so i've reading up a lot of US-based personal finance books and there seems to be a common theme on insurance, i.e. "insurance is for protection only, not investment".

This got me thinking about my insurance choices. I'm 35 yrs old and i have the following 2x GE plans with the listed riders for about 10 yrs running now. They are all investment-linked which I understand is a mistake?

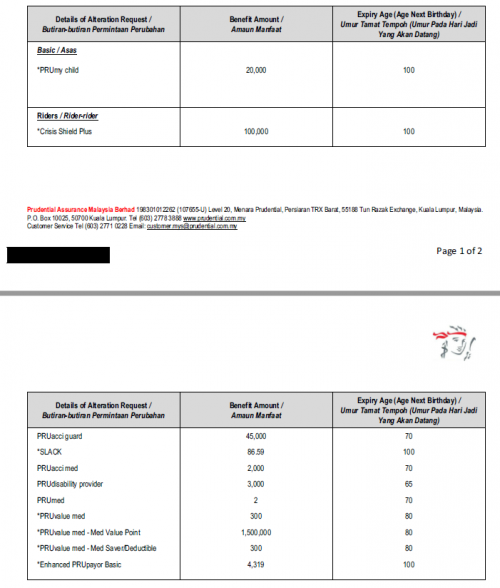

SmartProtect Essential Insurance 2 (RM270/month)

- SmartProtect Essential Insurance 2

- Critical Illness Benefit Rider

- Smart Early Payout CriticalCare

- IL Comprehensive Accident Benefits Xtra Rider

- IL Waiver of Premium Plus

- Smart Medic (SM150)

Great Early Triple Care Special (RM100/month)

I have quite a bit net worth with me that I'm pretty sure I can do without life insurance. My EPF & cash investments are 4x more than my life insurance sum assured. However, I do believe I still need medical and disability insurance. My question is, do you think it's worth for me to restructure my plan so I can:

- Remove the life insurance and investment portion

- Retain (& even upgrade) the medical & disability insurance portion

And what is the best way to go about doing it?

I didn't bother asking my insurance agent because he'll just tell me to retain everything and buy more policies

Good to hear that you have good awareness about your personal finances.

I always believe that you should maximize your coverage so that you don't utilise your personal assets or savings should there be any problem arise such as health, disability or accidents.

With that being said I don't know much about you now personally so the reply will be quite general.

The best way to go about is to do a overall review. That being said, get someone who is independent and non bias who can do that for you.

Jun 15 2020, 04:28 PM

Jun 15 2020, 04:28 PM

Quote

Quote ignore also no use, will be auto charge to your policy anyways

ignore also no use, will be auto charge to your policy anyways

0.1265sec

0.1265sec

0.54

0.54

7 queries

7 queries

GZIP Disabled

GZIP Disabled