some like it hot, some like it cold, some been staying out & some already knee deep inside

irregardless of our opinions, its the action the momo & we take that only matters, real cold hard cash or loan

the usual economic indicators for your pressure reading

http://money.cnn.com/news/economy/index.htmlthere is always 2 side to every issue, just like a coin

make a stand & make $ out of it

http://money.cnn.com/2010/01/04/markets/thebuzz/index.htm and for pleasure reading, the other side of the coin, Don't Blame Ben For The Meltdown

Financial Crisis: It's common these days to hear that the 2007-08 financial meltdown was all the Fed's fault. Speaking last weekend, Fed chief Ben Bernanke set the record straight.

In recent days, we've been surprised by the large number of pundits and market commentators who have stated matter-of-factly that the Fed's actions this decade were "at fault" for the housing boom and bust.

It's one thing, of course, to say that the Fed might have erred in keeping interest rates too low during the economic problems of the 2000s. That may well be the case. But it's quite another to say that they "caused" it all. This simply ignores history.

Faced with a record stock market collapse, a recession and the economic aftermath of 9/11, the Fed very aggressively slashed interest rates from 6.5% at the start of 2001 to 1% by mid-2003 and kept them there until mid-2004. The housing market boomed.

Starting in mid-2004, however, the Fed began to let rates creep up, fearing a spurt in inflation if rates were kept too low.

The housing market continued to boom for two more years, until rates hit 5% in May of 2006. It was then that many people with low-interest, adjustable-rate mortgages suddenly found themselves unable to keep up with payments. Home sales plunged, prices fell, foreclosures soared.

In 2007, the housing market suffered a spectacular fall that dragged down the global economy with it. All the Fed's fault? In a word, no. Virtually no one in 2003 was arguing for anything but massive interest-rate cuts by the Fed. And the Fed obliged them.

Again, in 2005, the Fed raised interest rates based on market fears of rampant inflation. If anything, the Fed's mistake was being too reactive — and not focusing on price stability, the only thing it really can control.

Scapegoating Bernanke would be an easy answer to all this. It would mean we'd have to do little other than fire him, and all our troubles go away.

Unfortunately, what Bernanke said on Sunday at the annual meeting of the American Economic Association happens to be dead right: Our crisis was not one of monetary policy but of misregulation of our financial and housing markets. Whether you think monetary policy was right or wrong, it did not cause the crisis.

"Borrowers chose, and were extended, mortgages that they could not be expected to service in the longer term," Bernanke said. "This description suggests that regulatory and supervisory policies, rather than monetary policies, would have been more effective means of addressing the run-up in house prices."

He's right. As we've noted repeatedly on this page, it wa s government regulation of the housing market that caused our current woes.

Take the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac out of the picture, remove the Community Reinvestment Act (CRA) from the books, and there's no housing crisis — and no financial meltdown. Period. No matter what the Fed did.

By funding trillions of dollars of home loans made by private banks to poor credit risks, Fannie and Freddie created the toxic financial waste that now pollutes the balance sheets of nearly every finance company in America. And will for years to come.

Fannie and Freddie didn't act alone; they were pushed into doing it by Democrats in Congress, such as Connecticut Sen. Chris Dodd and Massachusetts Rep. Barney Frank, and by the Clinton administration, which equipped the CRA to force banks to make bad loans in the name of "boosting homeownership."

"The financial crisis was caused by U.S. government housing policies that helped create 25 million subprime and Alt-A mortgages — 47% of all U.S. mortgages — which are currently defaulting at unprecedented rates," noted Peter Wallison, a senior fellow at the American Enterprise Institute, who predicted the debacle back in 2000. "This caused the financial crisis and current recession."

Today, Fannie and Freddie have become de facto nationalized mortgage companies — holding or originating nearly one half of the nation's $11 trillion or so in mortgages, many of them little more than junk. Having lost an estimated $100 billion in the last year and failed spectacularly, you might think they would pull back.

They haven't. Congress just lifted the borrowing capacity of the two GSEs to above $400 billion — giving them a blank check back from taxpayers to continue their disastrous lending practices.

We're not saying the Fed is beyond reproach. Fed policy is often ill-timed and misguided. But it didn't cause the meltdown.

Those who blithely blame Bernanke's Fed deflect attention from the true culprit behind this mess: a big-government regulatory regime that forced banks to make loans to people who couldn't pay them, and now wants you to pay for it all. And you will.

» Click to show Spoiler - click again to hide... «

do we sell into rally & buy the dip?

market alwiz got up & down, do follow ur own instinct coz no pain, no gain!

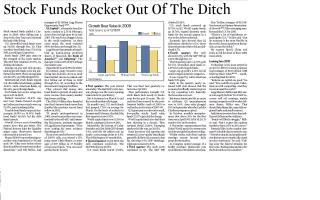

Factory Data Spur Stocks To Solid Gains; Volume Up

Stocks christened a new decade with gusto Monday as the major indexes popped to new highs.

The NYSE composite led with a 2% surge thanks to strength in energy and industrial stocks. The Nasdaq scooped up a 1.7% advance. The S&P 500 and the Dow rose 1.6% and 1.5%, respectively.

Small caps also rallied as the S&P 600 vaulted 2.1%. The indexes closed near session highs, with the Nasdaq reaching the highest closing level since September 2008. The other indexes made it to 15-month peaks.

Volume surged from Thursday's soft preholiday action. NYSE trading swelled 60% and Nasdaq volume 57%.

The news that ignited the buying was December manufacturing data. Before the market opened, data showed China's factory output climbed in December.

In the U.S., the Institute for Supply Management's December index clocked in at 55.9 — a fifth straight month of expansion and its best reading since early 2006. Analysts' consensus forecast was 54.3.

Commodities swung higher on the implication for increased demand.

The market also got a boost from crude prices, which spiked to a two-month high near $82 a barrel partly on the manufacturing data.

Gold surged and the dollar dived as the economic reports raised the likelihood of inflation and higher interest rates.

It was a good day for leading stocks, with many rising in strong volume and some reaching new highs.

Data on factory orders, pending home sales and December vehicle sales will be out Tuesday.

Dec 31 2009, 02:18 PM

Dec 31 2009, 02:18 PM

celebration time, have u place ur bets for the coming year or hibernating

celebration time, have u place ur bets for the coming year or hibernating  step right in, big or small, black or red, up or down, in or out

step right in, big or small, black or red, up or down, in or out  + a sector for pressure reading

+ a sector for pressure reading  Quote

Quote

dun like ipsu chart

dun like ipsu chart

0.0512sec

0.0512sec

0.89

0.89

7 queries

7 queries

GZIP Disabled

GZIP Disabled