is the assumptions with regards to future earnings that are more likely to have a greater impact on valuations. To be able to forecast earnings correctly, one should be able to build the information flowing into the company’s expected earnings forecasts.

In this light, it can be said that each individual will be in a position to understand a certain business better than others. This understanding will become his area of competence of which he will, over a period of time, be able to evolve a circle of competence. The concept, as is original defined by Warren Buffett, stands to mean: ‘an area where an investor can know significantly more than the average investor (called the circle of competence), and focus his efforts on that area’. By developing this, an investor should successfully be able to weave the information flow into his financial model to arrive at a stock’s intrinsic value. As is understood, the circle of competence is a process of evolution and cannot be developed overnight. Rather, it has to be built by gaining insight into the company’s area(s) of operations, finance, management and the scope of future events that are likely to affect it.

Thus in conclusion, you, as an investor, need to compare intrinsic value of the company as a whole to its current market capitalisation. Success will, however, depend on your skill of accurately determining the intrinsic value. It can also be said that to be a good value investor, one needs to harness the qualities of a contrarian investor, a patient investor, a rational investor, an analytical investor, and above all, a long-term investor

Added on November 3, 2009, 10:36 amassuming aapl & goog is excellent la due to moat & bla bla. does it mean, we should be holding our stock position currently? this is wat i understand from the below article or am i over-reading too deep into buffet

anyway, would like to thank the long term holders for hanging on the roller coaster (without u all support to buy from us & average down, we'll have no one to sell to), if it drops, see u below & i can buy the dip

if market moves upward after all data release with confirmation, i hav to gostan position & continue buy...

http://warrenbuffettstockpicks.com/

http://warrenbuffettstockpicks.com/In tough economic times, most individuals would prefer to play it safe but recession stock picks are the way to go according to Warren Buffet stock picks strategy. Warren Buffett is the world’s best and most well known investor and this is what he has to say about Berkshire’s investment portfolio.

“We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.”

In other words, the recession is the perfect time to buy cheap stocks that are below their fair value.

Critics might argue that the stocks and shares in Berkshire Hathaway itself are losing value in the recession. To that, I would argue that the man is still worth tens of billions of dollars and is consistently in the top 3 of Forbes’ World’s richest list. How can you argue with that kind of success? But what is grating is that so called talking heads still criticize Buffett’s investment strategy as being old fashion and not current with today’s market. To that, I say let’s take a look at their bank account balances. Warren Buffett has survived the tech bubble and he will also prevail against the current credit crunch crisis in which “finance specialists” contrived complex investment vehicles that no one could understand which eventually unraveled into a big mess.

Given Buffett’s stock picks of consistently beating the market through decades, I’d put my hard earned money on him and trust Buffett’s recession stock picks advice.

It is well known that Buffett’s investing portfolio is to buy and hold forever. Warren Buffett is thinking for a long term investment strategy and if you have money to invest in the recession, this is the perfect time to put your money in the stock market! Let’s remember, Buffett survived the tech bubble and he will once again survive the credit crunch and housing bubble. The buy and hold, long term investment strategy is in stark contrast to the greedy fast money thinking that got us into this problem in the first place.

Once again, let’s take a look at what Warren Buffett’s advice on stock picking.

“Only buy something that you’d be perfectly happy to hold if the market shut down for 10 years.”

So, to sum up Warren Buffett’s advice on investing: buy and hold for long term and go contrary to popular opinion. Buy stocks that are in steep discounts right now because of the recession and watch it pay off in 10 years time. Read and learn advice from Warren Buffett’s recession stock picks.

Added on November 3, 2009, 10:47 amanyway, can buffet lover teach me how derivatives fit into category of a business with large moat?

are derivatives profitable company or a hedging instrument (ie. gambling)?

some articles may be old, but the essence r still there. so long read man

any buffet lover can summarize all tis in a few sentence ah?

http://blogs.moneycentral.msn.com/topstock...ves-costly.aspxThey were seen by Buffett as an easy way to pocket a quick $4 billion-plus, which was booked much like an insurance premium, even though he is famous for scoffing at derivatives as "weapons of mass financial destruction."

http://seekingalpha.com/article/34606-buff...s-a-fool-s-gameHe noted, however, that Berkshire currently has several dozen derivatives positions -- such as futures and options contracts on stock indexes and foreign currencies

http://www.rapidtrends.com/derivatives-buf...ss-destruction/unless buffet also play, following the money izit?

http://www.vanityfair.com/online/politics/...estruction.htmlAs subsequently revealed in Berkshire Hathaway’s third-quarter 10-K filing with the S.E.C., in 2008, the Oracle turned out to be one of America’s largest sellers of derivative contracts.

http://news.bbc.co.uk/2/hi/business/2817995.stm'Derivatives are financial weapons of mass destruction - Warren Buffett'. so is this mean hypocrite ah?

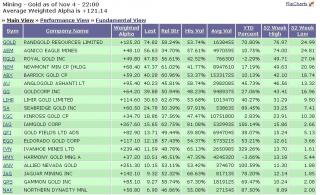

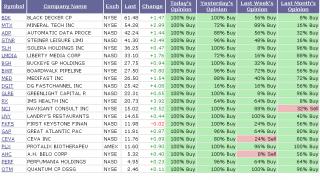

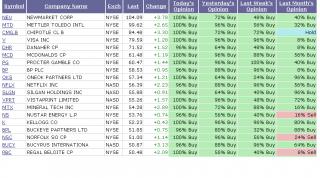

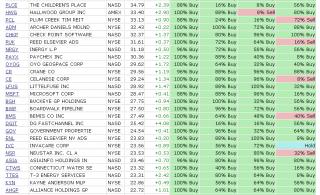

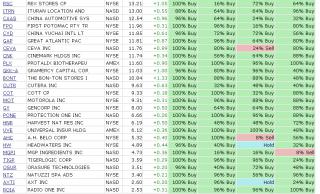

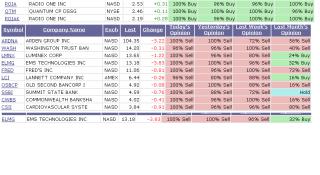

Added on November 3, 2009, 10:54 amstil kenot post pictures

here is another really louyah analyst report on dog jones yoyo session

Stocks ended a confusing session Monday with moderate gains in lower volume.

The Dow rose 0.8%, the NYSE composite 0.7% and the S&P 500 0.6%. The Nasdaq edged up 0.2%.

But volume fell across the board, indicating that institutional investors remain reluctant to buy stocks.

Some economic news and one staggering bankruptcy gripped the market from the get-go. Later came an ominous warning from a Fed official.

But later in the morning, a Fed official warned Congress that the banking system still faces pain.

Jon Greenlee, a top executive with the Fed's Division of Banking Supervision and Regulation, said that "significant stress and weaknesses persist. Corporate bond spreads remain high by historical standards as both expected losses and risk premiums remain elevated.

"Poor loan quality, subpar earnings and uncertainty about future conditions raise questions about capital adequacy for some institutions," he said.

Stocks retraced their early gains and were in the red for a time. The major indexes started bouncing back in the midafternoon to close comfortably off their session lows.

Your only worries for now should be limited to any stocks you bought during the uptrend and are still holding.

This post has been edited by sulifeisgreat: Nov 3 2009, 05:18 PM

Oct 30 2009, 10:38 PM

Oct 30 2009, 10:38 PM

Quote

Quote

(kenot choose confuse! mus make a stand

(kenot choose confuse! mus make a stand  hav to agree with ur remarks

hav to agree with ur remarks

0.0312sec

0.0312sec

0.67

0.67

7 queries

7 queries

GZIP Disabled

GZIP Disabled