Outline ·

[ Standard ] ·

Linear+

Investment StashAway Malaysia, Multi-Region ETF at your fingertips!

|

CaptainGrindy P

|

Jan 20 2021, 10:55 AM Jan 20 2021, 10:55 AM

|

New Member

|

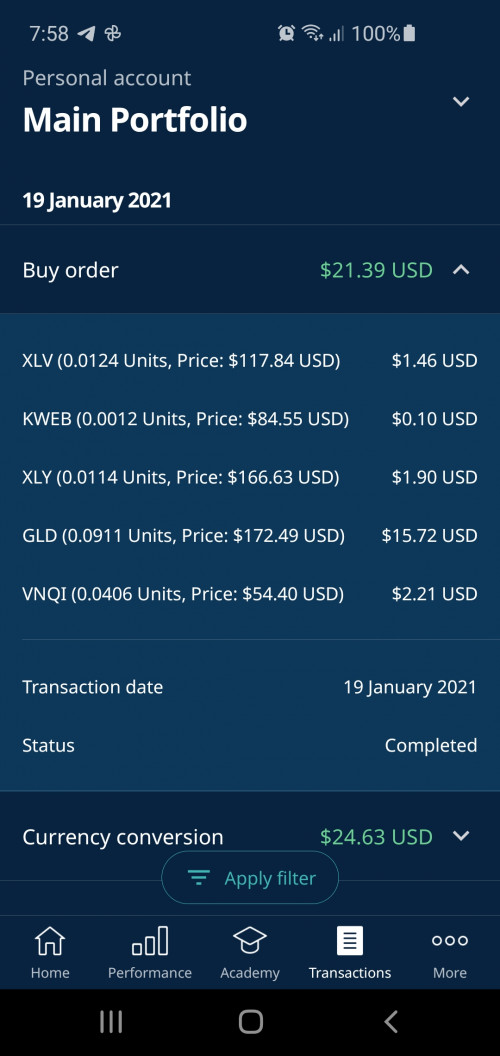

QUOTE(tbgreen @ Jan 19 2021, 11:35 PM) I don't know what went wrong or it is normal: SAMY keep buying GLD for me, in both my risk 36% & 22%. My GLD weigtage now is 16.47% for R36% and 19.66% for R22%. But SAMY keep buying GLD in my current weekly DCA... Is Gold cheap now? Or SAMY see what we cannot see: the Gold price will sky rocket soon? Perhaps my understanding of GLD in this etf is totally wrong..... Puzzle puzzle puzzle to make up to the TARGET weightage of 20%, thats it |

|

|

|

|

|

CaptainGrindy P

|

Jan 25 2021, 11:17 PM

|

New Member

|

omg, kweb is on fire, again... how am i suppose to top up again with the price keep rallying. scare the hell out of me

|

|

|

|

|

|

CaptainGrindy P

|

Jan 26 2021, 01:31 AM

|

New Member

|

QUOTE(lee82gx @ Jan 26 2021, 12:04 AM) Um, if u enter now, almost none of it would be kweb by way of active rebalancing. sry, was trying to say all etf in my portfolio keep rising and is at all time high, especially KWEB. IJR also. this month alone, portfolio gain 4-5%. |

|

|

|

|

|

CaptainGrindy P

|

Jan 26 2021, 01:43 AM

|

New Member

|

i was thinking of one kind of method of depositing:

Amount deposit = regular amount - changes in the value of previous month

For example: assume regular amount is RM1000. If in December your portfolio gain profit by RM600, then the "amount deposit" = RM400 (1000-600). If conversely, this month your portfolio loses RM200, then the "amount deposit" = RM1200 (1000-(-200)). What do u all think?

|

|

|

|

|

|

CaptainGrindy P

|

Jan 26 2021, 12:43 PM

|

New Member

|

QUOTE(lee82gx @ Jan 26 2021, 08:09 AM) So why worry about the small amount buying ath, suffering correction but not worry about your big pool also suffering the correction? If thats the case why not sell the whole portfolio now? Thats because you believe deep down it will rise, eventually. So if indeed that is true, why not keep investing / invested? BTW I am only sharing my useless 2c. Don't listen to it.  I get u. im thinking about the entry point |

|

|

|

|

|

CaptainGrindy P

|

Jan 26 2021, 02:22 PM

|

New Member

|

QUOTE(sohailili @ Jan 26 2021, 01:40 PM) The best time to plant a tree was 20 years ago. The second best time is now. bravo, good good  |

|

|

|

|

|

CaptainGrindy P

|

Mar 16 2021, 08:29 PM

|

New Member

|

QUOTE(xander83 @ Mar 16 2021, 08:16 PM) ETFs picks are done manually by SA committee After that the rest are fully robo with algorithm including optimisation The only change would be manually when they swapped or change or enter new ETFs into inclusion as they need to create a new algorithm for this purposes ETFs are selected using ERAA or manually by SA committee? |

|

|

|

|

|

CaptainGrindy P

|

Mar 17 2021, 10:43 AM

|

New Member

|

QUOTE(yklooi @ Mar 17 2021, 10:38 AM) just a simulated scenario for comparing from https://moneysmart.gov.au/managed-funds-and...-fee-calculator0.7% annual mgmt fees with SA VS 0% annual mgmt fees with DIY  will DIY results be same as SA 10 yrs? even a 1%pa less than SA will be noticeable too after 10 yrs if diy using SA allocation, should get investment earning between 11.20 and 12%? |

|

|

|

|

|

CaptainGrindy P

|

Mar 17 2021, 10:51 AM

|

New Member

|

QUOTE(cucumber @ Mar 17 2021, 10:46 AM) One small thing to note, for DCA, if we want to mimic SAMY buying different ETFs with only RM1k, then we'll need the original IBKR account which allows 'fractional shares'. That has a monthly fee of $10USD. So annual fees will be more like RM500. If u can deposit 4k and above per month, then diy is viable? 4k because 1 share of GLD is USD 162, it is 20% of portfolio, so to buy 1 share, total amount = 162 x 100/20 x 4.1 (usd/myr) = RM3240 roughly |

|

|

|

|

|

CaptainGrindy P

|

Mar 17 2021, 10:53 AM

|

New Member

|

QUOTE(yklooi @ Mar 17 2021, 10:47 AM) simulated for comparing purposes... fyi, 2020 SA returns https://www.stashaway.my/r/our-returns-2020disclaimer:  Investment involves risk. The price of securities may go down as well as up, and under certain circumstances an investor may sustain a total or substantial loss of investment. Past performance is not necessarily indicative of the future or likely performance of the fund. Investors should read the relevant fund's prospectus for details before making any investment decision. An Investor should make an appraisal of the risks involved in investing in these products and should consult their own independent and professional advisors, to ensure that any decision made is suitable with regards to their circumstances and financial position. sorry but does this answer my question? |

|

|

|

|

|

CaptainGrindy P

|

May 9 2023, 12:53 PM

|

New Member

|

Dear any math sifu,

MWR - if let say is MWR 3%

Does it means if i have been putting the same amount into FD at the same time throughout the period in a FD, it will equates to a FD rate of 3%?

|

|

|

|

|

|

CaptainGrindy P

|

May 10 2023, 09:13 AM

|

New Member

|

If

i put fd 1k/year for 9years (term: 12months) reinvest interest. The rate is 3%per annum.

I put SA 1k/year for 9years

On 10th year (last fd matured ady), if SA MWR is 3%. Will both SA and FD have the same amount?

|

|

|

|

|

|

CaptainGrindy P

|

May 10 2023, 02:38 PM

|

New Member

|

QUOTE(Medufsaid @ May 10 2023, 12:55 PM) you cannot predict SA performance. it carries risks. if predictable returns is what you want you can just deposit into FD i am not predicting SA return. i am benchmarking SA return with FD. my current MWR is +3.45%. im asking what this MWR means, if it means 3.45% does it mean if i have been putting the same amount at the same time to FD, assuming all fd has matured at the time of comparison, will it also give the same amount as SA today. meaning i want to find the practical use of this MWR. |

|

|

|

|

Quote

Quote 0.1570sec

0.1570sec

0.36

0.36

7 queries

7 queries

GZIP Disabled

GZIP Disabled