QUOTE(redtuna @ Sep 27 2020, 02:22 PM)

I don't have any idea.. he want to buy ILP hibah.. but then the agent said better take non ILP because ILP if fund drop need to add more and give attachment as example.

But seeing the increment from RM 125 to 525 mcm illogical je. But why the agent want to push for non ILP? Extra commission?

the certificate that your friend has is ILP. I'm not sure why agent explained it is non-ILP. As you can tell, the name of the product bought by your friend is called Takafulink. It is ILP from PruBSN. you can always call PruBSN to confirm with the CS.

if you read carefully, your friend was told to add topup of RM152,000. isn't this more surprising than the RM400 per month?

anyway, to give you some explanation this could be a result of your friend not paying on time or bad fund performance or because your friend's coverage is memang enough to go up to age 64 only, right now.

But from age 64 to age 100, the charges are crazy expensive, so additional RM400 per month is 'normal'. I'm not saying the calculation has to make the most sense but like i said, the RM152k should be more shocking right?

QUOTE(redtuna @ Sep 28 2020, 10:52 AM)

» Click to show Spoiler - click again to hide... «

Found this FWD product online

One of the benefits as stated

Pay the same contribution yearly until certificate expires.

But then when go through the PDS, the rate is not guaranteed.

Is it a bit misleading? Can I lodge a complaint on this?

I will be interested to know the result of your complaint.

On a side note, it's actually "normal". what they are trying to say is. I charge you RM500 per year, every year for coverage of 30 years. For whatever reason because you buy their takaful and many people die during the 1st 15 years, now, they tell you only RM700 per year must be charged every year. So you have to pay RM700 per year until end of 30 years, IF they dont increase the price again during that year 16 to 30.

QUOTE(redtuna @ Sep 29 2020, 09:05 PM)

» Click to show Spoiler - click again to hide... «

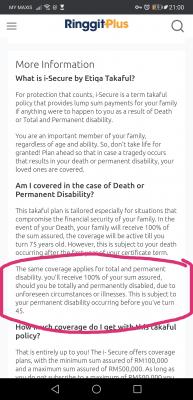

I come across this I-secure takaful by ETIQA.. since there is no PDS provided by ETIQA I did some research and found out this odd term in Ringgit Plus website..

Does that mean if the TPD occur after 45 I will not eligible for compensation?

yes, as per what is written there. however, i would again suggest getting the information directly from Etiqa, i somehow have reservation over websites like ringgitplus because i dont know how much accuracy can be placed upon their information. most in the market, the TPD coverage is up to 60 at least, if it's 45 does seem short compared to the market, but not beyond the realm of possibility.

Sep 27 2020, 02:26 PM

Sep 27 2020, 02:26 PM

Quote

Quote

first time come across such thing for a term insurance.

first time come across such thing for a term insurance.

depends....my takes are depends on

depends....my takes are depends on 0.0265sec

0.0265sec

0.43

0.43

6 queries

6 queries

GZIP Disabled

GZIP Disabled