have not done any report yet, its a lazy saturday

last time ozak posted some weekly market commentary? izit still available to us on a weekly basis? tq

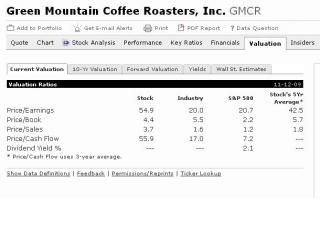

QUOTE(cloud9_lee @ Nov 13 2009, 11:13 PM)

I am hoping LVS will climb to $18. Any thought?

why la lvs topic keep coming up? hold till $19.94 but let me short again at $18.04

imo, below super long read article sums up the situation in usa

i also feel is bearish but the market shows it is not

so my opinion doesn't matter, what the market does - matters

momo have more bullets than us, to do r&d, i small ikan bilis only dog tail them

Job Losses Demystified (Obama : "No one expected this") Peter Schiff

As the unemployment rate crossed the double digit barrier for the first time since Michael Jackson learned to moonwalk, President Obama announced that he will convene a "jobs summit" to finally bring the problem under control. Using all the analytic skill that his administration can muster, the President is determined to figure out why so many people are losing their jobs and then formulate a solution. That's a relief; for a while there, I thought we were in real trouble! In fact, the absolute last thing our economy needs is more federal government interference. If Obama really wants to know what's behind entrenched joblessness, he should start by looking at the man in the mirror.

Obama is pursuing, with unprecedented vigor, the same policies that have for decades undermined our industrial base and yoked us to an unsustainable consumer/credit driven economy. This doubling down on Washington's past failures is destroying jobs at an alarming rate. Today we learned that the September trade deficit surged by 18.2%, the largest gain in ten years. Much of the deficit resulted from Americans spending Cash-for-Clunkers stimulus money on imported cars - or "American" cars loaded to the sunroof with imported parts. In exchange for more domestic debt, we have succeeded only in creating foreign jobs.

An article in this week's New York Times by veteran writer Louis Uchitelle confirmed a fact that I have been alleging for years. Uchitelle pointed out that foreign outsourcing of component manufacturing has led to consistent overstatement of U.S. GDP and productivity. The connection goes a long way to explain why we keep losing jobs even as GDP is apparently expanding.

As our economy becomes less competitive due to higher taxes, burdensome and uncertain regulations, and capital flight, more manufacturing and services will be outsourced to foreign firms. However, the flaw in GDP calculation allows the output of those foreign workers to be included in our domestic tally. Since we count the output but not the worker responsible for it, government statisticians attribute the gains to rising labor productivity. To them, it looks like companies are producing more goods with fewer workers.

The reality is that we are producing less with fewer workers. The added "productivity" comes from higher unemployment and larger trade deficits. This is a toxic formula that will have lethal economic consequences.

Don't expect the brain trust at the President's job summit to fret much about these details. That public relations stunt will likely ignore the root cause of the economic imbalances and instead stress the need for government spending on training and education, i.e. more public debt. The unemployed do not need government theatrics, they need actual jobs. But as long as the government props up failed companies, soaks up all available investment capital, discourages savings, punishes employers, and chases capital out of the country, jobs will continue to be lost.

To really fix the unemployment problem, the President must look past his peers in government and academia to understand how jobs are actually created. In the private sector, all individuals have a choice to either work for themselves or someone else. Since labor is far more productive when combined with capital (office equipment, machinery, business models, and intellectual capital), those who lack these assets themselves often choose to work for others who have sacrificed to accumulate them. This increased productivity is shared between the worker and the owner of capital, and both are better off.

However, for one person or company to choose to offer a job to another, there must be an incentive to do so, and they must have the necessary capital. In the first place, employers must commit to paying wages and benefits, comply with government mandates and regulations, and subject themselves to potential lawsuits from disgruntled employees. All of these costs must be measured against the extra profits an employer hopes to earn by hiring an additional worker.

If profit opportunities exist, jobs will be created. Otherwise, they will not. Of course, anything the government does to raise the cost of employment, such as a higher minimum wage, mandated heath care, or greater regulatory burdens, not only prevents new jobs from being created but also causes many that already exist to be destroyed. Anything that diminishes the profit potential of extra hiring will diminish the number of job opportunities that are created. Also, since it is after-tax profits against which employers measure risk, the higher the marginal rate of income tax, the less likely employers will be able to hire.

Finally, in order to hire workers, employers must have access to capital to expand operations. Anything the government does to discourage capital formation automatically diminishes job creation. By running the largest federal deficits in history, Barack Obama is diverting all available capital to the Treasury, and is in effect waging a war against private capital formation.

If the President's summit truly intends to find the root cause of unemployment, his advisers don't need Bureau of Labor statistics or complex modeling software, just the courage to drop their dogmatic belief in central planning and embrace the laws of economics.

During the past three decades the great majority of new jobs have been created by small busineses. This has been especially true at the early stages of a recovery. But small business owners pay income tax. Prospective entrepreneurs looking out to huge income tax hikes next year and particularly after the 2010 elections, find the prospects for a small business bleak.

Prospective lenders (banks) also see nothing doing out there. So, we have a situation where Banks don’t want to lend and nobody except bad credit risk consumers wants to take their money.

The only ones that are doing OK are big manufacturers who are increasing their profits by lowering costs by laying off less experienced and other low productivity workers. So the stock market has been going up while the overall economy shrinks. Hence the “jobless recovery”.

Clueless Summit

something’s wrong when the government of the most prolific

job-creating economy in history has to schedule a “summit”

to decide how to create jobs.

This isn’t rocket science. Any business owner, entrepreneur or

manager can tell you that job creation requires new businesses,

new investment in plant and equipment, and economic policies

conducive to both.

But so far, those in charge in Washington seem to be doing everything

in their power to kill jobs, whether it’s hiking the minimum

wage, snubbing trade deals, imposing new mandates with health

reforms and climate controls, or paving the way for a massive 69%

increase in capital-gains tax rates by letting the Bush cuts expire.

All told, these and other initiatives, plus the higher spending that

goes with them, will suck as much as $13 trillion out of our economy over

the next decade.

Yet Democrats are shocked — shocked! — that the unemployment rate

has surged to a 26-year high of 10.2%, nearly a third higher

than estimated in February. And that more than 4 million jobs

have been lost this year despite $700 billion in bailouts, $787 billion

in “stimulus,” record-low interest rates of 0%, and more than

$1 trillion in liquidity pumped into the banking system.

Given this record, the only real reason for a jobs summit is to appear

to be “doing something” about the labor market implosion.

After all, 2010 is a midterm election year, and the Democrats’ ability

to continue their leftist tinkering with our once-mighty economy hinges on

voters giving them another chance.

Well, they don’t need a summit. Job creation closely tracks investment in

plants and equipment.So anything the government does to

remove barriers to business investment—whether by cutting regulations,

slashing taxes or reducing government spending — will

lead to more jobs.

Of particular importance are small businesses, which—as a new

report from the Kauffman Foundation noted—created virtually all

the new jobs from 1980 to 2005.

Today,small firms suffer the most damage from congressional incompetence.

The newly passed health care bill, for example, slaps

families with more than $500,000 in income with an added 5.4%

tax. But, according to Congress’ Joint Tax Committee, a third of

this will be paid by small, family-owned businesses.

The government’s fiscal insanity hurts everyone. The Congressional

Budget Office reckons that government outlays will grow at

least 67% over the next 10 years while public debt more than doubles

to $14.3 trillion. In short, not an ideal time for entrepreneurs.

Meanwhile,as Americans in the hundreds of thousands lose their

jobs each month, the government continues to siphon off badly

needed investment capital, waste money to keep failed companies

afloat, discourage personal savings and erect barriers to hiring.

If this continues, don’t expect the “Sorry, not hiring” signs to

come down very soon—summit or no summit.

This post has been edited by sulifeisgreat: Nov 14 2009, 06:50 PM

Nov 7 2009, 09:57 AM

Nov 7 2009, 09:57 AM

Quote

Quote

(beware, sometimes got pullback, sometimes no

(beware, sometimes got pullback, sometimes no

the trick is how sniff for roket fuel?

the trick is how sniff for roket fuel?

coz so far, i sighted no usa stock pick from a forever fan

coz so far, i sighted no usa stock pick from a forever fan  brainstorm kua

brainstorm kua

izit for real?

izit for real?

0.0551sec

0.0551sec

0.35

0.35

7 queries

7 queries

GZIP Disabled

GZIP Disabled