QUOTE(Sumofwhich @ Feb 21 2020, 04:59 PM)

"in times of needs", prolly property or hospital medical bills

Leverage model from EPF. Not that hard.Private Retirement Fund, What the hell is that??

|

|

Feb 21 2020, 05:15 PM Feb 21 2020, 05:15 PM

Return to original view | IPv6 | Post

#1

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(Sumofwhich @ Feb 21 2020, 04:59 PM) "in times of needs", prolly property or hospital medical bills Leverage model from EPF. Not that hard. |

|

|

|

|

|

Mar 13 2020, 06:10 PM

Return to original view | IPv6 | Post

#2

|

|

All Stars

12,387 posts Joined: Feb 2020 |

For those who are eyeing for CIMB-Principal PRS Plus Asia Pacific Ex Japan Equity - Class C, now should be a good time.

Its NAV has dropped to 0.9296. |

|

|

Mar 13 2020, 10:20 PM

Return to original view | IPv6 | Post

#3

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(cempedaklife @ Mar 13 2020, 07:30 PM) I was happily topping up rm50 each time several times until recent days.a bit unsure now For me, buying PRS is just meant for tax deduction.This post has been edited by GrumpyNooby: Mar 13 2020, 10:21 PM |

|

|

Mar 13 2020, 10:22 PM

Return to original view | IPv6 | Post

#4

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(cempedaklife @ Mar 13 2020, 10:21 PM) But its good to get low entry price what It won't matter much since you're very likely to keep it for 20 to 30 years until you reach your golden age. |

|

|

Mar 13 2020, 10:34 PM

Return to original view | IPv6 | Post

#5

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(cempedaklife @ Mar 13 2020, 10:28 PM) Then i dunno why you said now is a good time lol. Since entry price is not a concern lol. It may not applicable to you. Since it's on the downward trend, I'm just saying now could be a good entry. I cannot see the future and I don't know upcoming NAV. This is the lowest NAV I saw so far since the beginning of 2020. |

|

|

Mar 16 2020, 05:20 AM

Return to original view | IPv6 | Post

#6

|

|

All Stars

12,387 posts Joined: Feb 2020 |

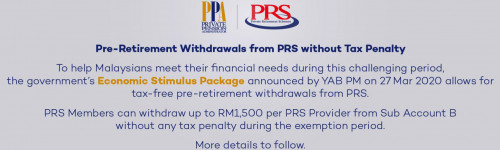

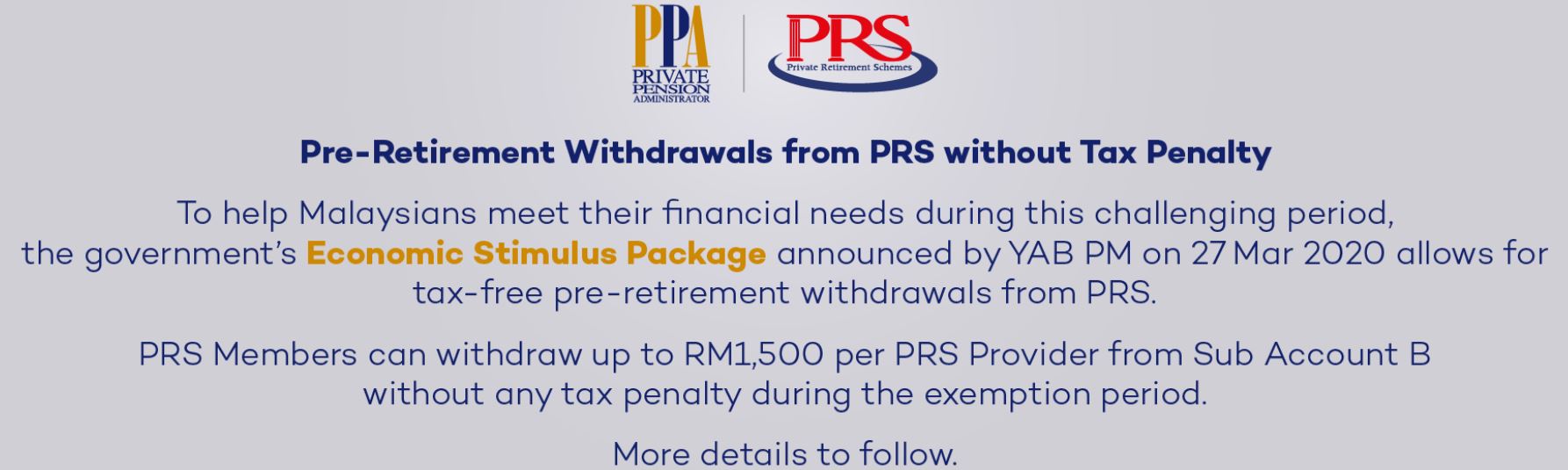

Dear PRS Member,

Effective 15 March 2020, PRS Members can make pre-retirement withdrawals from PRS for the purposes of housing and healthcare without tax penalty, as announced in Budget 2020. This move will help Malaysians to use a portion of their retirement savings for their needs. Withdrawals will come from Sub Account B, which holds 30 percent of PRS Members’ savings. In recognition of rising healthcare cost, withdrawal for immediate family members is also allowed and can be used to cover 91 types of illnesses, including the cost of medical equipment or medication for the approved illnesses. For housing, withdrawals can be made to buy or build a house as well as to reduce or redeem a housing loan. Below is a list of forms, guides and documents which you can download to facilitate your withdrawal application. If you have a question that is not answered in the FAQ, you can call PPA at 1300-131-772 for further assistance on this withdrawal measure. |

|

|

|

|

|

Mar 16 2020, 09:42 AM

Return to original view | Post

#7

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(wongmunkeong @ Mar 16 2020, 09:35 AM) thank U for the useful info sharing GrumpyNooby, I copied from the mailer from PPA. Don't thank me! |

|

|

Mar 28 2020, 10:07 PM

Return to original view | IPv6 | Post

#8

|

|

All Stars

12,387 posts Joined: Feb 2020 |

|

|

|

Apr 1 2020, 12:07 PM

Return to original view | IPv6 | Post

#9

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(GrumpyNooby @ Mar 28 2020, 10:07 PM) https://www.ppa.my/wp-content/uploads/2020/...Tax-Penalty.pdf Good thing is: What is the maximum withdrawal amount I can make for this temporary relief? Members may request for withdrawal from one or more funds managed by each PRS Provider to a maximum amount of RM1,500 per Provider. This post has been edited by GrumpyNooby: Apr 1 2020, 12:08 PM |

|

|

Apr 1 2020, 01:05 PM

Return to original view | IPv6 | Post

#10

|

|

All Stars

12,387 posts Joined: Feb 2020 |

Wondering if FSM can help to process the withdrawal or do I need to go deal with the PRS provider myself?

|

|

|

Apr 1 2020, 05:17 PM

Return to original view | IPv6 | Post

#11

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(markedestiny @ Apr 1 2020, 05:16 PM) You mean for subsequent buys, even after you have opened account with FSM? He's answering my question on the special withdrawal. Not related to usual buy order via FSM. |

|

|

Apr 1 2020, 08:15 PM

Return to original view | IPv6 | Post

#12

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(markedestiny @ Apr 1 2020, 07:14 PM) Ok, similar process with eUT which I am using. Hopefully these two platforms could automate more of the manual processes. eUT has been spamming with the same email!  |

|

|

Apr 1 2020, 08:55 PM

Return to original view | IPv6 | Post

#13

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(cempedaklife @ Apr 1 2020, 08:52 PM) I think its more to do with the fundhouse If you're planning to buy PRS funds from either Affin Hwang, Kenanga, or Principal PRS, with FSM, no forms are required. https://www.fundsupermart.com.my/fsmone/art...cipal-PRS-Funds This post has been edited by GrumpyNooby: Apr 1 2020, 08:56 PM |

|

|

|

|

|

Apr 3 2020, 08:14 AM

Return to original view | IPv6 | Post

#14

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(ben3003 @ Apr 3 2020, 08:08 AM) why no give step to withdraw one.. PPA asked you to deal with your PRS provider. PPA is not going to deal with you directly. 3. What is the maximum withdrawal amount I can make for this temporary relief? Members may request for withdrawal from one or more funds managed by each PRS Provider to a maximum amount of RM1,500 per Provider. For more information or assistance on the withdrawal application process, members may contact their respective PRS Providers via the following channels: |

|

|

Apr 8 2020, 12:27 PM

Return to original view | IPv6 | Post

#15

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(tehoice @ Apr 8 2020, 12:23 PM) i did a brief calculation of how much my account has made (pure profit for 2019), since don't have the actual official numbers on my profit. I bought one PRS fund in 2015. Simple ROI without considering MWA via DCA/RSP effect is close to break even.The recent market tumbles wiped out all of my profits made for 2019. despite that, when you withdraw, you are merely withdrawing your past years' profit and you still let your capital run in it. at least for my case lah. Yes, now is really a buy high and sell low situation, but my own argument is, look back at the main reason for me to invest into PRS and that is the tax relief of 3k each year. Now that you're able to withdraw at least some money back at no penalty, why not take this chance and cash it out a little. so the cash out from account B is merely withdrawing some of the profits that you have made in your past years. Minus the investment concept, letting the monies remain in your account, be it, EPF or PRS, is because you want to let the magic of compounding to work for your future retirement pot. i assume your EPF will certainly has much bigger pot of money and the compounding effect can definitely works better than your money does in the PRS right? (let's just assume, say 5% p.a. for each). So let's say you have 2 providers and both also more than RM1500 in your account, won't you withdraw RM3k from PRS instead of EPF? If I withdraw RM 1500 now, what profit am I withdrawing? If settlement date falls at the wrong date, I'm selling the fund in loss. Am I right? |

|

|

Apr 8 2020, 12:38 PM

Return to original view | IPv6 | Post

#16

|

|

All Stars

12,387 posts Joined: Feb 2020 |

There's no right or wrong. It's just a personal preference.

For me since it's an investment over time horizon, I won't consider tax relief as an input for portfolio gain/loss calculation. This post has been edited by GrumpyNooby: Apr 8 2020, 12:47 PM |

|

|

Apr 8 2020, 01:04 PM

Return to original view | IPv6 | Post

#17

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(Thrust @ Apr 8 2020, 01:04 PM) I would like to know if we withdraw RM1,500 from PRS account 2 in 2020, and subsequently perform a top-up self contribution of RM3,000 in Q4 of 2020,... will I still be entitled for a tax rebate on the RM3,000 being top-up made in year 2020? YesPPA said the pre-retirement special withdrawal is going to be tax free:  https://www.ppa.my/wp-content/uploads/2020/...Tax-Penalty.pdf This post has been edited by GrumpyNooby: Apr 8 2020, 01:06 PM |

|

|

Apr 8 2020, 01:11 PM

Return to original view | IPv6 | Post

#18

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(Thrust @ Apr 8 2020, 01:10 PM) Hi, No details yet from LHDN as per the forumer said.Sorry but I am not asking about it being tax free. I wanted to withdraw the RM1,500 and later just top up another RM1,500 to make it a sum of RM3,000. This RM3,000 I plan to put back in to PRS to enjoy tax exemption in 2020. You can wait for LHDN for further details. Whether the tax relief is going to be RM 3000 or RM 4500 (like SSPN implementation). This post has been edited by GrumpyNooby: Apr 8 2020, 01:12 PM |

|

|

Apr 8 2020, 01:13 PM

Return to original view | IPv6 | Post

#19

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(MUM @ Apr 8 2020, 01:12 PM) just an added note to take note in the link... Go ask PPA."Note: One of the prevailing terms and conditions for pre-retirement withdrawal from sub-account B is still applicable, whereby such withdrawals may only be made from a PRS fund one year after enrolment." so does it clearly mentioned that, in order to get the tax relief of RM3000 for this year's contribution, does one need to put in only RM3000 or (RM3000 + what ever that had been withdrawn under this special perks)? I did reply one post above. |

|

|

Apr 8 2020, 05:16 PM

Return to original view | IPv6 | Post

#20

|

|

All Stars

12,387 posts Joined: Feb 2020 |

QUOTE(iamkid @ Apr 8 2020, 05:13 PM) Cant find any option to withdraw/sell PRS in Fundsupermart FSM Manual process15.7 Can I sell my PRS funds? Yes, you can sell your units in Account B after 1 year of your subscription. You will need to submit a copy of fund house redemption form to process the withdrawal. Please be noted that a tax penalty of 8% will occur to you by to Inland Revenue Board of Malaysia unless your age is 55 and above. The PPA pre-retirement redemption fee of MYR 25.00 is waived by PPA until further notice. For account A, you can only redeem your PRS investments upon retirement age of 55. Redemption for a deceased member or permanent departure of a member from Malaysia are required to furnish documents which required by PPA. You may click here to view the details. https://www.fundsupermart.com.my/fsmone/fun...ment-Scheme-PRS |

| Change to: |  0.1293sec 0.1293sec

0.73 0.73

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 14th December 2025 - 08:36 AM |

Quote

Quote