Hi bro...u hv very valid question..let me try to explain

In the comparison, the basis is not 300k, but the basis is paying RM3,080 monthly for next 10yrs...which is RM370k.

So, to answer your question, the actual basis is paying RM370k over 10 yrs, with “loan and invest” compared to “no loan, but invest by force-saving, by assuming u have taken the loan”

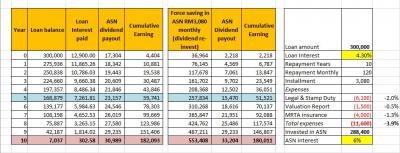

Option 1

Eventhough i could get 300k loan, but there is upfront fees i have to pay...one-time cost abt 12k to obtain this 300k.

300k-12k = 288k, which is the actual amount which i can invest in ASNB. Thats why on Day 1, my loan value is 300k but ASNB investment value is 288k. Then i work out the spreadsheet assuming mortgage interest 4.3% and ASBN dividend 6% (assume both constant over 10 years)

Option 2

I don’t take loan, instead invest every month RM3,080, which is the same amount i pay to bank if i took the loan. Which is forced-saving method. In this option, i not need to worry about BLR movement and ASBN dividend trend. Risk free option.

Conclusion

“Taking loan, invest, pay refinance installment of RM3,080” could gives almost same return after 10 yrs, compared to “No loan, invest RM3,080 monthly in ASBN”.

By the way, i might miss some important variable as i only did quick spreadsheet by considering basic variable only.

QUOTE(plumberly @ Nov 9 2017, 06:30 PM)

Interesting comparison.

But ....

if the purpose is to decide which option to go for, then I feel that the comparison is not comparing apple with apple.

Why? Different basis for the 2 options, both should have the same amount of money at the start.

Say DTrump has RM30k in hand. Should he go for the:

a. ASX loan and keep the RM30k in FD or ASX or

b. invest that RM30K with monthly contributions?

This to me is a fair comparison, I think.

My 1.5 cents.

Nov 7 2017, 02:27 PM

Nov 7 2017, 02:27 PM

Quote

Quote

.....terima kasih

.....terima kasih

0.3598sec

0.3598sec

0.44

0.44

7 queries

7 queries

GZIP Disabled

GZIP Disabled