Aug 10 2021, 07:52 PM

Aug 10 2021, 07:52 PM

QUOTE(timeekit @ Aug 10 2021, 07:23 PM)

Hi All,

I need your advice and clarification on how my medical policy works. Note the policy is from Great Eastern.

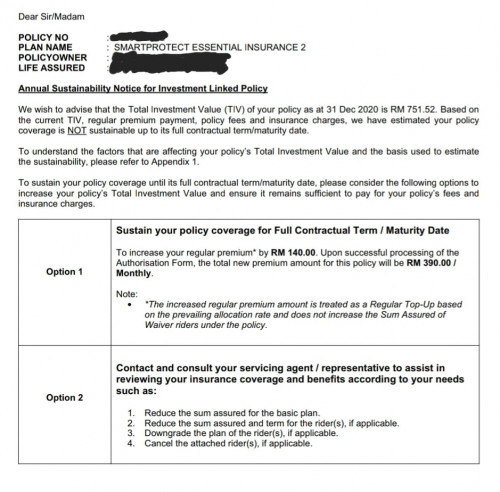

I receive this letter couple of months back asking me top up because my current monthly payment is unable to "sustain" my insurance plan.

My insurance agent explain to me that topping up is not required especially for my age demographic (late 20s), and my policy can still cover me to maybe age 70+(?)

I have a few questions :

1) What is the difference between increasing and not increasing the premium amount.

2) If i increase the premium amount, does it mean that the policy can maintain longer and vice versa ?

3) Scenario : Lets say i don't increase the premium amount, and the policy can "sustain" until I'm 70, what happens later if i reach to 71 age, does my policy suddenly lapse ? how will i be notified and how much should i increase the premium then ? (Touch Wood) Lets say if i'm hospitalised at age 71, does it mean that my insurance is effectively lapse and I'm not insured? What happen to all the premiums i payed previously, does it not cover any of my hospital bill ?

4) Scenario : Lets say i do increase the premium and policy can sustain longer, but what if (touch wood) I don't reach the supposedly extended period. What happens to the extra premiums I paid ? All wasted ?

Really sorry if I'm asking very noob-ish questions.

Appreciate your time in explaining this to me and much thanks in advance.

1) What is the difference between increasing and not increasing the premium amount.I need your advice and clarification on how my medical policy works. Note the policy is from Great Eastern.

I receive this letter couple of months back asking me top up because my current monthly payment is unable to "sustain" my insurance plan.

My insurance agent explain to me that topping up is not required especially for my age demographic (late 20s), and my policy can still cover me to maybe age 70+(?)

I have a few questions :

1) What is the difference between increasing and not increasing the premium amount.

2) If i increase the premium amount, does it mean that the policy can maintain longer and vice versa ?

3) Scenario : Lets say i don't increase the premium amount, and the policy can "sustain" until I'm 70, what happens later if i reach to 71 age, does my policy suddenly lapse ? how will i be notified and how much should i increase the premium then ? (Touch Wood) Lets say if i'm hospitalised at age 71, does it mean that my insurance is effectively lapse and I'm not insured? What happen to all the premiums i payed previously, does it not cover any of my hospital bill ?

4) Scenario : Lets say i do increase the premium and policy can sustain longer, but what if (touch wood) I don't reach the supposedly extended period. What happens to the extra premiums I paid ? All wasted ?

Really sorry if I'm asking very noob-ish questions.

Appreciate your time in explaining this to me and much thanks in advance.

You are advised by the insurance company to do the necessary top up otherwise your policy may not be sustainable based on your original term of coverage. Which means your insurance coverage will end earlier.

In this case, your insurance company recommends you to top up an additional RM140 monthly.

2) If i increase the premium amount, does it mean that the policy can maintain longer and vice versa ?

Yes as per my explanation above

3) Scenario : Lets say i don't increase the premium amount, and the policy can "sustain" until I'm 70, what happens later if i reach to 71 age, does my policy suddenly lapse ? how will i be notified and how much should i increase the premium then ? (Touch Wood) Lets say if i'm hospitalised at age 71, does it mean that my insurance is effectively lapse and I'm not insured? What happen to all the premiums i payed previously, does it not cover any of my hospital bill ?

Nowadays Insurance company are required to send you an annual statement to show when your policy is likely to end. You won't have "suddenly" kind of scenario unless you're ignorant to your annual statement (then you can't blame the insurance company because they've already gave you written notice and advise).

4) Scenario : Lets say i do increase the premium and policy can sustain longer, but what if (touch wood) I don't reach the supposedly extended period. What happens to the extra premiums I paid ? All wasted ?

Basically you're trying to say if "events" happen and an example, you died earlier, if your policy features Basic Sum Assured + Cash Value, means whatever you're covered for Death + Cash Value at that moment will be payable to your Nominee. So there is no "rugi"

This post has been edited by lifebalance: Aug 10 2021, 08:30 PM

Quote

Quote since on Goodwill basis,...will it impact the policy annual limits/lifetime limits?

since on Goodwill basis,...will it impact the policy annual limits/lifetime limits? Much better than some that has "Policyholders are entitled to claim hospitalisation reimbursement up to their annual limit and lifetime limit subject to the existing terms and condition of their medical plan."

Much better than some that has "Policyholders are entitled to claim hospitalisation reimbursement up to their annual limit and lifetime limit subject to the existing terms and condition of their medical plan." if your medical benefits has over >1 mil annual limit, that's not an issue.

if your medical benefits has over >1 mil annual limit, that's not an issue.

0.3070sec

0.3070sec

0.66

0.66

7 queries

7 queries

GZIP Disabled

GZIP Disabled