QUOTE(samkps @ Apr 15 2015, 10:55 PM)

Oh... usual practice, 1/3 reserve...

Why they never advertise one?

I call them tomorrow..

EcoMajestic @ Semenyih (VERSION 7), ~Lets Continue Partyfor MerryDale~

|

|

Apr 15 2015, 11:21 PM Apr 15 2015, 11:21 PM

|

Junior Member

407 posts Joined: Jun 2009 |

QUOTE(samkps @ Apr 15 2015, 10:55 PM) Oh... usual practice, 1/3 reserve... Why they never advertise one? I call them tomorrow.. |

|

|

|

|

|

Apr 15 2015, 11:27 PM

|

Senior Member

15,454 posts Joined: Nov 2011 |

QUOTE(Mr Kong @ Apr 15 2015, 11:21 PM) Why they never advertise one? Lol.. too many demands but too less units available, what for need to spend budget for advertisement since it is already sold out... I call them tomorrow..  |

|

|

Apr 15 2015, 11:32 PM

|

|

Junior Member

407 posts Joined: Jun 2009 |

QUOTE(samkps @ Apr 15 2015, 11:27 PM) Lol.. too many demands but too less units available, what for need to spend budget for advertisement since it is already sold out... Yeah. You are right. But i am interested to purchase one unit leh.. |

|

|

Apr 15 2015, 11:56 PM

|

Senior Member

9,913 posts Joined: Jun 2014 |

QUOTE(Mr Kong @ Apr 15 2015, 10:25 PM) Hi there. May I know what were the launch price for the shoplot? They didn't advertise also... Price ranges from RM1388k to RM2739k. Only 102 units with 32 offered to existing purchasers. As the number of units are very limited that's why not publicly advertised. |

|

|

Apr 16 2015, 12:00 AM

|

|

Senior Member

9,913 posts Joined: Jun 2014 |

QUOTE(Mr Kong @ Apr 15 2015, 11:21 PM) Why they never advertise one? Call them also no use. Sure no more as I missed the boat and then asked them few times to confirm any drop out unit... I call them tomorrow.. |

|

|

Apr 16 2015, 12:36 PM

|

|

Senior Member

15,454 posts Joined: Nov 2011 |

QUOTE(Jasoncat @ Apr 16 2015, 12:00 AM) Call them also no use. Sure no more as I missed the boat and then asked them few times to confirm any drop out unit... purchaser mostly hardcore taikor... financial strong strong...  |

|

|

|

|

|

Apr 17 2015, 10:06 AM

|

|

Junior Member

225 posts Joined: Dec 2009 |

Guys, does it matter and which is better if just looking from the rate perspective and risk

Bank A 3.99 + 0.41 = 4.4 Bank B 3.15 + 1.25 = 4.4 This post has been edited by ckl1998: Apr 17 2015, 10:07 AM |

|

|

Apr 17 2015, 10:50 AM

|

|

Senior Member

15,454 posts Joined: Nov 2011 |

QUOTE(ckl1998 @ Apr 17 2015, 10:06 AM) Guys, does it matter and which is better if just looking from the rate perspective and risk Base rate derived from cost of fund + statutory reserve requirement --> Bank with lower cost of fund + strong reserve normally will have lower base rate. Bank A 3.99 + 0.41 = 4.4 Bank B 3.15 + 1.25 = 4.4 Spread derived from the operating cost, profit margin, customer's risk margin etc ---> Bank with higher spread means higher profit margin. If all other charges, terms and conditions are same for both banks, I will opt for bank B, coz still maybe have chance and room for me to negotiate with the bank for better rate (lower spread). |

|

|

Apr 17 2015, 10:57 AM

|

|

Senior Member

10,387 posts Joined: Dec 2011 |

QUOTE(samkps @ Apr 17 2015, 10:50 AM) Base rate derived from cost of fund + statutory reserve requirement --> Bank with lower cost of fund + strong reserve normally will have lower base rate. Instead, I will opt for A for stability. Spread derived from the operating cost, profit margin, customer's risk margin etc ---> Bank with higher spread means higher profit margin. If all other charges, terms and conditions are same for both banks, I will opt for bank B, coz still maybe have chance and room for me to negotiate with the bank for better rate (lower spread). Cost of fund reserve at 3.15% is seriously quite low and with current impact, GST, economy, Ringgit falling, group deposit posibly reducing and withdrawing, bank cost of a loan inclusive system maintenance, salary, etc the cost might be average at 3.5% to 3.6%, for most banks set up at 3.9-4%, it is a calculative risk and offers more stability if funds goes down further by this year, therefore, I opt for a lower spread rate instead of low Base Rate which is review every 3 mths. |

|

|

Apr 17 2015, 11:03 AM

|

|

Senior Member

10,387 posts Joined: Dec 2011 |

QUOTE(Jasoncat @ Apr 15 2015, 07:01 PM) Kenanga: Rising Eco World a ‘must-have’ stock Wow, interesting news on top of the 470 acres Batu Kawan land aquisition proposal to PDC. Fast-emerging property developer Eco World Development Group Bhd may rise to the top of the industry food chain over the next two years, says Kenanga Research today, tipping the counter as a “must-have” stock. In a report today, the research house noted the developer’s resilience against market-wide slowdown with its recent property launches seeing take-up rates between 80% and 100% compared to industry average of 50% to 60%. “We like the stock as a long-term value emerging stock given their aggressive growth path and management team,” said Kenanga. “Expect Eco World to be a ‘must-have’ stock as we will not be surprised if it becomes a market leader over the next two years.” Among others the research house tipped the management profile of Eco World, with strong experience in quality township planning, as a big draw among the property-buying crowd. At present Eco World’s remaining gross development value (GDV) comes to an estimated RM51.2 billion, of which 83.5% are either mixed developments or townships, according to Kenanga. The rest are industrial business parks. In terms of key personnel, former SP Setia chief of nearly 18 years Liew Kee Sin was re-designated board chairman in March. Another addition to the board was Liew’s long-time associate Voon Tin Yow – Liew’s former chief executive officer at SP Setia for the duration of the former’s stay — as executive director. Other prominent names in Eco World’s senior management lineup include industry veterans with former links to SP Setia as well, among others chief executive officer Chang Khim Wah and chief financial officer Heah Kok Boon. “We expect such profiling to translate into strong branding and demand for Eco World’s projects as property buyers these days are savvy and do their ‘research’ before making a purchase,” said Kenanga. “Thus, we believe Eco World will be gaining market share as buyers are aware that by buying Eco World products, project quality and delivery will be equally top-notch as Eco World is aiming to establish a branding strength with market leadership qualities.” ‘Liew reinstated as head’ In addition the redesignation of Liew as non-executive chairman from his previous non-executive directorship is crucial for Eco World, added the research house, as Liew is proposing a property-focused special purpose acquisition company (Spac) also bearing the Eco World brand. “The new position officially re-instates Liew’s role as a mentor, and head of the company, and he will also head the management team for the Spac,” said Kenanga. “This is crucial for the group, especially since Eco World has plans to acquire 30% of the Spac. The Spac will expand its wings to the United Kingdom and Australia.” To recap, in October 2014 Eco World announced its intention to subscribe to Liew’s proposed Spac, named Eco World International, to the tune of 30% equity for some RM562.5 million. This means the Spac is eyeing as much as RM1.9 billion in capital raised through its proposed listing. However a Business Times report in March this year quoted Liew as saying that the Spac will not be a blank-cheque initial public offering (IPO), rather listing with assets in hand. “We are awaiting the outcome of the IPO application to the Securities Commission.” “We will add more international projects to Eco World International as we move forward and the focus will still be in London and Australia,” said Liew as quoted by the paper. This is seen as an allusion to Liew’s personal joint venture with Irish developer Ballymore announced in January this year, worth some RM11.8 billion in estimated gross development value (GDV) through his personal vehicle Eco World Investment, to develop three residential property projects in London. Liew had previously said the joint venture may be injected into the Spac, which is eyeing a listing in the third quarter of this year. However the draft prospectus is not yet available on the Securities Commission’s website at publication time. ‘Phenomenal Sales' Eco World’s strong take-up rates came despite most of its property launches residing firmly outside the affordable price range, noted Kenanga today. The research house noted the company’s recent launches such as Eco Majestic, Eco Botanic, Eco Spring and Eco Business Park I had recorded “phenomenal sales”, achieving strong take-up within days of launching. While most of Eco World properties are priced above RM500,000 per unit, those that come under the RM1 million per unit mark are seeing take-up rates of over 97%, said Kenanga. As for properties priced above the RM1 million per unit threshold, the developer is seeing take-up rates from 80% to full take-up within one to two days of launching, added Kenanga. “This suggests that Eco World is hitting all the right notes with buyers in terms of pricing, product positioning as well as branding as take-up rates remain strong despite most units being priced outside the affordable range,” said Kenanga. Taking Johor by storm Kenanga took special note of Eco World’s strong inroads into the Johor property market in 2014 despite softening market conditions, which led to lower sales for other developers. In its report today, Kenanga said most developers under its coverage only managed full-year sales of between RM220 million and RM605 million in 2014. By contrast Eco World’s full-year sales in the state clocked in at RM1.8 billion in 2014, making up 57% of the developer’s total sales figure. “Property data showed that the higher absorption rates in the 3Q14 (at 11, below 10-yr average of 12) for Johor’s residential property also ties in with the timing of Eco World’s sales progress in Johor which jumped by RM1.2 billion from March 2014 to October 2014,” said Kenanga today. “However, 4Q14 saw lower absorption rates on the back of lower sales and higher incoming supply, while there were minimal new launches from Eco World (in that quarter),” added Kenanga. The developer’s success in Johor despite the lull period is likely due to its right positioning and pricing, opined Kenanga, noting among others that Eco World’s projects in Johor are seeing in excess of 80% in take-up rates. “As such, we believe Eco World may already be starting to steal market share from other developers in that region and has clearly demonstrated marketing abilities which set themselves apart from other developers,” said Kenanga further. |

|

|

Apr 17 2015, 03:59 PM

|

|

Senior Member

15,454 posts Joined: Nov 2011 |

QUOTE(Chris Chew @ Apr 17 2015, 10:57 AM) Instead, I will opt for A for stability. Chris gor, if the cost of fund is increased, the KLIBOR rate will definately increase as well.. If KLIBOR is increased, I presume Bank B will increase its Base rate also, no?Cost of fund reserve at 3.15% is seriously quite low and with current impact, GST, economy, Ringgit falling, group deposit posibly reducing and withdrawing, bank cost of a loan inclusive system maintenance, salary, etc the cost might be average at 3.5% to 3.6%, for most banks set up at 3.9-4%, it is a calculative risk and offers more stability if funds goes down further by this year, therefore, I opt for a lower spread rate instead of low Base Rate which is review every 3 mths. Klibor increase definately will give more severe impact to those banks with smaller deposit bases, higher current BR rate in this context, no?  |

|

|

Apr 17 2015, 08:04 PM

|

|

Junior Member

225 posts Joined: Dec 2009 |

QUOTE(samkps @ Apr 17 2015, 03:59 PM) Chris gor, if the cost of fund is increased, the KLIBOR rate will definately increase as well.. If KLIBOR is increased, I presume Bank B will increase its Base rate also, no? Very sorry. I quote the wrong infoKlibor increase definately will give more severe impact to those banks with smaller deposit bases, higher current BR rate in this context, no? Bank A 3.99 + 0.41 = 4.4 Bank B 3.20 + 1.25 = 4.45 Anyway, yeah, really want to understand one should focus more on BR or the spread in the event if both the effective rate is the same |

|

|

Apr 17 2015, 10:27 PM

|

|

Senior Member

9,913 posts Joined: Jun 2014 |

QUOTE(samkps @ Apr 17 2015, 10:50 AM) Base rate derived from cost of fund + statutory reserve requirement --> Bank with lower cost of fund + strong reserve normally will have lower base rate. Samkor, Base Rate is comprised of benchmark cosf of fund + SRR. Most banks (if I remember correctly, up to 90%) use 3M KLIBOR as the benchmark COF. So irrespective of the actual COF whether high or low, since it is to be based on the benchmark COF, it doesn't mean that bank with lower actual COF will have lower BR.Spread derived from the operating cost, profit margin, customer's risk margin etc ---> Bank with higher spread means higher profit margin. If all other charges, terms and conditions are same for both banks, I will opt for bank B, coz still maybe have chance and room for me to negotiate with the bank for better rate (lower spread). On the part of the spread, it will be maintained throughout the loan tenure unless - so fat hope for better spread |

|

|

|

|

|

Apr 17 2015, 11:58 PM

|

|

Senior Member

15,454 posts Joined: Nov 2011 |

QUOTE(Jasoncat @ Apr 17 2015, 10:27 PM) Samkor, Base Rate is comprised of benchmark cosf of fund + SRR. Most banks (if I remember correctly, up to 90%) use 3M KLIBOR as the benchmark COF. So irrespective of the actual COF whether high or low, since it is to be based on the benchmark COF, it doesn't mean that bank with lower actual COF will have lower BR. Jason gor, if KLIBOR is used as benchmark COF, isn't it supposed to be same across all the banks, as it is an average value? Then how come every bank has its own BR On the part of the spread, it will be maintained throughout the loan tenure unless - so fat hope for better spread I thought Base Rate is the "benchmark cost of fund of the bank itself" in reference to KLIBOR, no? That's why different bank has different actual COF and hence different BR, no? If BR = 3M KLIBOR + SRR, then the variation of BR will only rely on the SRR. This post has been edited by samkps: Apr 18 2015, 12:20 AM |

|

|

Apr 18 2015, 01:08 AM

|

|

Senior Member

9,913 posts Joined: Jun 2014 |

QUOTE(samkps @ Apr 17 2015, 11:58 PM) Jason gor, if KLIBOR is used as benchmark COF, isn't it supposed to be same across all the banks, as it is an average value? Then how come every bank has its own BR Samkor, theoretically all the banks that use KLIBOR are supposed to have the same BR. I believe the difference could be due to the timing they captured the data and submitted to Bank Negara last year. Also it is possible that the difference in the way they do the computation resulted in different BR. That explains why the BR of most banks are quite close as you can see here I thought Base Rate is the "benchmark cost of fund of the bank itself" in reference to KLIBOR, no? That's why different bank has different actual COF and hence different BR, no? If BR = 3M KLIBOR + SRR, then the variation of BR will only rely on the SRR.

The BR could have changed now as the banks are only required (by Bank Negara) to keep the BR unchanged for the first 3 months. BR = 3M KLIBOR + SRR, so the variation of BR relies on both KLIBOR and SRR (not just only on SRR). |

|

|

Apr 18 2015, 01:23 AM

|

|

Senior Member

9,913 posts Joined: Jun 2014 |

QUOTE(Chris Chew @ Apr 17 2015, 11:03 AM) Wow, interesting news on top of the 470 acres Batu Kawan land aquisition proposal to PDC. I personally think that EW will buck against the trend and be one of the top developers (if not the only one) with strong sales this year. Went to IProperty expo today (Friday) - they are still very confident of good sales performance. |

|

|

Apr 18 2015, 07:51 AM

|

|

Junior Member

225 posts Joined: Dec 2009 |

QUOTE(Jasoncat @ Apr 18 2015, 01:08 AM) Samkor, theoretically all the banks that use KLIBOR are supposed to have the same BR. I believe the difference could be due to the timing they captured the data and submitted to Bank Negara last year. Also it is possible that the difference in the way they do the computation resulted in different BR. That explains why the BR of most banks are quite close as you can see here So theory wise and long term wise, should seek for lowest spread possible as BR will move no matter how?

The BR could have changed now as the banks are only required (by Bank Negara) to keep the BR unchanged for the first 3 months. BR = 3M KLIBOR + SRR, so the variation of BR relies on both KLIBOR and SRR (not just only on SRR). |

|

|

Apr 18 2015, 08:53 AM

|

|

Senior Member

15,454 posts Joined: Nov 2011 |

QUOTE(Jasoncat @ Apr 18 2015, 01:08 AM) Samkor, theoretically all the banks that use KLIBOR are supposed to have the same BR. I believe the difference could be due to the timing they captured the data and submitted to Bank Negara last year. Also it is possible that the difference in the way they do the computation resulted in different BR. That explains why the BR of most banks are quite close as you can see here Jason gor, thanks for the information...

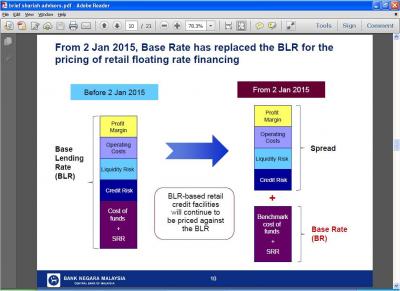

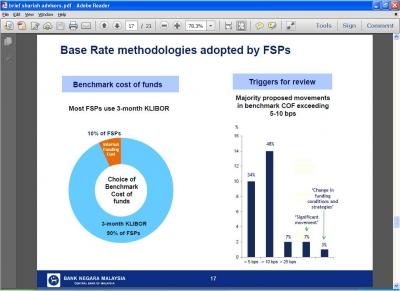

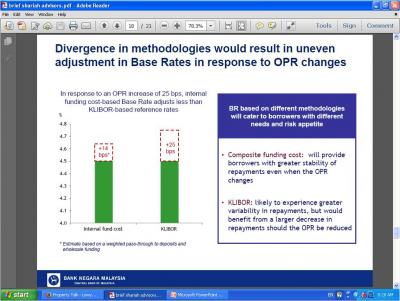

The BR could have changed now as the banks are only required (by Bank Negara) to keep the BR unchanged for the first 3 months. BR = 3M KLIBOR + SRR, so the variation of BR relies on both KLIBOR and SRR (not just only on SRR).  Have done some reading and there is clearer picture now.. BR = Benchmark cost of fund + SRR Spread = profit margin + operating cost + credit risk + liquidity risk There are 3 types of reference rate - base rate, benchmark cost of fund, actual cost of fund index. All three have strong correlations with COF. Apparently, the approach adopted by Bank Negara is Reference rate = Benchmark cost of fund + SRR. Bank Negara gives flexibility to the bank to adopt their choice / methodology of Benchmark Cost of Fund. 90% bank choose to use 3M KLIBOR as Benchmark COF, but there is still 10% banks choose to use "Internal Funding Cost" as the Benchmark COF instead. I think the obvious case here would be Maybank, due to their super low BR (3.2%), I suspect they are not using the 3M KLIBOR as the Benchmark COF. Public bank maybe another case as well. Therefore, the divergence in base rate methodologies could lead to uneven adjustment to base rate when there is changes in OPR or KLIBOR. Bank Negara expects that Internal funding Cost-based BR shall be adjusted less than the KLIBOR-based BR. Majority banks propose that when there is a change of 5-10 base points in the benchmark of COF, it will trigger the change of the BR. Notes: 1.) I presume the formula that is being used by the banks for calculating the BR all are same. The variation only rely on which type of benchmark cost of funding the bank is using - either internal fund or KLIBOR. 2.) I presume Bank Negara also provide a time frame for the banks to capture the KLIBOR data. They cannot varies too much between different banks within the same time frame. Therefore, I believe the variation in BR for different banks that adopt the KLIBOR-based COF mostly is due to the SRR components. SRR is the fund deposited to the Central Bank according to the bank liability. Therefore, I believe the variation in bank liability is much higher compare to the KLIBOR and hence carry more weightage in terms of BR variation. This post has been edited by samkps: Apr 18 2015, 09:20 AM Attached thumbnail(s)

|

|

|

Apr 18 2015, 09:09 AM

|

|

Senior Member

15,454 posts Joined: Nov 2011 |

QUOTE(ckl1998 @ Apr 18 2015, 07:51 AM) So theory wise and long term wise, should seek for lowest spread possible as BR will move no matter how? Not quite.... Take your example: Before OPR change: Bank A 3.99 + 0.41 = 4.4 Bank B 3.15 + 1.25 = 4.4 After OPR raise up 25 base points: Bank A (3.99 + 0.25) + 0.41 = 4.65 Bank B (3.15 + 0.25) + 1.25 = 4.65 BR movement depends on the benchmark COF, nothing related to the spread portion. Bank Negara projected that those bank using the internal funding-based benchmark COF shall be more resilient to BR changes in case there is any OPR rate change, compared to those adopt KLIBOR-based. Nevertheless, I still believe the banks can offer a better Spread rate for their premier customer. BR depends on the benchmark COF and can't change if there is nothing change in OPR/KLIBOR. Bank can alter or change the Spread rate instead, depending on the credit risk profile of the borrower... This post has been edited by samkps: Apr 18 2015, 09:29 AM |

|

|

Apr 18 2015, 10:38 AM

|

|

Senior Member

9,913 posts Joined: Jun 2014 |

QUOTE(samkps @ Apr 18 2015, 08:53 AM) Jason gor, thanks for the information... Samkor, impressed Have done some reading and there is clearer picture now.. BR = Benchmark cost of fund + SRR Spread = profit margin + operating cost + credit risk + liquidity risk There are 3 types of reference rate - base rate, benchmark cost of fund, actual cost of fund index. All three have strong correlations with COF. Apparently, the approach adopted by Bank Negara is Reference rate = Benchmark cost of fund + SRR. Bank Negara gives flexibility to the bank to adopt their choice / methodology of Benchmark Cost of Fund. 90% bank choose to use 3M KLIBOR as Benchmark COF, but there is still 10% banks choose to use "Internal Funding Cost" as the Benchmark COF instead. I think the obvious case here would be Maybank, due to their super low BR (3.2%), I suspect they are not using the 3M KLIBOR as the Benchmark COF. Public bank maybe another case as well. Therefore, the divergence in base rate methodologies could lead to uneven adjustment to base rate when there is changes in OPR or KLIBOR. Bank Negara expects that Internal funding Cost-based BR shall be adjusted less than the KLIBOR-based BR. Majority banks propose that when there is a change of 5-10 base points in the benchmark of COF, it will trigger the change of the BR. Notes: 1.) I presume the formula that is being used by the banks for calculating the BR all are same. The variation only rely on which type of benchmark cost of funding the bank is using - either internal fund or KLIBOR. 2.) I presume Bank Negara also provide a time frame for the banks to capture the KLIBOR data. They cannot varies too much between different banks within the same time frame. Therefore, I believe the variation in BR for different banks that adopt the KLIBOR-based COF mostly is due to the SRR components. SRR is the fund deposited to the Central Bank according to the bank liability. Therefore, I believe the variation in bank liability is much higher compare to the KLIBOR and hence carry more weightage in terms of BR variation.  prof really pro prof really pro Oh yeah, I missed out MBB which I believe it uses blended COF (the actual COF) instead of KLIBOR as its reference. So its BR rate is supposed to be closer to FD/CASA. Theoretically, banks like MBB that uses blended COF may see relatively less volatility in their BR as its liability components which comprises FD will be repriced slower. This implies 2 things - if OPR hikes, then its BR will adjust up slower / smaller and vice versa. Nevertheless, since I / we do not have the privy access to their BR computation methodology, I presume the BR adjustment is elastic and timely to reflect the change in some key reference rate, eg OPR which will have widespread effect to all the funding cost. For banks that have effective cost control this will give them more room to play around with their spread and remain competitive in the market. As for your presumption stated in the 2nd part of your note, in terms of quantum different banks will have different amount of statutory funds to be kept but same rate 4% applied across all banks. Naturally banks with higher eligible liability will have higher funds to be reserved for that regulatory purpose. But again, how significant is the weightage of it in BR calculatotion will depend on the methodology used by each banks. This post has been edited by Jasoncat: Apr 18 2015, 10:53 AM |

| Change to: |  0.0307sec 0.0307sec

0.56 0.56

6 queries 6 queries

GZIP Disabled GZIP Disabled

Time is now: 14th December 2025 - 09:12 AM |

Quote

Quote