domestic helper - RM3.5k per month - (can consider to do it yourself and take it as exercise, until when you are physically not able to, can try consider check in to old folks home, maybe cheaper and easier that way)

physiotherapy for 2 - RM1k per month (start exercising and live healthier lives now and very high chance you won't need any physio at all)

supplement for 2 - RM500 (milk powder, omega, vitamins, ect) - just eat healthy and normal and probably you won't need supplement?

but it's good that you plan and allocate for that, i'll take note of that too to put aside, who knows...it's always good to prepare for the worst but also we can try prevent or minimize chances of it happening by taking actions now too...

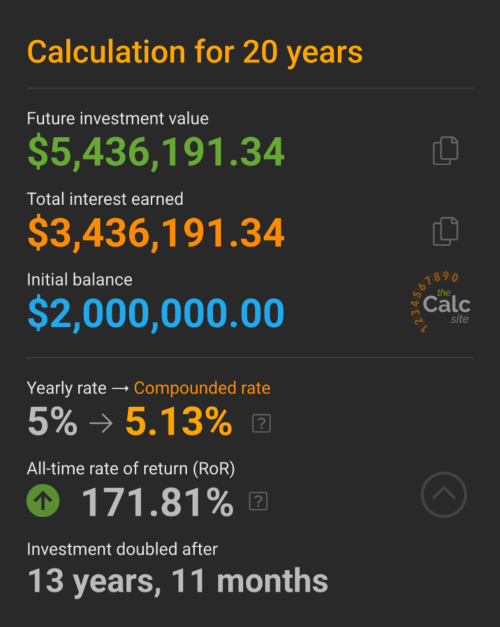

2.5 million is our goal if we want to retire comfortable now

i use to focus on 1.5M but after knowing that medical cost is so expensive i think 2.5M is needed

even with insurance it wont help especially when you old you need to take supplement, you need physiotherapy, you need domestic helper

i start to plan all this as now i am at 52 this year and why 1.25M per person as i need to cover for my wife so i need to have 2.5M for 2

future cost in 10 years - hopefully this number maintains!

domestic helper - RM3.5k per month

physiotherapy for 2 - RM1k per month

insurance for 2 - RM1.2k per month

tnb - RM500 per month

water bill - RM50 per month

supplement for 2 - RM500 (milk powder, omega, vitamins, ect)

medicine for 2 - RM500 (depend on your sickness - just assume u have heart problem, cholesterol problem, diabetic problem, high bp)

phone bill for 2 - RM100

unifi - RM150

other misc - RM1000 (clinic visit, travel cost)

makan for 3 - RM3000 (me, my wife, domestic helper)

Total 11.5k

Estimate i think on the safe side just make sure put 15k per month for expenses

2.5M x 5.5% = RM137,500 per year dividend

137500 / 12 = RM11458 per month so need to take out additional 3.5k per month to top it up until RM15k per month

chatgpt projected as long as i have 2.5M and i consistently withdraw RM15k per month and with dividend of 5.5% after 20 years i should still have 900k left...

if you think the above number is not realistic i really welcome you to comment so i can adjust and plan accordingly

i have 8 more years till retirement but if i continue to work for the next 8 years and do not withdraw any money from EPF and continue to slowly pump like RM10k per year i might hit it base on my calculation

Jun 6 2025, 12:51 PM

Jun 6 2025, 12:51 PM

Quote

Quote

0.0552sec

0.0552sec

0.47

0.47

7 queries

7 queries

GZIP Disabled

GZIP Disabled