Jan 12 2008, 04:41 PM

Jan 12 2008, 04:41 PM

QUOTE(cherroy @ Jan 12 2008, 05:33 PM)

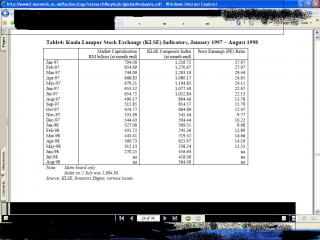

I think you get the wrong number, prior before financial crisis, KLSE was trading above 20x or around 20x - 25x.

Only on super bull run 1993-1994, KLSE managed to trade at 30x plus.

PE at 20x is already somehow a little expensive if growth room upside not much, it only implied a potential 5% return rate which is not that attactive already. It is all about risk and reward. You don't take the high risk to get the return which is comparable to other safer investment tools

PE is a comparable and relative number a 15x in certain time is not the same 'expensive or cheap' level at 15x at other time.

It is depends on interest rate environment, future growth prospect, regional and global condition, liquidity condition etc. If the shares like Coca-cola is trading at 11x while ABC stock in KLSE is trading at 18x, if both growth potential is the same for both stocks for a global fund manager, which one they will choose or buy?

or if the interest rate is 2%, while PE is at 20x (5% return rate), in this case stocks seems attractive, but if interest rate is 5%, then 20x is bloody is expensive already *if consider there is not much future growth for stocks or economy is not growing. On the other hand, if company earning is expected to grow significantly like 30% or more, then even at current PE of 20x seems cheap enough as future earning will drag down its PE, that generally called PE expansion. So whether KLSE has room more upside is largely depends how well the company financial result will be. If company results don't improve as same pace with the rise of the share price/market then it is not sustainble, on other hand, if they do report good result overall then it has room for more upside.

So one can't take the PE number of 17 or 20 to say stock is cheap straight away, PE is not a magical number, it only will be a powerful figure or useful figure for one to make comparison and justification. PE number alone can't tell the whole story, need to look at broader picture to justify it as it is all about risk and reward ratio.

Just my 2 cents

The data are extracted from Public Mutual Analysis, and i truly believe what they said. GDP is expected at 5-6%. The PE of CI stocks together ( Macro Economy) as compared as one stock such as cola-cola or Genting etc. I always leave the selection of individual stocks to the fund managers ( less headaches ), so long they can generate a reasonable profit i( expecting 15% profit a year ). What is the point of challenging them that i can generate more profit than them ? It is like telling your worker that you can do better job than him, ending up doing the job by yourself. After all, I only pay them 0.25 to 1.5% a year to manage my funds.Only on super bull run 1993-1994, KLSE managed to trade at 30x plus.

PE at 20x is already somehow a little expensive if growth room upside not much, it only implied a potential 5% return rate which is not that attactive already. It is all about risk and reward. You don't take the high risk to get the return which is comparable to other safer investment tools

PE is a comparable and relative number a 15x in certain time is not the same 'expensive or cheap' level at 15x at other time.

It is depends on interest rate environment, future growth prospect, regional and global condition, liquidity condition etc. If the shares like Coca-cola is trading at 11x while ABC stock in KLSE is trading at 18x, if both growth potential is the same for both stocks for a global fund manager, which one they will choose or buy?

or if the interest rate is 2%, while PE is at 20x (5% return rate), in this case stocks seems attractive, but if interest rate is 5%, then 20x is bloody is expensive already *if consider there is not much future growth for stocks or economy is not growing. On the other hand, if company earning is expected to grow significantly like 30% or more, then even at current PE of 20x seems cheap enough as future earning will drag down its PE, that generally called PE expansion. So whether KLSE has room more upside is largely depends how well the company financial result will be. If company results don't improve as same pace with the rise of the share price/market then it is not sustainble, on other hand, if they do report good result overall then it has room for more upside.

So one can't take the PE number of 17 or 20 to say stock is cheap straight away, PE is not a magical number, it only will be a powerful figure or useful figure for one to make comparison and justification. PE number alone can't tell the whole story, need to look at broader picture to justify it as it is all about risk and reward ratio.

Just my 2 cents

You can air your own view. For instance, i can say i can beat Tiger Wood in Golf. I can also claim that during recession, people eat only one meal a day !

This post has been edited by SKY 1809: Jan 12 2008, 05:41 PM

Quote

Quote

0.0260sec

0.0260sec

0.52

0.52

6 queries

6 queries

GZIP Disabled

GZIP Disabled