QUOTE(kenloh7 @ Feb 20 2019, 01:40 PM)

Hi guys, I'm new to ASNB here. Would like to know the differences of ASM to FD.

Are the below true? Can you also add on to the pros/cons that you can think of?

Pros:

1. Higher interest rate at 6%+ vs 4%+ by FD

2. Can withdraw at anytime vs withdraw after maturity (3m/6m/12m) for FD

3. Any month is the always best time to deposit, unlike FD promotion which happens infrequently

Cons:

1. Not insured by PIDM

2. Need to fight for limited units (for non-bumi)

Also 1 question, I just created the account this month and currently have about RM2k after progressively topping up. Will I be entitled for RM2k dividend's calculation for this month, or zero since I start off with RM0 as the lowest balance?

Your question is answered when u scroll up.

To save your time, let me correct it.

1. Higher interest rate, but not necessarily 6%. As mentioned by sifus and unkers, this year probably 5.X%. It really depends on how Zeti play our money.

2. Yes you can withdraw anytime, but you only get dividend (aka Interest

) after end of financial year. Any it is prorated by month, calculated by

minimum balance.

3. Yes. To be exact, if you can deposit on 1st of the month, amount considered for dividend will includes the money you deposited. (Note: I can't prove this, see if any unker can back this up).

4. Yes, we have discussion about how PIDM insure the FD. Due to vast amount of money involved, I doubt it can really compensate the money you lost when something happened to FD.

5. If you're indian, you no need to fight amount for ASM3 as there are already 30K quota for you.

For this month, you got a big fat zero.

Unless if you topped up on 1st Feb.

QUOTE(swn525 @ Feb 20 2019, 01:50 PM)

sorry, i try search "death", get some info, but can't find the prons & cons, did i search wrong wording?

http://www.asnb.com.my/v3_/pdf/perkhidmata...risan/PA_en.pdflook like pengisytiharan amanah is more faster, take 21 days

if my calculation correct

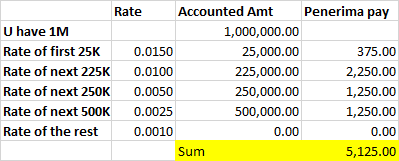

base on the claim table, first 500k will deduct (375 + 2250 + 1250 + 1250 =

RM 5125), next 500k is 0.1% which is

RM 5001 mil - 5125 - 500 =

RM 994,375I thought the last 500K is 0.25%? See the PDF I attached above.

This post has been edited by xeon1989: Feb 20 2019, 01:56 PM

Jan 18 2019, 03:23 PM

Jan 18 2019, 03:23 PM

Quote

Quote

0.1648sec

0.1648sec

0.28

0.28

7 queries

7 queries

GZIP Disabled

GZIP Disabled