This is my premium hike from PRU, which an ILP based medical/life plan, it does not say that my investment is doing poorly but instead blame the increase of medical cost as the reason for the hike.

And since I am already here, should I take up the option to reduce the hike?

LETTER FROM PRU

Dear Sir/Madam,

Policy Number :

Life Assured :

Assured :

Subject : PRUValue Med New Insurance Charges and Premium

Thank you for choosing PRUValue Med as your health and medical

protection solution.

Healthcare costs have been consistently rising with increased

demand for healthcare services, and better medical treatment

with advancement in technology. As such, we continuously strive

to reduce the impact of medical inflation by working closely with

our healthcare providers to maintain high-quality care and

preferred rates.

Yet, the average medical inflation for PRUValue Med for the past 3

years is still rising at 14.30% per year. 65 out of 1,000 policy

owners made a claim compared to 67 out of 1,000 policy owners

3 years ago. Each claim on average has increased from RM

9,120.00 to RM 14,233.00.

As your long-term medical protection is important, we regularly

review our medical plans to ensure you are protected when you

need it. Having carefully considered the rise in healthcare costs,

we will be revising the insurance charges of your medical plan

effective 01-01-2024*.

With this revision of the insurance charges, your premium will be

revised as below:

Current Premium

RM 463.00

Monthly

New Premium**

RM 546.00

Effective Date 01-01-2024

Monthly

Note: The increase in premiums is to cater for the increase in medical insurance

charges. Payor coverage (if applicable) will increase correspondingly, and

additional insurance charges will be deducted from your policy account value. We

advise you to refer to your annual statement and discuss with your Prudential

Wealth Planner or Bank Representative to review your policy’s sustainability

regularly to ensure continuity of your coverage.

Option to Convert

For lower insurance charges, you have an option to change your current medical plan to include a higher Med Saver Plan. This means you will need to pay the selected Med Saver amount to the hospital before your insurance plan starts to pay out any eligible claim. If you opt for the higher Med Saver Plan, your current Room & Board (R&B) Plan will also be revised from R&B RM100 Plan to R&B RM150 Plan.

Below is the new premium comparison of your current plan based on PRUValue Med Plan RM300 Med Saver with R&B RM100 Plan.

Your current plan

RM300 Med

Saver with R&B RM100 Plan

RM 546.00 Monthly

Optional plan

RM1000 Med

Saver with R&B RM150 Plan

RM 505.00 Monthly

To opt for the higher Med

Saver with R&B RM150 Plan,

please complete and return to

us the enclosed "Option to

Convert" form by 31-12-2023.

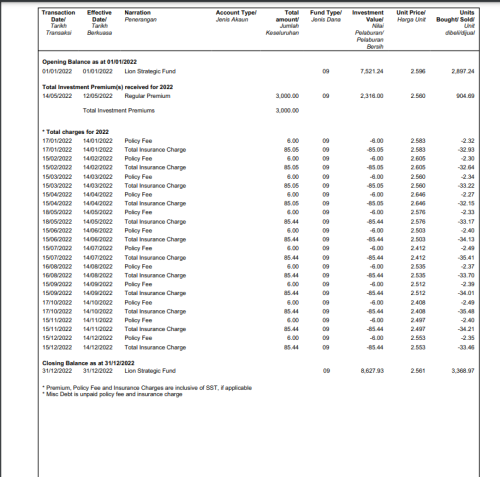

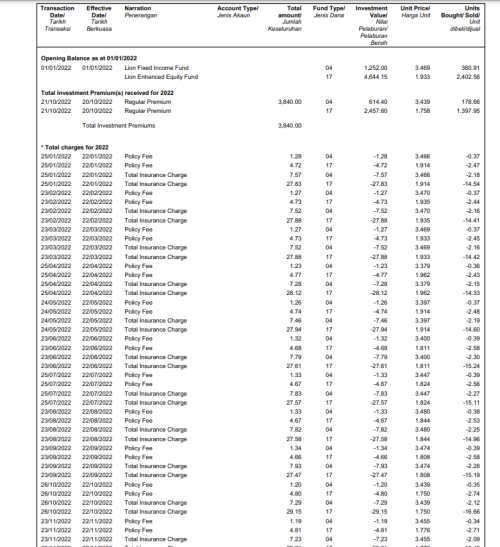

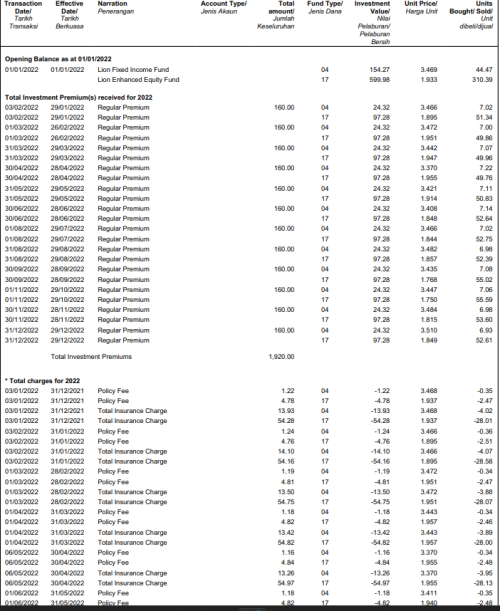

A medical repricing and underperformance of the fund can happen either independently or at the same time.

The letter you received seems to be talking about the medical repricing.

Your insurer will inform you on the sustainability of the plan due to the fund performance on a yearly basis via a different letter.

Sep 8 2023, 10:18 AM

Sep 8 2023, 10:18 AM

Quote

Quote

0.0406sec

0.0406sec

0.46

0.46

7 queries

7 queries

GZIP Disabled

GZIP Disabled