Jul 29 2020, 12:19 PM

Jul 29 2020, 12:19 PM

QUOTE(lovingforyou @ Jul 29 2020, 07:58 AM)

Yes, i notice the guarantee cash payout. I believe they describe the guarantee cash payout 15% - 20% in this way:-

First year invest 50k, you get 15% "bonus" = 7.5k

2nd to 5th year invest 50k, get 15% "bonus" as well as 7.5k per year

Then 6th year to 13rd year, no need to do investment anymore and they are giving 20% bonus which is 10k

And i done a simple calculation, total contribution had been made is RM250,000

The bonus total for 13 years is (7500 x 5) + (10,000 x 8) = 117,500

Wtf this kind of policy existing in this world

Nvm i ask my another insurance agent to help me to take a look on the policy

Btw sifu sekalian, how do i send my policy for you guys here?

There should be a maturity benefit at the end of the coverage which is after 13 years. The maturity benefit should be ranging around another 130k to 150k ++. Which makes the total = RM117,500 (bonus total) + maturity benefit = Not less than RM250,000 premium paid.First year invest 50k, you get 15% "bonus" = 7.5k

2nd to 5th year invest 50k, get 15% "bonus" as well as 7.5k per year

Then 6th year to 13rd year, no need to do investment anymore and they are giving 20% bonus which is 10k

And i done a simple calculation, total contribution had been made is RM250,000

The bonus total for 13 years is (7500 x 5) + (10,000 x 8) = 117,500

Wtf this kind of policy existing in this world

Nvm i ask my another insurance agent to help me to take a look on the policy

Btw sifu sekalian, how do i send my policy for you guys here?

In savings plan, insurance company will guarantee to return all your premiums paid 100% at the end of maturity if I am not mistaken. Any extra return will depend on the fund performance. Generally, savings plan should not be used as a high return investment tool.

Like previous sifu said, savings plan will have a surrender penalty if you terminate the policy before the maturity date and you will definitely lose money before maturity.

If you want to share the policy here, you can just take the picture of the schedule and upload as image here.

This post has been edited by GE-DavidK: Jul 29 2020, 12:38 PM

Quote

Quote

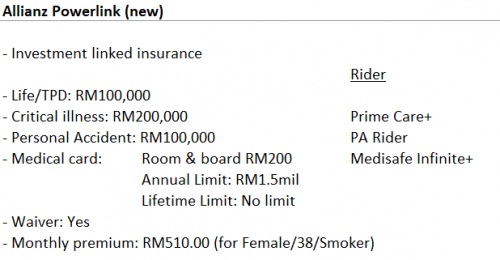

He did quote me a similar package for GE to match the coverage by Allianz but the monthly premium is higher at RM575 and I need to top up / pay extra since I wanted early payout for critical care, whereas Allianz already have payout at all stages.

He did quote me a similar package for GE to match the coverage by Allianz but the monthly premium is higher at RM575 and I need to top up / pay extra since I wanted early payout for critical care, whereas Allianz already have payout at all stages. 0.1360sec

0.1360sec

0.46

0.46

7 queries

7 queries

GZIP Disabled

GZIP Disabled