QUOTE(Avenger_2012 @ Feb 6 2024, 03:11 PM)

I came from future.

6.25%.

since you are from the future, tell me when will usdmyr reach 5.18? haha6.25%.

EPF DIVIDEND, EPF

|

|

Feb 6 2024, 03:45 PM Feb 6 2024, 03:45 PM

Return to original view | Post

#801

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(Avenger_2012 @ Feb 6 2024, 03:11 PM) I came from future. since you are from the future, tell me when will usdmyr reach 5.18? haha6.25%. |

|

|

|

|

|

Feb 6 2024, 06:36 PM

Return to original view | Post

#802

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(nexona88 @ Feb 6 2024, 06:16 PM) one thing I can see... may I know where it is tagged?your account got tag as "i-saraan" if you officially registered... previously, u won't know until get the rm300 from government in Sept the transaction, which appears as i-saraan in the app, appears as Voluntary contribution on the website version. |

|

|

Feb 6 2024, 06:42 PM

Return to original view | Post

#803

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(nexona88 @ Feb 6 2024, 06:39 PM) under Profile... saw and found it... many thanks... got one big list of stuff... from your name, EPF number, address etc. bottom got write ... |

|

|

Feb 14 2024, 12:36 PM

Return to original view | Post

#804

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(nexona88 @ Feb 14 2024, 12:31 PM) Malaysia has the best retirement platform, called KWSP we definitely have a good retirement platform, but other parts of Malaysia is a bit lacking.  A few years ago, I had the liberty to talk to friends of mine from London on the same topic. It was said Malaysia has the very best retirement platform called Kumpulan Wang Simpanan Pekerja (KWSP). Suffice it to say they were envious of such a system in place, notably in a developing country such as ours. Although people in the United Kingdom were paid handsomely in services and wages, they were forced to create their own retirement plans. Japan has a mandatory pension scheme, but the government increases their retirement age to 65 years old. It was said their salary cut was around 30% for the pension scheme. So on average, their monthly pension is 16,610 yen, or RM 530 per month. https://jesseltontimes.com/2024/02/13/malay...rm-called-kwsp/ the immediate focus is our ringgit...  still not crisis yet, cos still not touch 4.88....  |

|

|

Feb 17 2024, 10:43 AM

Return to original view | Post

#805

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(fuzzy @ Feb 17 2024, 10:11 AM) EPF app is down for maintenance, ini kari lah? QUOTE(nexona88 @ Feb 17 2024, 10:38 AM) Seems like it's coming this weekend 🤑💰🔥 so tonight's fireworks is to celebrate the dividend yield???? hahaha CommodoreAmiga, magika, and 1 other liked this post

|

|

|

Feb 19 2024, 06:31 PM

Return to original view | Post

#806

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(romuluz777 @ Feb 19 2024, 06:15 PM) Best is to make a trip to the EPF office to get an accurate clarification from the horse’s mouth😄 even if one gets some info from the horse's rep's mouth (the horse is EPF itself...), how much can one trust that info to be accurate in X years or even at current juncture? Best to only find out when one actually will do the full withdrawal or fixed monthly withdrawal. romuluz777 liked this post

|

|

|

|

|

|

Feb 20 2024, 04:19 PM

Return to original view | Post

#807

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(nexona88 @ Feb 20 2024, 03:42 PM) Doubtful of how your savings are managed? didn't someone said the div still have to deduct 2.5% for zakat? or something like that?Choose Simpanan Shariah where your savings are managed in accordance with Shariah and enjoy dividends without worries. After that you can keep it in peace! #KWSP #SimpananShariah  |

|

|

Feb 20 2024, 04:21 PM

Return to original view | Post

#808

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(prophetjul @ Feb 20 2024, 03:23 PM) Announcement: SGD has just hit another record high. don't know to be happy or not.... in ringgit terms, thanks to ringgit crashing vs usd and sgd, my whole year's expenditure already full covered (translation gain of course... didn't convert back to ringgit)but in usd term, flat like a corpse's heartbeat. so, should be happy??? |

|

|

Feb 21 2024, 08:25 PM

Return to original view | Post

#809

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(romuluz777 @ Feb 21 2024, 08:22 PM) and gonna reduce some more to focus on domestic sectors suspect it is also to prop up ringgit and bring capital back to malaysia to prop up prices here. |

|

|

Feb 23 2024, 05:08 PM

Return to original view | Post

#810

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(nexona88 @ Feb 23 2024, 04:25 PM) Tax expert predicts 2023 EPF dividend rate at below 6% yet higher than previous year’s 5.35% Funny right? Tax expert talk abt epf div. Some more dare to say reeling from lost fund.MALAYSIANS can expect some solace or silver lining amid the drastic fall of the ringgit as the Employees’ Provident Fund (EPF) is likely to declare 2023 dividend payout between 5.5% and 5.8% in early March. “In simple term, it is better than the previous year but EPF members should not have too high an expectation.” Even as the unemployment rate has declined, Koong pointed out that EPF is still reeling from the “lost funds” effect – referring to the four times of special withdrawals during at the height of the COVID-19 pandemic – which have not been channelled back to the retirement fund. “To declare the dividend payout of 6%, EPF will have to maintain current dividend payout as well as deliver a better performance in its investment portfolios for one to two years,”. https://focusmalaysia.my/tax-expert-predict...ous-years-5-35/ |

|

|

Feb 23 2024, 06:44 PM

Return to original view | Post

#811

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(ronnie @ Feb 23 2024, 05:45 PM) he speaks the truth nobody dare say ma.... the 4x withdrawal was not well planned at all.. its not about the truth as in the withdrawals were ill advised. Yes, those were very silly and the gov/PM/FM of that period should be ashamed. But to state that 2023's div is still negatively impacted is a silly statement. If the assets sold were that good, then EPF should purchased them back and EPF has plenty of time and opportunity to do so. Remember, epf is still getting positive inflow of funds every month pretty much. the negative impact of the sale of those assets would already be felt during covid period. romuluz777 and CommodoreAmiga liked this post

|

|

|

Feb 26 2024, 01:44 PM

Return to original view | Post

#812

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(magika @ Feb 26 2024, 11:52 AM) Nice try but hook no fish he may as well ask the balance in EPF directly... no need to do this round about way. haha magika liked this post

|

|

|

Feb 26 2024, 02:01 PM

Return to original view | Post

#813

|

||||||||||||||||||||||||||||||||||||

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(ongth60 @ Feb 26 2024, 12:14 PM) Here's a table showing the year-by-year comparison of the investment amount for both scenarios: great example....

This table illustrates how the consistent 5.5% EIR provides a steady increase in investment value, while the 10% EIR scenario shows fluctuations due to the -10% adjustments in years 5 and 8. Despite these fluctuations, the total amount after 10 years in the second scenario ends up slightly higher than in the first, highlighting the impact of higher risk and potential reward. The second scenario, which involves a 10% effective interest rate (EIR) with a couple of years experiencing a -10% adjustment, is riskier compared to a consistent 5.5% EIR for several reasons: 1. **Volatility**: The presence of negative returns (-10%) introduces volatility, meaning the investment value can decrease significantly during those years. This unpredictability can be riskier, especially if the investment needs to be liquidated during a down year. 2. **Compounding Effect**: While the compounding effect can work in favor of an investor when returns are consistently positive, it can also amplify losses during negative return years. This means that recovering from a -10% loss requires more than a 10% gain the following year to break even due to the compound interest effect. 3. **Predictability and Planning**: A consistent 5.5% EIR provides more predictability, allowing for better financial planning and less stress about potential negative impacts on the investment due to market fluctuations or other factors. 4. **Risk Tolerance**: The second scenario might be more suitable for investors with a higher risk tolerance who are willing to accept the possibility of negative returns for the potential of achieving slightly higher gains over the long term. In contrast, a consistent 5.5% EIR is more suitable for conservative investors who prefer stability and lower risk. Thus, while the second scenario may offer a slightly higher final amount after 10 years, it carries more risk due to its volatility and the negative returns experienced in certain years. Just to share: at simple glance also pretty can guess that scenario 1 would be better than scenario 2. (of course the detail analysis proves it, so at end to really confirm still need the table.) scenario 1 is 55% arithmetic total return. scenario 2 is 60% arithmetic total return, but with years of volatility. ask any laymen to use their life experience: which would one choose?  no risk or big risk with movement. |

||||||||||||||||||||||||||||||||||||

|

|

|

|

|

Feb 26 2024, 05:26 PM

Return to original view | Post

#814

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(batman1172 @ Feb 26 2024, 04:02 PM) Old guy like me will take scenario 1 to protect 30 years of my retirement fund to cover needs. Anything more I would put in higher risk assets and rebalance yearly. its not just old guys... basically anyone who is not of risk neutral or risk seeking preference would choose scenario 1. This has more history: https://pages.stern.nyu.edu/~adamodar/New_H.../histretSP.html throw cash in and then go do whatever one wants with one's energy and time... zero worries, whereas the scenario 2 still need to worry if a particular year will crash 10% or not. (before the fact of the crash of course). batman1172 and CommodoreAmiga liked this post

|

|

|

Feb 27 2024, 07:42 PM

Return to original view | Post

#815

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(Cubalagi @ Feb 27 2024, 06:55 PM) Joined PNB in July 2020 yet all 4 of these organization didn't really perform that outstandingly right? Harvard economics degree Danaharta, danajamin, khazanah and PNB He has more asset management experience then Amir who was a more corporate guy. Id say give him a chance.   CommodoreAmiga liked this post

|

|

|

Feb 27 2024, 08:28 PM

Return to original view | Post

#816

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(nexona88 @ Feb 27 2024, 07:59 PM) Only joined not even 1 month... Don't know leh... if just hiring a new intern or even lateral move manager/vp, don't mind giving space and chance. Give the guy some space & chance to perform 🧐 EPF is one of the biggest fund in Malaysia... So cannot really play around 😔 but ceo also still need to give chance? some more the largest fund in Malaysia? somehow cannot swallow this... its like lets give PM of a country the chance... still want to give???? still not ready? kens88` and CommodoreAmiga liked this post

|

|

|

Feb 27 2024, 08:45 PM

Return to original view | Post

#817

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(nexona88 @ Feb 27 2024, 08:42 PM) Upcoming dividend sure cannot blame him.... The old guy responsibility.... oh yeah of course... 2023 completely nothing to do with him... Q1 results partly his responsibility... Q2 & above definitely confirm his responsibility... That's where we can see if he fit for the job or not.... 2024 and onwards... eitherway, judging from history, it is just a 3 year rotating chair for them... the special political appointees... |

|

|

Feb 28 2024, 02:30 PM

Return to original view | Post

#818

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(ccschua @ Feb 28 2024, 01:26 PM) now is the classification time, how much dividend u get this year. why not just write the actual avg aum in epf better? B40 - 0 to 40k M40 - 41k to 131k T20 - 131k > so the abv is translated to the table below: B40 - 0 to 666k M40 - 667k to 2.18 million T20 - > 2.18 million btw, like what others said, the table makes no sense... there are only 70K persons with 1 million and above in EPF. definitely not T20 definition. |

|

|

Feb 28 2024, 03:28 PM

Return to original view | Post

#819

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

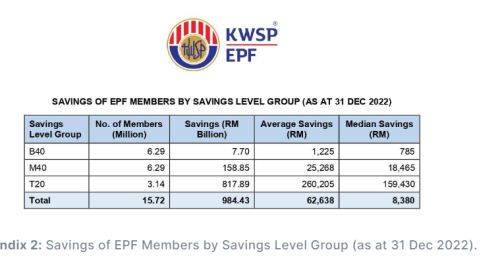

QUOTE(fuzzy @ Feb 28 2024, 03:24 PM) Think is based on this. funny or not this table from EPF?  all it means is that the data on B40 is wrong. no way B40, if all of them are working, to have such low 800rm median savings. (unless epf want to claim that 20% of the epf members are first time employee with lesser than 6 months working experience) CommodoreAmiga liked this post

|

|

|

Feb 29 2024, 04:13 PM

Return to original view | IPv6 | Post

#820

|

|

Senior Member

3,692 posts Joined: Apr 2019 |

QUOTE(!@#$%^ @ Feb 29 2024, 01:47 PM) regardless 5.5 or 6.5%, anybody here gonna stop topping up 100k into epf? Since q4 last year, decided to stop adding more. Any movement in is due to parking spare funds in epf while awaiting opportunity to convert.Now overall strategy is to increase non-ringgit wealth from 40% to 55% by end of year. CommodoreAmiga liked this post

|

| Change to: |  0.0526sec 0.0526sec

0.29 0.29

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 22nd December 2025 - 01:02 AM |

Quote

Quote