Feb 13 2021, 07:38 PM

Feb 13 2021, 07:38 PM

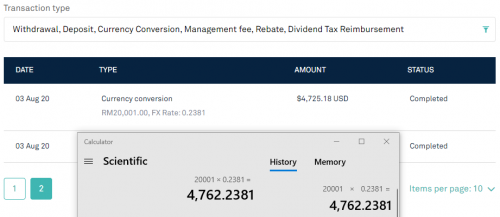

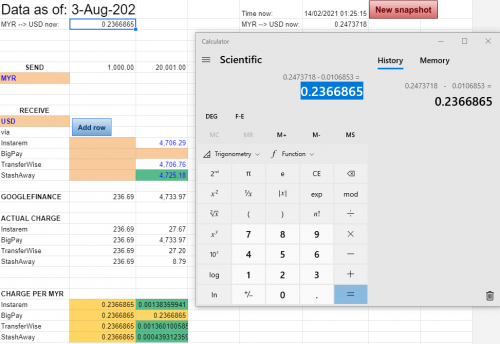

Question about SA's conversion rate - I don't like what I'm seeing but I might be wrong in this. Here's a snapshot of my SA transaction history:

The transfer fee was USD37.0581, considering SA's exchange rate displayed there, there was a hidden processing fee of 37.0581 USD.

Now to reverse engineer to find out what was the MYR>USD rate on 3 Aug 2020:

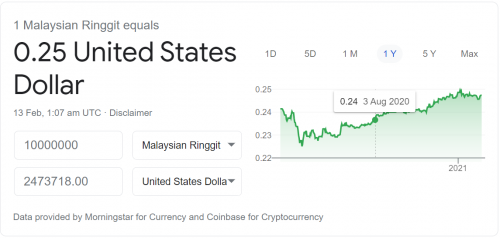

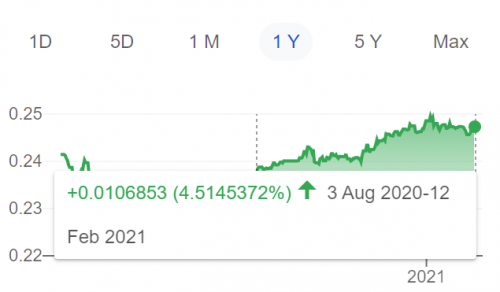

Today (13 Feb), 1MYR = 0.2473718USD

On 3 Aug, 1MYR = 0.2473718 - 0.0047429 = 0.2426289

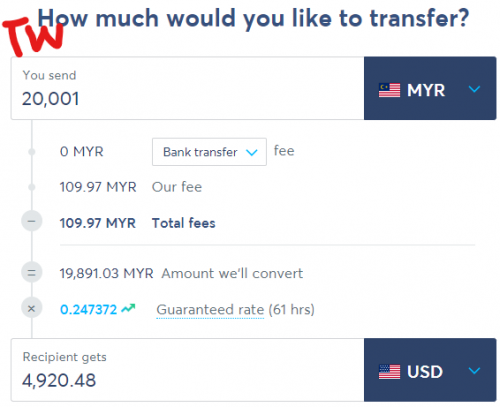

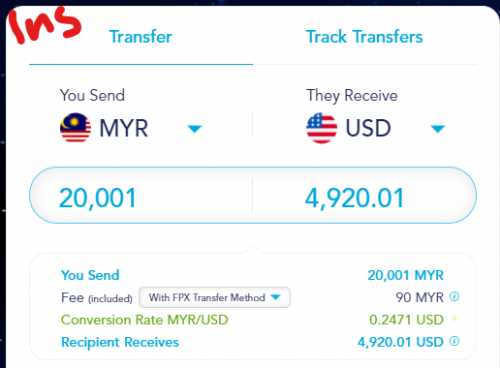

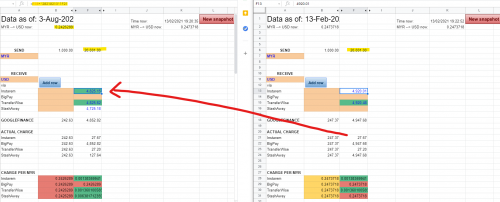

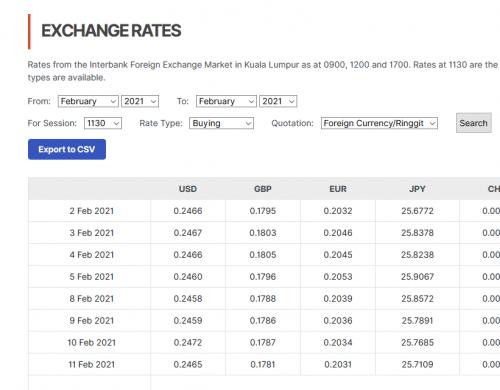

But of course, I have no way to reverse engineer fintech's or bank's offers so I went to Instarem and TransferWise to check the rates, and plotted them onto my own transfer rate calculator (Special thanks to a forumer who did a sheet like this himself, I made my own copy with some additional functions). Google finance is the benchmark, and the various fintechs are more realistic values:

TW and Instarem:

Excel comparison:

RHS: Today's exchange. I'm taking 27.67 USD as the actual charge incurred for the exchange and put that into 3 Aug sheet (LHS). Meaning, if I did the transfer on 3 Aug instead using TransferWise, I would've receive approx 4825 USD instead. That is 100 USD spread from SA's conversion compared to other fintechs! Did I miss out something or is SA conversion rate really that bad?

inb4 "Why are you trying to reverse engineer this?"

I didn't know what I was doing back then, now I want to know if I should continue keeping my money in SA or take it out to invest manually. Frankly speaking, the performance has been disappointing, and I want to know why.

On top of that, there's a 3+USD conversion back to RM to pay the management fee every month, so shitty conversion rate would really hurt investments in SA.

OR, if anyone is going to make a deposit into SA soon, please do me a favour and compare your post-conversion amount to other fintechs? Thank you!

Quote

Quote

yes it's a loss

yes it's a loss

because the transactions happened right before the "market correction" everyone has been talking about this week. It is indeed a little frustrating, but what we're doing here is entrusting someone else (SA) to invest for us, meanwhile I/we(?) can't really time the market, so these reds aren't what we can control. Personally, I've already scheduled my monthly DCA, so I'll just try to sit back and let that happen.

because the transactions happened right before the "market correction" everyone has been talking about this week. It is indeed a little frustrating, but what we're doing here is entrusting someone else (SA) to invest for us, meanwhile I/we(?) can't really time the market, so these reds aren't what we can control. Personally, I've already scheduled my monthly DCA, so I'll just try to sit back and let that happen.

lesgo greeeeeeen

lesgo greeeeeeen

0.0568sec

0.0568sec

0.60

0.60

7 queries

7 queries

GZIP Disabled

GZIP Disabled