Congrats on the new thread and thank you for keeping the thread tidy

👍

This post has been edited by lifebalance: Jan 31 2021, 11:02 AM

Insurance Talk V7!, Your one stop Insurance Discussion

Insurance Talk V7!, Your one stop Insurance Discussion

|

|

Jan 31 2021, 11:02 AM Jan 31 2021, 11:02 AM

Return to original view | Post

#1

|

All Stars

10,162 posts Joined: Nov 2014 |

Congrats on the new thread and thank you for keeping the thread tidy

👍 This post has been edited by lifebalance: Jan 31 2021, 11:02 AM |

|

|

|

|

|

Jan 31 2021, 11:12 AM

Return to original view | Post

#2

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(MUM @ Jan 31 2021, 11:04 AM) PIAM: Medical and health policies do not provide coverage for Covid-19 Thanks for sharing. This will help affirm consumers that if they're seeking for a coverage for covid 19, they'll need to opt for life companies.Adeline Paul Raj 19 hrs ago as of from 31 Jan 2021 11am KUALA LUMPUR (Jan 30): Medical and health insurance policies issued by general insurance companies do not provide coverage for pandemics such as Covid-19, the General Insurance Association of Malaysia (PIAM) said today. “The reason for this is that pandemics have been assumed as a rare event and thus, the absence of wide coverage under most policies. Pandemics are generally a risk with high exposure. As insurance premiums will commensurate with the risk exposure, insurance premiums will naturally be higher if a pandemic is covered,” it said. more.... https://www.msn.com/en-my/money/topstories/...w?ocid=msedgntp  |

|

|

Jan 31 2021, 12:55 PM

Return to original view | Post

#3

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(ckdenion @ Jan 31 2021, 12:52 PM) once a thread reaches 1250 posts, need to "migrate" to a new thread. Don't think that's the real reason, some threads has 250 pages ~ 850 pages But then again, how is this related to insurance talk ? XD I think it's good to start in a new thread otherwise if you want to search through 500 pages of post, no one will bother to, lol This post has been edited by lifebalance: Jan 31 2021, 12:56 PM |

|

|

Jan 31 2021, 04:14 PM

Return to original view | Post

#4

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(Pohziliang96 @ Jan 31 2021, 03:41 PM) New thread wow 1. Life insurance if you got debts to settle and wish to pass down the assets debt free to charity or extended familyIf I’m gonna be alone forever(no kids, wife), should I buy life insurance? Or medical card is enough? 2. The life insurance normally comes with total permanent disability so if you want to take care of yourself should you be disabled permanently one day, then the insurance payout will help with your living expenses You may also want to look into personal accident coverage. Which covers into loss of any one limbs, accidental death. 3. Critical Illness if you wish to cover in the event you're unable to work for a period of time due to critical illnesses, the payout will be able to help you pay off your living expenses 4. Medical card basically pays for the hospitalization fee only. What happens after you are discharged / finish with follow up is pretty much on how healthy is your cash flow. This post has been edited by lifebalance: Jan 31 2021, 04:22 PM woe.com liked this post

|

|

|

Jan 31 2021, 04:25 PM

Return to original view | Post

#5

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(Pohziliang96 @ Jan 31 2021, 04:19 PM) thanks for sharing It's definitely more than just a medical card which is just one aspect in insurance planning. I always thought a medical card is already sufficient Seems like I’m wrong now Thanks Hence its always advisable to get a comprehensive plan so that all aspect are covered. |

|

|

Jan 31 2021, 09:31 PM

Return to original view | Post

#6

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(TaiGoh @ Jan 31 2021, 08:19 PM) Hi guys, 1. Depends on how long you plan to stay with this company [Possible scenarios: Laid off/Change of job instead of retirement]Currently holding a SmartProtect Essential with SmartMedic Xtra plan with Great Eastern since 2012. Thinking to spend some time to review the insurance plan that I bought because normally I just follow what insurance agent suggested. Currently is 32 years old, working low risk job, non-smoker. Want to ask a few questions hope sifus here can clear my doubts: 1. If my company provide a company medical card with 80k annual limit, is that okay to sign up for deductible plan with deductible 80k for example? I assume I can change plan in the future to non-deductible plan without issue right (For example when I retired)? 2. Just wondering is there a way we can 'DIY' to compare the plans offered by different companies, or we straight talk to agent and ask for quotation then compare? 3. Personally prefer Prudential or AIA over Great Eastern. Just wondering is that still worth to switch since I already holding a policy with Great Eastern? I assume the benefits, premium, and claiming process should be almost the same across these three companies right? 4. What is the recommended R&B, I assume RM150 will be too low and RM200 onwards should be acceptable right? Thanks a lot! That being said, it'll be subject to your health at later part of your life if you'd like to change it back to a lower or non-deductible plans. There is however a plan that allows you to convert to a non-deductible @ Age 60 which is Allianz atm. 2. Consult a Financial Adviser Representative and they'll be able to give you a non-bias fair comparison  3. Premium is not necessary the same as the cost of insurance is different for each company as well as the benefits. For a better comparison and review, best to consult a Financial Adviser. 4. That depends on what's your expectation from your insurance policy to payout to you when you're hospitalized. Will you be satisfied if the insurance company pays only RM150 at the moment? if not, what will be the amount that you're happy with ? Again that could boil down to the level of care that you want the hospital to provide to you without you having to fork out extras for it. Hope that answers your questions. |

|

|

|

|

|

Jan 31 2021, 09:54 PM

Return to original view | Post

#7

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(YoungLee @ Jan 31 2021, 09:33 PM) can insurance be used to buy funeral services? Estimated RM50k total. You can use it for funeral expenses purposes.How fast does the beneficiary get the payout once someone is dead As for the death claim timeframe, it ranges from 9 working days - TBC depending on whether the case involves any investigation or it's very straight forward case However, the above timeframe is not general, depends on how quick you can assemble the docs as well and hand in. Some death claim benefit can be rejected due to: 1. the cause of death does not under the ambit policy/contract/certificate’s benefit, 2. breach of terms and conditions under the policy/contract/certificate, 3. death due to suicide within the specified time-frame mentioned under the terms and conditions of the policy/contract/certificate. (Commonly this would be for a-12 month period), 4. policy/contract/certificate is not in-force, 5. non-disclosure or incorrect information provided at time of proposal/application, 6. pre-existing conditions (depending on the terms and conditions of the policy/contract/certificate). What doc you need to prepare for Death Claim? 1. Claimant Statement – Death Claim 2. Certified Death Certificate 3. Claimant's proof of relationship to the Deceased (i.e. marriage certificate, birth certificate, etc.) 4. Certified IC of Claimant 5. Policy Contract / Bond of Indemnity with Stamp Duty Additional documents for death occurring within 2 years from date of issue or reinstatement: 1.Attending Physician’s Statement - Death 2. 5 copies of Consent Form & Patient’s Card Additional document for Accidental Death: 1. Certified Police Report 2. Certified Third Party Police Report (if any) 3. Certified Post-mortem & Toxicology report 4. Certified Burial Permit 5. Newspaper cutting (if any) Additional document if death occurred in overseas: 1. Certified JPN Letter 2. Certified death certificate issued by the country where the Assured had passed away This post has been edited by lifebalance: Jan 31 2021, 09:55 PM |

|

|

Feb 1 2021, 08:56 AM

Return to original view | Post

#8

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(TaiGoh @ Jan 31 2021, 11:12 PM) Thanks lifebalance and lifebalance for your reply! 1. If you're using a deductible plan, you'll be forced to use your company card first otherwise you'll have to pay fork out to pay for the deductible before the deductible medical card can be used.The reason I ask for a deductible plan is because I would assume that deductible plan premium will be a lot cheaper than non-deductible plan. So I just wondering is that a good idea to opt for a deductible plan since company already provided the benefits, then the premium saved can be utilized somewhere else. Or normally when hospitalization needed, it will be always advisable to use personal medical card first then followed by company medical card when over limit? I am not so worried about I got laid off, but change of job could be possible. I not sure how the policy works but just wondering whether it is possible to adjust the deductible amount or even adjust to a non-deductible plan in the future. And whether worth it to do so? And I assume that there will be no waiting period and contestability period need to be served in this case if within the same company? Thanks! As mentioned in the earlier post, as long as you're still healthy, you can make a request to change by re-declaring your health status at that point of time, if the insurance company finds it unfavorable then they'll reject your application to change the deductible to a non-deductible plan. So if you have a 80k deductible plan for example then you'll be forced to pay the 80k upfront first before the balance is covered by the insurance company throughout your policy lifetime. On the other side of the coin, you pay a low premium for your insurance but at the same time, will it be worth paying 80k upfront? QUOTE(MUM @ Feb 1 2021, 08:46 AM) Thanks for the inputs. That depends on what is offered by the insurance company for the 80k deductible. (Different company have different % of discount)Btw, what is the variance In premium per year between a 80k deductible n a non deductible plan for his age? For example, the normal premium is RM1,000 monthly, but someone with an 80k deductible could be paying RM200 monthly. |

|

|

Feb 1 2021, 10:34 AM

Return to original view | Post

#9

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(ckdenion @ Feb 1 2021, 09:43 AM) bro, which company has 80k deductible plan btw? nah doesn't exist, only giving it as an example.The highest deductible you can set now is either 75k - 100k QUOTE(YoungLee @ Feb 1 2021, 09:51 AM) It will take a long time to get the money lol? So basically is like a reimbursement right? Need to pay out of pocket for funeral expense, then only claim back from insurance payout This is not considered a "reimbursement", it's a payout from the policy benefit. Consider that the policy has been fulfilled by the insurance company once the insured has passed away.QUOTE(MUM @ Feb 1 2021, 10:04 AM) that is one of the selling points of UBB trust as mentioned... If you have a trust set up, the payment of funds will be much faster as the money is already there, and you'll just need to submit the necessary documents for the trust to hand out the money. (This is provided you have park some initial asset/cash into the trust).Why Should I establish a UBB CASH TRUST today? It provides swift cash for expenses during emergencies and to tide your family over until the insurance payout and access to your money in your bank accounts or will. This cash can also be used to pay legal fees to access any inheritances and bereavement-related expenses. However if your trust depends on insurance payout, the processing time is similar to what I've mentioned earlier. This post has been edited by lifebalance: Feb 1 2021, 10:40 AM |

|

|

Feb 2 2021, 03:01 PM

Return to original view | IPv6 | Post

#10

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(Pohziliang96 @ Feb 2 2021, 01:58 PM) Hey I’m back You may want to get a few quote or check out the online brochures directly with the insurance company and do your own studies.May I know which products provide more coverages? Like including medical and personal accident. And I’m not living in a city. The nearest bank I could reach is Maybank. Can I buy ETiqa’s insurance at any branches of Maybank? If you want to deal direct with the insurance company, then you may opt to get their term policies available on their website, just key in your details, choose the plan & make the payment, I believe Google will be your best friend. If you wish to get comprehensive policies, you'll have to deal with an agent. Nowadays, you'll be able to buy a policy with the agent without having to meet the agent face to face. This post has been edited by lifebalance: Feb 2 2021, 03:06 PM Pohziliang96 liked this post

|

|

|

Feb 3 2021, 10:05 AM

Return to original view | Post

#11

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(TaiGoh @ Feb 2 2021, 11:32 PM) Thank you so much for your reply, appreciate it! Indeed there is a upgrade made in 2018 to SmartMedic Xtra. I did a check the premium difference between SmartMedic Million and SmartMedic Xtra for age 32 is just RM26 for R&B200. So far I see the only drawback is SmartMedic Million with deductible RM300 I guess? Or maybe something that I did not aware of. Also it does come with regular increment to the R&B just in case R&B getting more expensive in the future. Yes, agreed with all the sifus said here, I forgotten about if reduce deductible in the future will need to undergo another round of underwriting and subject for approval. So definitely will be out for my considerations for now. I am actually curious how the commission works here, I would assume that if I did an upgrade of medical card, the commission for that agent will be restarted correct? And does it matter for consumer point of view? FOR EXAMPLE the medical card premium is 1000 annually, the commission is 30% second year is 25%, I am still paying 1000 annually correct? Will try to compare the plan out there and see whether there is a worth to make a switch, because thinking better do the decision now than later, but if there is no justification to do that, most likely will continue stick with GE. Thanks again.  |

|

|

Feb 3 2021, 01:57 PM

Return to original view | Post

#12

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(adamhzm90 @ Feb 3 2021, 01:54 PM) Anyone can provide quotation for cross hibah? What amount would you like to Hibah?Will need Husband and Wife details as below DOB Gender Smoker or Not Occupation Hibah Amount |

|

|

Feb 3 2021, 03:44 PM

Return to original view | Post

#13

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(KLlang @ Feb 3 2021, 03:33 PM) During pandemic, so far, does insurance company still give guaranteed yearly renewal to standalone medical card holder without underwriting? All medical benefit insurance requires an underwriting unless it's a Guaranteed Issue by the insurance company to you (normally provided you've been with them (the insurance company as a policy holder) for many years with no health issue/claims). Otherwise it's quite impossible.Anyone come across this? However, there are guaranteed renewal medical card out there as well as non-portfolio withdrawal products. Just not "without any underwriting required". This post has been edited by lifebalance: Feb 3 2021, 03:45 PM |

|

|

|

|

|

Feb 3 2021, 04:04 PM

Return to original view | Post

#14

|

|

All Stars

10,162 posts Joined: Nov 2014 |

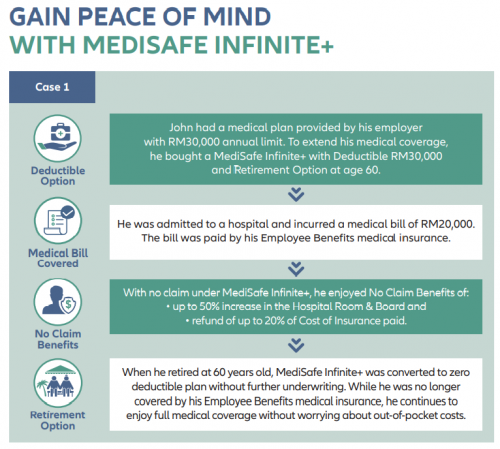

QUOTE(Ewa Wa @ Feb 3 2021, 04:04 PM) This is a plan for those want a high deductible amount, pic said 60yo onwards become non deductible. Can it be earlier for example 50yo? Possible or the option only in 60yo? No, only upon 60 years old |

|

|

Feb 3 2021, 09:19 PM

Return to original view | Post

#15

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(Ryuluvlia @ Feb 3 2021, 08:51 PM) Hi, does anyone know any life insurance plan that will give higher cashback then what we have paid when reach maturity like 70 years old? You mean cash value? that will really depends as the figures upon maturity are non-guaranteed. However some company do offer extra payout upon maturity I'm afraid I can't disclose here, later kena flag hehe |

|

|

Feb 3 2021, 11:44 PM

Return to original view | Post

#16

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(KLlang @ Feb 3 2021, 10:08 PM) Thanks lifebalance. Not to mentioned new sign-up, my concern is long time existing policy holder with same company. Company are expose to higher risk since customer may recovered from COVID but didn't declare to company. It'll subject to the policy that you've bought with the insurance company, if the company provides coverage, then it'll be within their discretion and T&C as not all insurance company covers COVID at the moment.For other health history/ claims, company will receive claim and records from policy holder. But for COVID, customer may recover before yearly renewal and not submit any claim at all since is cover by gov. How agent handle this actually? With regards to future undertaking on COVID recovered patient, they may have new guidelines should there be risk factor involved with recovered patient. |

|

|

Feb 6 2021, 10:15 PM

Return to original view | Post

#17

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(edwin1002 @ Feb 6 2021, 10:04 PM) any covid insurance? All insurance companies and takaful operators under the Life Insurance Association of Malaysia (LIAM) and Malaysian Takaful Association (MTA) have confirmed that they will provide hospitalisation and treatment coverage for COVID-19 – but your policy may differ in terms of specific benefits, terms and conditions.Here are the list of LIAM insurance and takaful operators providing COVID-19 coverage: AIA Bhd Allianz Life Insurance Malaysia Berhad AmMetLife Insurance Berhad AXA AFFIN Life Insurance Berhad Etiqa Life Insurance Berhad Gibraltar BSN Life Berhad Great Eastern Life Assurance (Malaysia) Berhad Hannover Rueck SE, Malaysian Branch Hong Leong Assurance Berhad Malaysian Life Reinsurance Group Berhad Manulife Insurance Berhad MCIS Insurance Berhad Prudential Assurance Malaysia Berhad Sun Life Malaysia Assurance Berhad Tokio Marine Life Insurance Malaysia Bhd. Zurich Life Insurance Malaysia Berhad Benefits such as: (Depends on the company) - Hospitalisation benefit of RM200 per day up to 30 days - Death benefit - Hospitalisation cash relief - One time payoff upon diagnosis |

|

|

Feb 6 2021, 11:19 PM

Return to original view | Post

#18

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(copterbandito @ Feb 6 2021, 10:51 PM) Hi all, wanna ask, my insurance is GE SMARTPROTECT ESSENTIAL INSURANCE 2. Quarterly premium is about RM600. In this insurance my Lion Strategic Fund has about RM8,000. 1. Your policy will enter into a premium holiday mode whereby the policy will continue to deduct the cost of insurance + other fees by the insurance company until your policy has RM0 where it'll lapse. Spoken to my agent that I can choose not to pay the premium as it will deduct from my fund 8K. Is it true it will not affect my coverage and what's the cons if I choose not to pay? Another question is can this GREAT IDEAL LIVING about RM800 yearly payment also can be pay up from my fund 8K? Sorry Covid time am exploring option to keep more cash in hand. If my understanding is right this premium payment from my FUND can last me more than 1 year. Any advice? Thanks 2. Great Ideal Living is a different plan compared to the GE SPE2. Which is a traditional plan, if you choose not to pay, same thing it will not lapse but the policy will enter into a automatic premium loan whereby the insurance company will charge you an interest for the loan, at the end of the period, it'll lapse if the loan interest owed >= your surrender value. If you're not really in need of that cash on hand that urgently, it'll be wise to keep the funds with the insurance company as they'll continue to re-invest your money for you (ILP) and not incur any loan interest (Traditional Plan). If you're feeling the burden to pay for the premium, maybe then it's advisable to go for a premium holiday until you recover your cash flow or maybe choose to reduce your existing benefit so that you can pay lesser premium if that will help you financially. copterbandito liked this post

|

|

|

Feb 7 2021, 03:08 PM

Return to original view | Post

#19

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(jutamind @ Feb 7 2021, 02:33 PM) need feedback on my insurance policies portfolio: 1. You mention your priority is Medical and CI coverage, have you figure out how much you're looking to cover? - there are few methods of finding it out1. AIA Assurance 1 Life insured: 200k, expiring age 100 TPD: 210k, expiring age 60 CI: 150k, expiring age 100 Premium waiver 2. AIA Assurance 2 Life insured: 100k, expiring age 100 TPD: 100k, expiring age 60 CI: 50k, expiring age 100 Medical card: 90k annual, lifetime 300k, room & board 150 expiring age 70 (with co-insurance but cant recall how much already, maybe 10-15k) Premium waiver 3. Allianz PowerLink Life insured: 100k, expiring age 100 TPD: 100k, expiring age 65 Medical card: 120k annual, lifetime 1.2m, room & board 200 expiring age 100 Premium waiver 4. Tokio Marine Medic Plus Medical card: 150k annual, room & board 500 (deductible 10k per disability) Thinking of optimizing both AIA policies but what would be a better option with the newer policies or just maintain them? To me, the more important is medical card and CI coverage. Appreciate views from all. Thanks. 2. Perhaps you can look into consolidating into a single policy if you'd prefer an ease of making claims / managing your policies. I.e a single medical card with high annual limit (nowadays they come min RM1 mil annual limit and above) instead of the current set up which has low annual limit + covering another card's deductible/co-insurance. 3. You can look into upgrading on the existing policy (if it is allowed). Probably get your servicing to quote for you. 4. I can only give a general comment as I don't know you personally. |

|

|

Feb 7 2021, 05:22 PM

Return to original view | Post

#20

|

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(jutamind @ Feb 7 2021, 03:23 PM) You can either cover based on your current annual income or based on the monthly commitment + some extras (to cater for any extra medication / supplements / etc) There are standalone CI as well as ILPs which you can set low death coverage but more to the CI benefit. As far as AIA is concern, nothing much you can do with the old policies unless you choose to buy a newer AIA policy. |

| Change to: |  0.0293sec 0.0293sec

0.75 0.75

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 1st December 2025 - 09:16 PM |

Quote

Quote