QUOTE(heavensea @ Mar 4 2020, 03:14 PM)

Old loan tak kasi potong?

Some banks practice with same installment amount but higher principal reduction on each installment. U need to monitor the monthly transaction to see tat.BNM Cut Rate Again But Not Benefit For New Loan, BNM Cut Rate Again But Not Benefit For N

|

|

Mar 4 2020, 07:50 PM Mar 4 2020, 07:50 PM

Show posts by this member only | IPv6 | Post

#21

|

All Stars

13,756 posts Joined: Jun 2011 |

QUOTE(heavensea @ Mar 4 2020, 03:14 PM) Old loan tak kasi potong? Some banks practice with same installment amount but higher principal reduction on each installment. U need to monitor the monthly transaction to see tat. |

|

|

|

|

|

Mar 4 2020, 08:09 PM

Show posts by this member only | IPv6 | Post

#22

|

|

Junior Member

461 posts Joined: May 2015 |

If the respective bank not reduce your instalment, actual is indirectly assist you to reduce more principal amount

Did you know how much you need to pay for interest cost each month again your monthly intalment !!! If your loan tenure is 35 years, at the starting point, interest cost already cover by 78% of your instalment amount, which mean only 22% can reduce your principal amount Of course interest cost will gradually decelerated & principal amount cover will be accelerated but need longer period of time In calculation based on my above scenario, if your instalment is RM 2061 then interest cost already RM 1607 per month, only left RM 454 amount to reduce your principal So you think if I take the loan right now, unfortunately 3 years down the road, BNM going to normalise the OPR, what happen to my instalment !!! What happen for my monthly interest cost !!! **Wisely investment or purchase is right now priority  |

|

|

Mar 4 2020, 08:55 PM

|

Senior Member

9,616 posts Joined: Dec 2013 |

QUOTE(ManutdGiggs @ Mar 4 2020, 07:50 PM) Some banks practice with same installment amount but higher principal reduction on each installment. U need to monitor the monthly transaction to see tat. Pbe potong trus for last reduction, this time dunno yet. |

|

|

Mar 4 2020, 11:30 PM

Show posts by this member only | IPv6 | Post

#24

|

|

Junior Member

461 posts Joined: May 2015 |

I have been watching some members here still misleading for those people intend to apply the home loan

Please reconfirm respectively bank officer who assist your home loan application You need wisely to ask what is the different right now (after Jan'20 & Mar'20 2 times OPR cut) compare with before rate cut |

|

|

Mar 5 2020, 12:21 AM

|

Junior Member

205 posts Joined: Nov 2012 |

QUOTE(DisneyHome @ Mar 4 2020, 07:34 PM) Too sad to say confirm no interest rate change for new home loan application despite OPR cut whereby announced by BNM yesterday (I have called my some bank officers to reconfirm) Really? So bank follows the OPR cut by reducing BR, but increase the interest rate to maintain back the mortgage interest? That's mean, if interest rate offered before was BR + 0.75% = 4.25% (before base rate cut was 3.50%), now become BR + 1.00% = 4.25% (after base rate cut to 3.25%) Bear in mind, during Jan'20 BNM had announced OPR cut simultaneously BR also follow the suit but same practice for majority bank (ie no change of interest rate offer for new home loan by that time) A few post back you also mentioned, when BNM announce OPR increase, our mortgage loan will hike more than expected example from 4.25 (BR 3.25 + Interest 1) to 5% (BR 4 + 1)?? Lol. Bank win liao lo |

|

|

Mar 5 2020, 12:50 AM

|

|

Junior Member

980 posts Joined: Mar 2019 |

When year 2009

OPR is 2% Still got space to cut rate |

|

|

|

|

|

Mar 5 2020, 07:28 AM

Show posts by this member only | IPv6 | Post

#27

|

|

Junior Member

461 posts Joined: May 2015 |

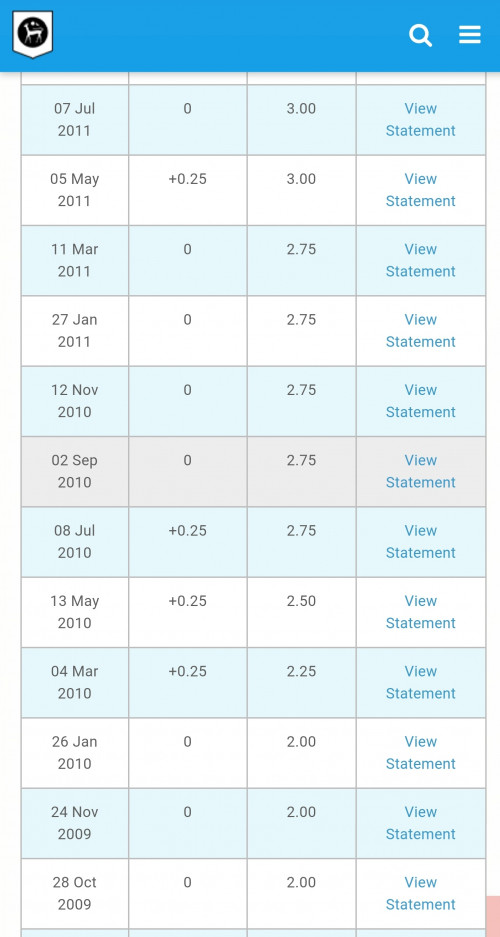

https://www.bnm.gov.my/index.php?ch=mone&pg=mone_opr_stmt If you look at above OPR decision, BNM even though aggressively cut rate to 2.00% during 2009 but very fast to normalise back to 3.00% in year 2011 Based on current offered by respective banks, even though 2 times OPR cut (BR also follow suit) but unfortunately spread rate increased back to normal the effective rate for new home loan applications As I mentioned earlier, If I want to take up new home loan right now, quite high risk for the coming next few years once BNM normalise the OPR again For those taken home loan before 2020, I can say congratulation to you all  For those intend to take new home loan, I can say wisely to calculate your monthly budget future & risk factor how far you can undertake  |

|

|

Mar 5 2020, 07:31 AM

Show posts by this member only | IPv6 | Post

#28

|

|

Junior Member

461 posts Joined: May 2015 |

Always remember "Historical Data" don't lie you

Only Human always can lie you  |

|

|

Mar 5 2020, 07:42 AM

Show posts by this member only | IPv6 | Post

#29

|

|

Junior Member

461 posts Joined: May 2015 |

The for funny things is if I purchase new property, at least need to wait 3 years for completion & vacant possession

During construction period, I only serving interest charged by progressively completion of each stage Even though, might be, this 2 or 3 years I can willing bear the risk of interest cost by 4.25% (subject to no changes on this 3 years) because still serving interest cost from small ticket of interest charged to gradually increase until VP Unfortunately after I got my home key, going to start instalment, BNM going to start normalising OPR, so my instalment also gradually increased & monthly interest charged also increased Don't forget right now supply more than demand market situation, if I want to rent out to cover my cost, rental market become more & more competitive  |

|

|

Mar 5 2020, 08:05 AM

|

|

Junior Member

164 posts Joined: Jan 2020 |

QUOTE(DisneyHome @ Mar 5 2020, 07:42 AM) The for funny things is if I purchase new property, at least need to wait 3 years for completion & vacant possession Yes, Long road to go, so I don't think OPR is really matter for new project buyer like us, since all loan now is more on semi flexi, no point to care so much on this OPR, just pay the progressive interest and instalment, that it. hahahahaDuring construction period, I only serving interest charged by progressively completion of each stage Even though, might be, this 2 or 3 years I can willing bear the risk of interest cost by 4.25% (subject to no changes on this 3 years) because still serving interest cost from small ticket of interest charged to gradually increase until VP Unfortunately after I got my home key, going to start instalment, BNM going to start normalising OPR, so my instalment also gradually increased & monthly interest charged also increased Don't forget right now supply more than demand market situation, if I want to rent out to cover my cost, rental market become more & more competitive |

|

|

Mar 5 2020, 11:04 AM

|

Junior Member

180 posts Joined: Jan 2003 |

QUOTE(DisneyHome @ Mar 5 2020, 07:42 AM) The for funny things is if I purchase new property, at least need to wait 3 years for completion & vacant possession if you still getting 4.25% interest today... then you better go do some homework and get a better deal so you won't get a that bad of a hit compare to those who got it before the 0.5% drop. Be a smart consumer and not get shortchange by the OPR drop.During construction period, I only serving interest charged by progressively completion of each stage Even though, might be, this 2 or 3 years I can willing bear the risk of interest cost by 4.25% (subject to no changes on this 3 years) because still serving interest cost from small ticket of interest charged to gradually increase until VP Unfortunately after I got my home key, going to start instalment, BNM going to start normalising OPR, so my instalment also gradually increased & monthly interest charged also increased Don't forget right now supply more than demand market situation, if I want to rent out to cover my cost, rental market become more & more competitive |

|

|

Mar 5 2020, 11:23 AM

|

|

Junior Member

897 posts Joined: May 2019 |

If BR drop, but the particular bank increase the + rate, to normalise the drop in BR, then this bank easily lose a lot of business to other competitor.

When OPR drops, no matter how, borrower generally see reduction in the interest payment across, just degree more and less compared to OPR. If one still stuck with higher loan interest despite OPR reduction, better review your loan or you may have made a poor decision to take up such a loan, like fixed rate loan or the bank is giving poor competitive rate. |

|

|

Mar 7 2020, 07:58 AM

Show posts by this member only | IPv6 | Post

#33

|

|

All Stars

13,756 posts Joined: Jun 2011 |

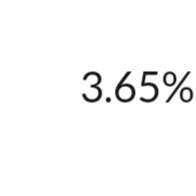

The normal loan rate now should b 3.65% for existing loan

New loan for gd payor stil around tis rate |

|

|

|

|

|

Mar 7 2020, 08:13 AM

|

All Stars

21,456 posts Joined: Jul 2012 |

QUOTE(ManutdGiggs @ Mar 7 2020, 07:58 AM) The normal loan rate now should b 3.65% for existing loan Some claimed current economy slowed down could be worse than 1997 AFC.New loan for gd payor stil around tis rate This post has been edited by icemanfx: Mar 7 2020, 08:13 AM |

|

|

Mar 7 2020, 09:01 AM

Show posts by this member only | IPv6 | Post

#35

|

Junior Member

728 posts Joined: Jun 2012 |

Thanks TS for sharing his comment. There is good good or bad interm of lower down the interest rate.

In my point of view, you can buy subsales property now instead of buying under construction project. Because subsales is full disbursement. So you can enjoy lower interest rate now. Also, if you do refinance now, u can enjoy lower interest rate to use ur money to settle high interest rate debt such as credit card or personal loan. |

|

|

Mar 7 2020, 09:10 AM

Show posts by this member only | IPv6 | Post

#36

|

|

All Stars

13,756 posts Joined: Jun 2011 |

QUOTE(icemanfx @ Mar 7 2020, 08:13 AM) Some claimed current economy slowed down could be worse than 1997 AFC. Some mentioned tis b4 last round. Dementia??? |

|

|

Mar 7 2020, 09:52 AM

Show posts by this member only | IPv6 | Post

#37

|

|

Junior Member

461 posts Joined: May 2015 |

QUOTE(Pac Lease @ Mar 7 2020, 09:01 AM) Thanks TS for sharing his comment. There is good good or bad interm of lower down the interest rate. Now the main issue is not easy to do refinancingIn my point of view, you can buy subsales property now instead of buying under construction project. Because subsales is full disbursement. So you can enjoy lower interest rate now. Also, if you do refinance now, u can enjoy lower interest rate to use ur money to settle high interest rate debt such as credit card or personal loan. Unless you are low gearing & personal profile sufficient strong Unfortunately a lot ppl holding few units property also hardly to refinance When market not stable, banks definitely very cautious to review all credit facilities Recently some majority banks already tightened lending policies, no matter refinancing or new property purchase |

|

|

Mar 7 2020, 10:27 AM

Show posts by this member only | IPv6 | Post

#38

|

|

Senior Member

3,165 posts Joined: Feb 2015 |

QUOTE(DisneyHome @ Mar 4 2020, 07:34 PM) Too sad to say confirm no interest rate change for new home loan application despite OPR cut whereby announced by BNM yesterday (I have called my some bank officers to reconfirm) You can’t blame the banks.. when rate is cut, banks source of funds (fixed deposit rates) are still locked at higher rates... banks can’t offer lower rates as yet... it will take some time before they attract new FD at lower rates, then they can lower the spreads in the future... banks not in charity.. if u tak suka.. then don’t take the loan .. this is just realityThat's mean, if interest rate offered before was BR + 0.75% = 4.25% (before base rate cut was 3.50%), now become BR + 1.00% = 4.25% (after base rate cut to 3.25%) Bear in mind, during Jan'20 BNM had announced OPR cut simultaneously BR also follow the suit but same practice for majority bank (ie no change of interest rate offer for new home loan by that time) |

|

|

Mar 7 2020, 10:38 AM

Show posts by this member only | IPv6 | Post

#39

|

Junior Member

458 posts Joined: Mar 2010 |

QUOTE(ManutdGiggs @ Mar 7 2020, 07:58 AM) The normal loan rate now should b 3.65% for existing loan Really? Which bank is offering this, assuming i have good track recordNew loan for gd payor stil around tis rate |

|

|

Mar 7 2020, 10:43 AM

|

|

All Stars

13,756 posts Joined: Jun 2011 |

QUOTE(Nama saya Amad @ Mar 7 2020, 10:38 AM) Really? Which bank is offering this, assuming i have good track record Few banks. Try 1 by 1. 😉 |

| Change to: |  0.0239sec 0.0239sec

0.82 0.82

6 queries 6 queries

GZIP Disabled GZIP Disabled

Time is now: 1st December 2025 - 05:38 PM |

Quote

Quote