Outline ·

[ Standard ] ·

Linear+

Insurance Talk V6!, Everything about Insurance

|

redtuna

|

Sep 27 2020, 08:24 AM Sep 27 2020, 08:24 AM

|

Getting Started

|

Those ILP product.. what will happen if the fund does not performs well like during this covid 19 period? my friend fwd me this.. initial contribution RM 125 for 250k coverage.. then fund cannot sustain need to for out RM 525 to maintain same coverage.. true or not? looks like the increment is too much. This post has been edited by redtuna: Sep 27 2020, 08:26 AM Attached thumbnail(s)

|

|

|

|

|

|

redtuna

|

Sep 27 2020, 02:22 PM

|

Getting Started

|

QUOTE(lifebalance @ Sep 27 2020, 11:18 AM) I'm a little confused by the statement given, projected to lapse @ Age 64, projected sustainability = 40 years ? a. Your friend's age only 24 now ? b. Does that mean your policy can only run another 40 years based on 125/m premium? c. Based on this insurance company recommendation to top up, is for until how old ? I don't see it written anywhere d. I don't see any medical rider so it's quite surprising that they would reprice a non-medical policy, that could be a bad sign that they are not able to sustain the claims ratio. I don't have any idea.. he want to buy ILP hibah.. but then the agent said better take non ILP because ILP if fund drop need to add more and give attachment as example. But seeing the increment from RM 125 to 525 mcm illogical je. But why the agent want to push for non ILP? Extra commission? |

|

|

|

|

|

redtuna

|

Sep 28 2020, 10:52 AM

|

Getting Started

|

Found this FWD product online One of the benefits as stated Pay the same contribution yearly until certificate expires.

But then when go through the PDS, the rate is not guaranteed.

Is it a bit misleading? Can I lodge a complaint on this? |

|

|

|

|

|

redtuna

|

Sep 28 2020, 11:09 AM

|

Getting Started

|

QUOTE(lifebalance @ Sep 28 2020, 11:01 AM)  first time come across such thing for a term insurance. As a consumer, you may feel free to lodge a complaint, let me know the outcome thereafter how they are able to maintain the fund until maturity with the same contribution. So far never come across any product that can guarantee same monthly contribution until maturity.. |

|

|

|

|

|

redtuna

|

Sep 29 2020, 09:05 PM

|

Getting Started

|

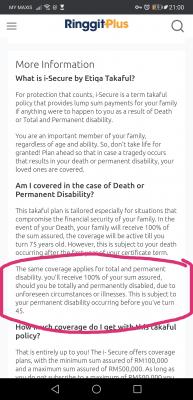

I come across this I-secure takaful by ETIQA.. since there is no PDS provided by ETIQA I did some research and found out this odd term in Ringgit Plus website..

Does that mean if the TPD occur after 45 I will not eligible for compensation? |

|

|

|

|

|

redtuna

|

Oct 1 2020, 12:33 AM

|

Getting Started

|

Some insurance provider offer tailor made top up package to certain big Co. which use employer coverage as deductible.

Eg :

Co. cover medical RM 80k.

Top up plan RM 200k

In normal situation if staff spend more than RM 80k he need to pay out of his own pocket. But under this package let say the medical fee is 180k the 1st RM 80k will be settled by employer as deductible and the remaining RM 100k will be paid by this takaful provider.

Because the deductible is high (RM 80k), the premium for the extra RM 200k is much cheaper compare to standard 200k medical card.

is there any insurance out there that can offers the same arrangement? Meaning client can choose the amount of deductible as to make the premium cheaper.

|

|

|

|

|

Quote

Quote

0.1301sec

0.1301sec

0.29

0.29

7 queries

7 queries

GZIP Disabled

GZIP Disabled