Hi bro, rilek dulu bro

The tax rebate and all is cool. Everybody make use of it.

Love the initiative in seeking out the details on your own!

Not only that, there's PRS as well, and now very proud that I started a SSPN account for my son

Here comes the "BUT"

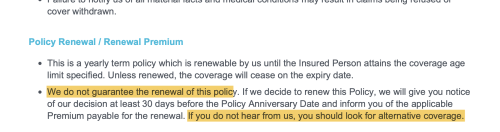

The fund values in your policy are not guaranteed. Those that are guaranteed, are not great.

So no learned person trying to genuinely help you, will tell you to "profit" using these tax benefits.

Unless they cannot convince you, can't confuse you also, then they straight up con you lah.

The tax incentives indeed are cool. I max them out every year.

However, as many here can attest to, the tax rebates do change from time to time.

What are you gna do then? Change your insurance policies as and when the tax incentives change?

That wouldn't be in your best interest to do so.

Might as well just dump the money into the sea. This one no need underwriting.

My point is, there are different angles to look at the tax incentives.

Yes, it is within our interests to make full use of it, you got this part right.

However, an insurance policy will never be an investment vehicle, however much you may want it to be, it is just not.

Regardless of how nice your source of info make it out to sound.

Since I cannot reveal other people's arrangements on my side, I use my own as an example la.

My Life Insurance coverage can previously sustain my household expenses for 20 years (if just put in a savings account and withdraw and use)

My most recent purchase helps sustain my household expenses perpetually in my absence. Cuz I damn near broke once, so very very scared my wife and kid no money.

I do the same with my customers. The intent always takes center stage.

Are there some fund values built-up in my policies? Yes there are.

Do I count on them? No

Why not? Cuz this money has its own purpose, which is to sustain my coverages to my intended time frame.

Then what do you look at? My investments loh, rent need to collect, dividends need to be reinvested, etc. Some money rightfully mine, have to grab la, no choice.

If you're deciding between an insurance commitment and an investment, if I were you, I will take care of my personal insurance first.

Why? Because I am a pretty sensible, risk-averse person.

And on a side note,

@lifebalance is a very experienced planner.

@adele123 is also a very knowledgeable and impartial contributor to this thread.

Maybe through just mere texts, it may have come across different.

I also can't tell you to just "don't take it the wrong way"... Sebab dah terang2 wrong way dah

And of course, subsequent interaction also teruk lah

Obviously it turned into an ego trip, and you found yourself in a spot rather than the answers you were looking for.

What do you think about the outcome? I leave this to you lah k?

This thread is memang good for just about anyone to ask questions. Maybe we keep it that way?

For everybody's benefit also la

And if you find some contributors in the industry that you feel comfortable dealing with, engage them in your own capacity loh.

When you converting to Licensed Financial Planner bro.

Oct 21 2022, 12:08 PM

Oct 21 2022, 12:08 PM

Quote

Quote

0.0651sec

0.0651sec

0.27

0.27

7 queries

7 queries

GZIP Disabled

GZIP Disabled