Would you, or are you spending more than 60% of your net income for home loan, and why?

How much would your ideal % of income be tucked away for home loan?

Would you spend over 60% of your income?, For home loan

|

|

Apr 12 2017, 08:22 PM, updated 9y ago Apr 12 2017, 08:22 PM, updated 9y ago

Show posts by this member only | Post

#1

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

As per title, just for the purpose of discussion.

Would you, or are you spending more than 60% of your net income for home loan, and why? How much would your ideal % of income be tucked away for home loan? |

|

|

|

|

|

Apr 12 2017, 08:26 PM

Show posts by this member only | Post

#2

|

Senior Member

1,765 posts Joined: Jul 2010 |

Anything above 50% of nett income just for loan repayments, for me that's living close to the edge already.

|

|

|

Apr 12 2017, 08:38 PM

Show posts by this member only | Post

#3

|

Senior Member

9,616 posts Joined: Dec 2013 |

60% for home loan only, no.

|

|

|

Apr 12 2017, 08:43 PM

Show posts by this member only | Post

#4

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(8sg9ft @ Apr 12 2017, 08:26 PM) Anything above 50% of nett income just for loan repayments, for me that's living close to the edge already.  QUOTE(heavensea @ Apr 12 2017, 08:38 PM) 60% for home loan only, no. But for starters, generally the millenials are having tough time, tend to fall into the 60+% bracket.Salary will go up in time, maybe suffer for 2 years, then as salary goes up, things will be better? This post has been edited by Michaelbyz23: Apr 12 2017, 08:52 PM |

|

|

Apr 12 2017, 08:44 PM

Show posts by this member only | Post

#5

|

|

Senior Member

1,780 posts Joined: Nov 2010 |

firstly, your question is wrong and not making any sense, please this close this thread and google DSR....

|

|

|

Apr 12 2017, 08:50 PM

Show posts by this member only | Post

#6

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(Nikmon @ Apr 12 2017, 08:44 PM) firstly, your question is wrong and not making any sense, please this close this thread and google DSR.... Mind further your explanation? My question was simple and simply for discussion purpose, on whether will you be willing to spend 60% of net income for home loan. Do I need to close my topic as per ordered by you, simply because I posted a discussion thread? Please advise me, sifu  If it's wrong, or offensive, I apologize, you are free to hit the report button as well. |

|

|

|

|

|

Apr 12 2017, 09:00 PM

Show posts by this member only | Post

#7

|

Senior Member

2,812 posts Joined: Dec 2011 |

worth if salary above 10k

|

|

|

Apr 12 2017, 09:02 PM

Show posts by this member only | IPv6 | Post

#8

|

|

Senior Member

1,359 posts Joined: Aug 2013 |

Mine 80% got for loan repayment 😂

|

|

|

Apr 12 2017, 09:06 PM

Show posts by this member only | Post

#9

|

|

Senior Member

2,812 posts Joined: Dec 2011 |

QUOTE(Kicimiao66cc @ Apr 12 2017, 09:02 PM) Mine 80% got for loan repayment 😂 me toooo   |

|

|

Apr 12 2017, 09:10 PM

|

|

Senior Member

7,343 posts Joined: May 2005 |

QUOTE(Kicimiao66cc @ Apr 12 2017, 09:02 PM) Mine 80% got for loan repayment 😂 20% enough for other expenses? |

|

|

Apr 12 2017, 09:18 PM

|

|

Senior Member

1,780 posts Joined: Nov 2010 |

QUOTE(Michaelbyz23 @ Apr 12 2017, 08:50 PM) Mind further your explanation? My question was simple and simply for discussion purpose, on whether will you be willing to spend 60% of net income for home loan. Do I need to close my topic as per ordered by you, simply because I posted a discussion thread? if you want to gauge how many rich and poor pp in this forum, than your poll's question is make sense.Please advise me, sifu If it's wrong, or offensive, I apologize, you are free to hit the report button as well. 60% is affordable for high income but not low income. This post has been edited by Nikmon: Apr 12 2017, 09:24 PM |

|

|

Apr 12 2017, 09:21 PM

Show posts by this member only | IPv6 | Post

#12

|

|

Senior Member

1,359 posts Joined: Aug 2013 |

QUOTE(selinix @ Apr 12 2017, 09:10 PM) 20% enough for other expenses? Enof lo |

|

|

Apr 12 2017, 09:22 PM

|

|

Junior Member

319 posts Joined: Nov 2012 |

i believe in work hard now relax later.. first few year is abit harder but at least at later age we can relax more.. if we dint give a go now with high commitments, then few years later our life will be more difficult..

|

|

|

|

|

|

Apr 12 2017, 09:28 PM

|

Junior Member

336 posts Joined: Mar 2017 |

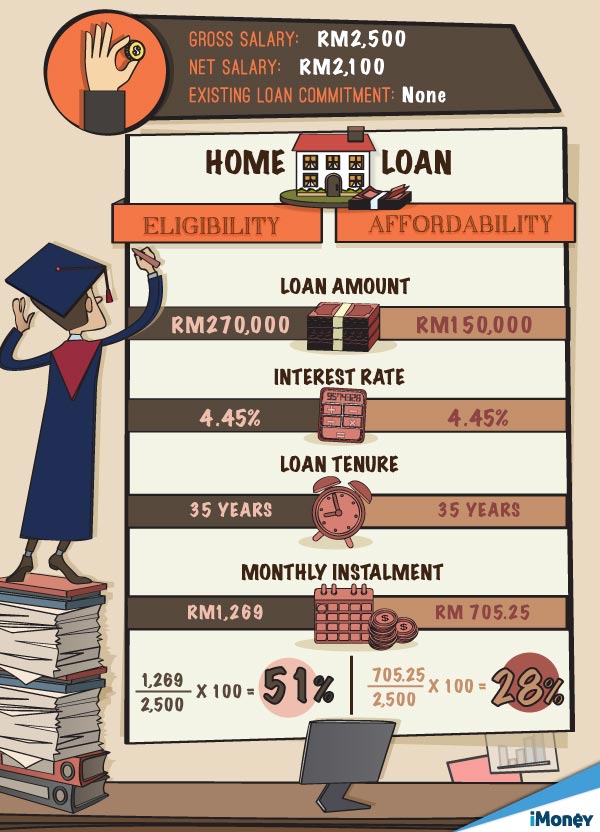

Doubt the bank would approve the loan 270k wit juz 2.1k nett income nowadays

|

|

|

Apr 12 2017, 09:28 PM

|

|

Senior Member

3,838 posts Joined: Sep 2013 |

QUOTE(Nikmon @ Apr 12 2017, 09:18 PM) if you want to gauge how many rich and poor pp in this forum, than your poll's question is make sense. correct. 60% for person with 1.8k salary is madness. prob wont hv enough to eat. 60% of 20k on the other hand is still comfortable.60% is affordable for high income but not low income. |

|

|

Apr 12 2017, 09:28 PM

|

|

Junior Member

115 posts Joined: Mar 2017 |

This is a very subjective question, if your annual income is like Lim Kok Thay, then you can well afford to spend more than 60% of your income on a home loan, as the balance income (after minus the home loan) is still tens of millions, and a small fraction of this is sufficient for you to sustain your living expenses.

On the other hand, if you income is 2k a month, if you pay 60% for home loan, the balance income is hardly sufficient to sustain a living. In any event, please note that Bank Negara only allows around 30%-40% of one's income for payment of home loan, so even if you wish to use 60% of your income to pay your home loan, no bank will agree to this. |

|

|

Apr 12 2017, 09:38 PM

Show posts by this member only | IPv6 | Post

#17

|

|

Senior Member

1,416 posts Joined: Feb 2015 |

QUOTE(Nikmon @ Apr 12 2017, 08:18 PM) if you want to gauge how many rich and poor pp in this forum, than your poll's question is make sense. +160% is affordable for high income but not low income. |

|

|

Apr 12 2017, 09:39 PM

|

|

Senior Member

9,616 posts Joined: Dec 2013 |

QUOTE(Michaelbyz23 @ Apr 12 2017, 08:43 PM) But for starters, generally the millenials are having tough time, tend to fall into the 60+% bracket. imno,Salary will go up in time, maybe suffer for 2 years, then as salary goes up, things will be better? everyone have to anticipate adverse future such as retrenchment, losing ability to work (touch wood) and etc. don't say 60%, 50% also considered risky as putting own-self in the edge of cliff already; especially in current malai bole land economy/market which is bleak like Death Metal music. |

|

|

Apr 12 2017, 09:41 PM

Show posts by this member only | IPv6 | Post

#19

|

|

Senior Member

1,416 posts Joined: Feb 2015 |

What if monthly income RM3000 but have FD 500k and use the interest to pay housing loan?

|

|

|

Apr 12 2017, 09:48 PM

|

Senior Member

2,396 posts Joined: Aug 2016 |

QUOTE(Tankimher @ Apr 12 2017, 09:46 PM) Don't talk cock laaaaa monthly income 3k FD 500k zzzz FAMA fund leh 😂 |

|

|

Apr 12 2017, 09:51 PM

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(Kicimiao66cc @ Apr 12 2017, 09:02 PM) Mine 80% got for loan repayment 😂 Haha, you must be earning 20k to qualify for that! QUOTE(FuNks @ Apr 12 2017, 09:06 PM) me toooo Another top earner! Haha.. But I cant imagine that, surely very love and clingy to your job. QUOTE(selinix @ Apr 12 2017, 09:10 PM) 20% enough for other expenses? Depends on the total net income, haha. Bank got their bracket I think, if above 20k can loan up to 90%.QUOTE(Nikmon @ Apr 12 2017, 09:18 PM) if you want to gauge how many rich and poor pp in this forum, than your poll's question is make sense. True, Thanks sifu for clarifying. I should have asked more specifically. To qualify for 60% and above, I think net income need to be at least 5k and above.. correct me if I am wrong.60% is affordable for high income but not low income. QUOTE(-/00\- @ Apr 12 2017, 09:22 PM) i believe in work hard now relax later.. first few year is abit harder but at least at later age we can relax more.. if we dint give a go now with high commitments, then few years later our life will be more difficult.. I totally agree on this. Too relax-ed when you are young, sure tough life awaits when you grow older, when you have more commitments creeping in. Wife, kids, insurance, parents, etc. |

|

|

Apr 12 2017, 09:51 PM

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(intoxicat @ Apr 12 2017, 09:28 PM) This is a very subjective question, if your annual income is like Lim Kok Thay, then you can well afford to spend more than 60% of your income on a home loan, as the balance income (after minus the home loan) is still tens of millions, and a small fraction of this is sufficient for you to sustain your living expenses. But my friends and I myself, managed to secure up to 70% of loan to our net income. It is kind of odd, I am kind of worried too whether should go for it or not. Apparently banks are still approving loan installment of 60-70% of income.On the other hand, if you income is 2k a month, if you pay 60% for home loan, the balance income is hardly sufficient to sustain a living. In any event, please note that Bank Negara only allows around 30%-40% of one's income for payment of home loan, so even if you wish to use 60% of your income to pay your home loan, no bank will agree to this. QUOTE(heavensea @ Apr 12 2017, 09:39 PM) imno, You are right, even the most stable job also can crumble down. Everything comes with a risk. What about you? Do you put 50% and less of your net income into housing loan?everyone have to anticipate adverse future such as retrenchment, losing ability to work (touch wood) and etc. don't say 60%, 50% also considered risky as putting own-self in the edge of cliff already; especially in current malai bole land economy/market which is bleak like Death Metal music. |

|

|

Apr 12 2017, 09:54 PM

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(David_77 @ Apr 12 2017, 09:48 PM) FAMA fund leh 😂 QUOTE(Tankimher @ Apr 12 2017, 09:50 PM) Hahahhaa his life is my dream You'll be surprised.. my banker told me he dealt with many 20+ years old kids.. but buy 800k house... FAMA got alot of FD .. Got some case they actually put in 70-80% or more of the loan amount into flexi account, and pay monthly instalment just ngam ngam 3 years to escape from lock in periodThis post has been edited by Michaelbyz23: Apr 12 2017, 09:54 PM |

|

|

Apr 12 2017, 10:00 PM

|

|

Senior Member

3,838 posts Joined: Sep 2013 |

QUOTE(Michaelbyz23 @ Apr 12 2017, 09:54 PM) You'll be surprised.. my banker told me he dealt with many 20+ years old kids.. but buy 800k house... FAMA got alot of FD .. Got some case they actually put in 70-80% or more of the loan amount into flexi account, and pay monthly instalment just ngam ngam 3 years to escape from lock in period QUOTE(Tankimher @ Apr 12 2017, 09:57 PM) Duit bapa boleh la haha whats wrong with an 20+yr old buying 800k property on their own? jeli? |

|

|

Apr 12 2017, 10:04 PM

|

|

Junior Member

372 posts Joined: Nov 2012 |

My house is 36% and car is 14% of my nett income (both acquire this year) Young and single, but also dont dare to press the pedal too hard

|

|

|

Apr 12 2017, 10:04 PM

|

All Stars

13,761 posts Joined: Jun 2011 |

Some bizmen able to do above mof 100%

|

|

|

Apr 12 2017, 10:06 PM

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(IVL @ Apr 12 2017, 10:04 PM) My house is 36% and car is 14% of my nett income (both acquire this year) Young and single, but also dont dare to press the pedal too hard Good job bro, Nowadays not easy to press below 50% considering the fact that salary has been stagnating and house prices go up like crazy. |

|

|

Apr 12 2017, 10:08 PM

|

All Stars

12,528 posts Joined: Feb 2013 |

QUOTE(HarpArtist @ Apr 12 2017, 08:00 AM) whats wrong with an 20+yr old buying 800k property on their own? jeli? +1. i know under 25 yr olds with 1.5mil+ portftolio all on their own. not everyone depend on fama la  |

|

|

Apr 12 2017, 10:09 PM

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(Babizz @ Apr 12 2017, 10:08 PM) +1. i know under 25 yr olds with 1.5mil+ portftolio all on their own. not everyone depend on fama la Salute the successful person! |

|

|

Apr 12 2017, 10:21 PM

|

|

Senior Member

9,616 posts Joined: Dec 2013 |

QUOTE(Michaelbyz23 @ Apr 12 2017, 09:51 PM) But my friends and I myself, managed to secure up to 70% of loan to our net income. It is kind of odd, I am kind of worried too whether should go for it or not. Apparently banks are still approving loan installment of 60-70% of income. Total commitments>50%You are right, even the most stable job also can crumble down. Everything comes with a risk. What about you? Do you put 50% and less of your net income into housing loan? |

|

|

Apr 12 2017, 10:28 PM

|

|

Senior Member

1,416 posts Joined: Feb 2015 |

QUOTE(Tankimher @ Apr 12 2017, 08:46 PM) Don't talk cock laaaaa monthly income 3k FD 500k zzzz Really got this kind of person..parent left one house and 500k cash for her but income only 3k |

|

|

Apr 12 2017, 10:31 PM

|

Junior Member

867 posts Joined: Feb 2017 |

question, if u go for conventional loan 35 years. if u got money and repay it within 20 years. do you get a lot of deduction?

|

|

|

Apr 12 2017, 10:35 PM

|

Senior Member

9,913 posts Joined: Jun 2014 |

QUOTE(ManutdGiggs @ Apr 12 2017, 10:04 PM) Some bizmen able to do above mof 100% Hehe... biz men have lines of credit leh... |

|

|

Apr 12 2017, 10:39 PM

|

|

Junior Member

443 posts Joined: Jul 2016 |

QUOTE(Babizz @ Apr 12 2017, 10:08 PM) +1. i know under 25 yr olds with 1.5mil+ portftolio all on their own. not everyone depend on fama la many. some under 30 own 10millions |

|

|

Apr 12 2017, 10:40 PM

|

|

Senior Member

2,396 posts Joined: Aug 2016 |

QUOTE(planc @ Apr 12 2017, 10:28 PM) Really got this kind of person..parent left one house and 500k cash for her but income only 3k Serious? Wow! 😳 |

|

|

Apr 12 2017, 10:41 PM

|

|

Junior Member

443 posts Joined: Jul 2016 |

QUOTE(HarpArtist @ Apr 12 2017, 10:00 PM) whats wrong with an 20+yr old buying 800k property on their own? jeli? you are also one of them, nothing to surprise |

|

|

Apr 12 2017, 10:45 PM

|

|

Junior Member

372 posts Joined: Nov 2012 |

QUOTE(Michaelbyz23 @ Apr 12 2017, 10:06 PM) Good job bro, Yeah salary stagnating +1 Nowadays not easy to press below 50% considering the fact that salary has been stagnating and house prices go up like crazy. Lucky for me paying 11% (progressive int.) only out of the 36% at the monent. |

|

|

Apr 12 2017, 10:49 PM

|

Junior Member

130 posts Joined: Jul 2011 From: Pandan Indah/KLIA |

In the past 4 month, i spend over 100% of my income. FML.

|

|

|

Apr 12 2017, 10:53 PM

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(IVL @ Apr 12 2017, 10:45 PM) Yeah salary stagnating +1 Yea, still manageable. Still got roughly 2.5 years ahead before paying full amount right? I opt for 100% full installment payment straight away. Sakit..Lucky for me paying 11% (progressive int.) only out of the 36% at the monent. QUOTE(akemwarhead @ Apr 12 2017, 10:49 PM) In the past 4 month, i spend over 100% of my income. FML. Spent on mortgage? |

|

|

Apr 12 2017, 10:55 PM

|

|

Junior Member

372 posts Joined: Nov 2012 |

QUOTE(Michaelbyz23 @ Apr 12 2017, 10:53 PM) Yea, still manageable. Still got roughly 2.5 years ahead before paying full amount right? I opt for 100% full installment payment straight away. Sakit.. Around there, 2-2.5yrs more to VP i reckon. Spent on mortgage? Good for you to reduce on interest amount. |

|

|

Apr 12 2017, 11:00 PM

|

|

Junior Member

130 posts Joined: Jul 2011 From: Pandan Indah/KLIA |

QUOTE(Michaelbyz23 @ Apr 12 2017, 10:53 PM) Yea, still manageable. Still got roughly 2.5 years ahead before paying full amount right? I opt for 100% full installment payment straight away. Sakit.. Im so sad when I read this post, people can ask whether spend 60% of their income on property, with my income right now, i dont even have the allocation for it. Need to find better job and side income. Spent on mortgage? For TS question, if you could afford it, why not, it's a good investment. |

|

|

Apr 12 2017, 11:01 PM

|

Senior Member

845 posts Joined: Apr 2010 From: Sri Petaling |

Mine 43% housing loan + 11% car loan

|

|

|

Apr 12 2017, 11:03 PM

|

|

Senior Member

2,812 posts Joined: Dec 2011 |

QUOTE(Michaelbyz23 @ Apr 12 2017, 09:51 PM) Haha, you must be earning 20k to qualify for that! no bro, just try makan roti, and steal food from company. Another top earner! Haha.. But I cant imagine that, surely very love and clingy to your job. Depends on the total net income, haha. Bank got their bracket I think, if above 20k can loan up to 90%. True, Thanks sifu for clarifying. I should have asked more specifically. To qualify for 60% and above, I think net income need to be at least 5k and above.. correct me if I am wrong. I totally agree on this. Too relax-ed when you are young, sure tough life awaits when you grow older, when you have more commitments creeping in. Wife, kids, insurance, parents, etc.  |

|

|

Apr 12 2017, 11:19 PM

|

Senior Member

2,094 posts Joined: Apr 2007 |

QUOTE(Michaelbyz23 @ Apr 12 2017, 08:22 PM) As per title, just for the purpose of discussion. Very simple question but yet, has stir up quite some contrasting views and opinions. For me, yes, technically on paper, I’ve more than 70% of my nett employment income for home loan. But at the same time, from this 60% that goes to home loan, I do get back a fair amount of money from the rental generated. The 60% is also spread out among few home loans (few properties).Would you, or are you spending more than 60% of your net income for home loan, and why? How much would your ideal % of income be tucked away for home loan? If I were to consider rental income as part of my total income, then the figure drops to about 50%. Why am I leveraging so much? Isn’t 70% dangerous one might ask? Well, I would still consider myself young (early 30’s) and about to start a family. Rather take the risk (meticulously calculated risk), and hopefully make it big through properties than regretting later in life. So far, things are good. My only worry moving forward is not about having insufficient properties, but rather not being able to further increase this DSR figure of mine which is currently at the 70% level. I have not done the detailed calculations yet, but with a 20% pay rise, I am hoping that I can further push this 70%++ figure to 80%. Noticed that another forummer commented on this thread and told you to close the thread as the topic is irrelevant. The DSR can also be googled up easily. Not sure what is his/her level of involvement or experience in property investment but it pretty much shows that he doesn’t have it both. For seasoned investor who have an impressive portfolio (and also very deep pockets), DSR can go easily cross 60% and way more than that. I’ve known of individuals who have breached the 100% mark. Imagine an individual having a nett worth of RM20mil (properties, securities, cash), borrowing a RM3mil home loan but with a monthly repayment that will clock his/her DSR at 100%. With the right and relevant supporting documents, chances of the home loan getting approved is very high. Of course, this policy differs from bank to bank. Each financial institution have their own risk appetite and evaluate opportunities differently. Anyway, good luck in your investment journey! |

|

|

Apr 12 2017, 11:26 PM

|

|

All Stars

13,761 posts Joined: Jun 2011 |

QUOTE(DrPitchard @ Apr 12 2017, 11:19 PM) Very simple question but yet, has stir up quite some contrasting views and opinions. For me, yes, technically on paper, I’ve more than 70% of my nett employment income for home loan. But at the same time, from this 60% that goes to home loan, I do get back a fair amount of money from the rental generated. The 60% is also spread out among few home loans (few properties). Wah boss u tok till so CHIM u no sked the forumer lipot u n ask mod close tis tered ga 🙊🙊🙊If I were to consider rental income as part of my total income, then the figure drops to about 50%. Why am I leveraging so much? Isn’t 70% dangerous one might ask? Well, I would still consider myself young (early 30’s) and about to start a family. Rather take the risk (meticulously calculated risk), and hopefully make it big through properties than regretting later in life. So far, things are good. My only worry moving forward is not about having insufficient properties, but rather not being able to further increase this DSR figure of mine which is currently at the 70% level. I have not done the detailed calculations yet, but with a 20% pay rise, I am hoping that I can further push this 70%++ figure to 80%. Noticed that another forummer commented on this thread and told you to close the thread as the topic is irrelevant. The DSR can also be googled up easily. Not sure what is his/her level of involvement or experience in property investment but it pretty much shows that he doesn’t have it both. For seasoned investor who have an impressive portfolio (and also very deep pockets), DSR can go easily cross 60% and way more than that. I’ve known of individuals who have breached the 100% mark. Imagine an individual having a nett worth of RM20mil (properties, securities, cash), borrowing a RM3mil home loan but with a monthly repayment that will clock his/her DSR at 100%. With the right and relevant supporting documents, chances of the home loan getting approved is very high. Of course, this policy differs from bank to bank. Each financial institution have their own risk appetite and evaluate opportunities differently. Anyway, good luck in your investment journey! Anw gd sharing fr many sifu here. |

|

|

Apr 12 2017, 11:37 PM

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(DrPitchard @ Apr 12 2017, 11:19 PM) Very simple question but yet, has stir up quite some contrasting views and opinions. For me, yes, technically on paper, I’ve more than 70% of my nett employment income for home loan. But at the same time, from this 60% that goes to home loan, I do get back a fair amount of money from the rental generated. The 60% is also spread out among few home loans (few properties). Thank you very much Sifu for your words of encouragement and constructive comment. If I were to consider rental income as part of my total income, then the figure drops to about 50%. Why am I leveraging so much? Isn’t 70% dangerous one might ask? Well, I would still consider myself young (early 30’s) and about to start a family. Rather take the risk (meticulously calculated risk), and hopefully make it big through properties than regretting later in life. So far, things are good. My only worry moving forward is not about having insufficient properties, but rather not being able to further increase this DSR figure of mine which is currently at the 70% level. I have not done the detailed calculations yet, but with a 20% pay rise, I am hoping that I can further push this 70%++ figure to 80%. Noticed that another forummer commented on this thread and told you to close the thread as the topic is irrelevant. The DSR can also be googled up easily. Not sure what is his/her level of involvement or experience in property investment but it pretty much shows that he doesn’t have it both. For seasoned investor who have an impressive portfolio (and also very deep pockets), DSR can go easily cross 60% and way more than that. I’ve known of individuals who have breached the 100% mark. Imagine an individual having a nett worth of RM20mil (properties, securities, cash), borrowing a RM3mil home loan but with a monthly repayment that will clock his/her DSR at 100%. With the right and relevant supporting documents, chances of the home loan getting approved is very high. Of course, this policy differs from bank to bank. Each financial institution have their own risk appetite and evaluate opportunities differently. Anyway, good luck in your investment journey!  Really exciting journey ahead awaits, lots of homeworks need to be done, and assess on risks as well. I've decided to put 60% of net income into mortgage, I'd rather take the calculated risk, than regret later too. |

|

|

Apr 12 2017, 11:38 PM

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(akemwarhead @ Apr 12 2017, 11:00 PM) Im so sad when I read this post, people can ask whether spend 60% of their income on property, with my income right now, i dont even have the allocation for it. Need to find better job and side income. Don't worry, you will find you way there one day bro. Abit of luck and hard work, keep finding! For TS question, if you could afford it, why not, it's a good investment. Patience is important. Channel your energy into good use |

|

|

Apr 13 2017, 12:06 AM

|

|

Senior Member

2,094 posts Joined: Apr 2007 |

QUOTE(akemwarhead @ Apr 12 2017, 11:00 PM) Im so sad when I read this post, people can ask whether spend 60% of their income on property, with my income right now, i dont even have the allocation for it. Need to find better job and side income. How one looks at it depends very much on the situation that they are in. If part of the money goes to supporting the family, a small chunk to insurance, a fair bit goes to charity bodies and some to servicing education loans, then the actual scenario isn't so bad after all.For TS question, if you could afford it, why not, it's a good investment. Rather decent I would say. |

|

|

Apr 13 2017, 12:20 AM

|

|

All Stars

20,146 posts Joined: May 2011 |

QUOTE(heavensea @ Apr 12 2017, 09:39 PM) imno, Like someone saideveryone have to anticipate adverse future such as retrenchment, losing ability to work (touch wood) and etc. don't say 60%, 50% also considered risky as putting own-self in the edge of cliff already; especially in current malai bole land economy/market which is bleak like Death Metal music. Love your job Love your boss Love your opis and Love your wifey |

|

|

Apr 13 2017, 12:25 AM

|

Senior Member

3,312 posts Joined: Dec 2010 |

QUOTE(DrPitchard @ Apr 12 2017, 11:19 PM) Very simple question but yet, has stir up quite some contrasting views and opinions. For me, yes, technically on paper, I’ve more than 70% of my nett employment income for home loan. But at the same time, from this 60% that goes to home loan, I do get back a fair amount of money from the rental generated. The 60% is also spread out among few home loans (few properties). nice sharing bro, like ManU says u no sked the fella report you and close this forum ka? sometime there is a few of those stars alot alot punya and like to showoff i dont understand why. @@ If I were to consider rental income as part of my total income, then the figure drops to about 50%. Why am I leveraging so much? Isn’t 70% dangerous one might ask? Well, I would still consider myself young (early 30’s) and about to start a family. Rather take the risk (meticulously calculated risk), and hopefully make it big through properties than regretting later in life. So far, things are good. My only worry moving forward is not about having insufficient properties, but rather not being able to further increase this DSR figure of mine which is currently at the 70% level. I have not done the detailed calculations yet, but with a 20% pay rise, I am hoping that I can further push this 70%++ figure to 80%. Noticed that another forummer commented on this thread and told you to close the thread as the topic is irrelevant. The DSR can also be googled up easily. Not sure what is his/her level of involvement or experience in property investment but it pretty much shows that he doesn’t have it both. For seasoned investor who have an impressive portfolio (and also very deep pockets), DSR can go easily cross 60% and way more than that. I’ve known of individuals who have breached the 100% mark. Imagine an individual having a nett worth of RM20mil (properties, securities, cash), borrowing a RM3mil home loan but with a monthly repayment that will clock his/her DSR at 100%. With the right and relevant supporting documents, chances of the home loan getting approved is very high. Of course, this policy differs from bank to bank. Each financial institution have their own risk appetite and evaluate opportunities differently. Anyway, good luck in your investment journey! on a side note this is a very beautiful insight! |

|

|

Apr 13 2017, 12:29 AM

|

|

All Stars

20,146 posts Joined: May 2011 |

QUOTE(planc @ Apr 12 2017, 09:41 PM) What if monthly income RM3000 but have FD 500k and use the interest to pay housing loan? U will be assessed under net worth category Probably the bank will need tou to pledge fd against the housing loan. |

|

|

Apr 13 2017, 12:31 AM

|

|

All Stars

20,146 posts Joined: May 2011 |

QUOTE(Tankimher @ Apr 12 2017, 09:46 PM) Don't talk cock laaaaa monthly income 3k FD 500k zzzz InheritageRetired individuals Insurance payout. Windfall Illegal activities. |

|

|

Apr 13 2017, 12:43 AM

|

All Stars

21,457 posts Joined: Jul 2012 |

Elevated dsr is vulnerable to bank interest rate rise. In some countries, dsr of over 30% is considered stressed and over 50% is suicidal.

For DSR calculation, should include other regular income else it is not logical to have over 100% DSR. This post has been edited by icemanfx: Apr 13 2017, 09:02 AM |

|

|

Apr 13 2017, 09:16 AM

Show posts by this member only | IPv6 | Post

#54

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(BEANCOUNTER @ Apr 13 2017, 12:29 AM) U will be assessed under net worth category Yea. But my banker friend also said nowadays FD means nothing..They will not take it into consideration when approving loan, cuz you can run anytime with FD. Unless you put big downpayment?Probably the bank will need tou to pledge fd against the housing loan. |

|

|

Apr 13 2017, 09:28 AM

|

Senior Member

4,998 posts Joined: Dec 2010 |

Another useless poll thread

|

|

|

Apr 13 2017, 09:32 AM

|

|

All Stars

21,457 posts Joined: Jul 2012 |

QUOTE(Michaelbyz23 @ Apr 13 2017, 09:16 AM) Yea. But my banker friend also said nowadays FD means nothing..They will not take it into consideration when approving loan, cuz you can run anytime with FD. Unless you put big downpayment? Bank could tell borrower to pledge FD as collateral.According to bnm, only about 6% of people have saving to support over 6 months of living expenses mean only a minority have substantial FD. |

|

|

Apr 13 2017, 09:33 AM

|

All Stars

10,188 posts Joined: Apr 2012 |

used to be 60% two years ago.... now already gone way below that.... so its either you improve your income or you dont get one.... especially nowadays millennial salary vs house price...

|

|

|

Apr 13 2017, 09:56 AM

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(icemanfx @ Apr 13 2017, 09:32 AM) Bank could tell borrower to pledge FD as collateral. I see. Btw just wondering, when they say 6 months of living expenses savings, they mean 6 months of savings equivalent to 6 months of income right?According to bnm, only about 6% of people have saving to support over 6 months of living expenses mean only a minority have substantial FD. QUOTE(aaron1717 @ Apr 13 2017, 09:33 AM) used to be 60% two years ago.... now already gone way below that.... so its either you improve your income or you dont get one.... especially nowadays millennial salary vs house price... Yea, imagine the way forward, salary will stagnant, and price of houses go way up. 10 years ago, and today, the basic salary hasnt really changed much. |

|

|

Apr 13 2017, 10:22 AM

|

|

All Stars

10,188 posts Joined: Apr 2012 |

QUOTE(Michaelbyz23 @ Apr 13 2017, 09:56 AM) I see. Btw just wondering, when they say 6 months of living expenses savings, they mean 6 months of savings equivalent to 6 months of income right? salary may stagnant... but u have to work harder now... compare to last time when one job able to get you house and car and still can spend on life... but then most of the millennials now... YOLO all the way... so they wont work anything more than they think the should... just 9-6pm work... and done... YOLO all the way.... for those with family is understandable... thats why must work super hard before u have a family of your own....Yea, imagine the way forward, salary will stagnant, and price of houses go way up. 10 years ago, and today, the basic salary hasnt really changed much. generally for me now is that i must have 6 months worth of my monthly income now.... lets say now u having 5k nett per mth... make sure u have 30k savings in your bank acc at least... This post has been edited by aaron1717: Apr 13 2017, 10:23 AM |

|

|

Apr 13 2017, 11:13 AM

|

All Stars

14,082 posts Joined: Aug 2009 From: Malaysia |

QUOTE(aaron1717 @ Apr 13 2017, 10:22 AM) salary may stagnant... but u have to work harder now... compare to last time when one job able to get you house and car and still can spend on life... but then most of the millennials now... YOLO all the way... so they wont work anything more than they think the should... just 9-6pm work... and done... YOLO all the way.... for those with family is understandable... thats why must work super hard before u have a family of your own.... Uptown punya boss sudah spoken.generally for me now is that i must have 6 months worth of my monthly income now.... lets say now u having 5k nett per mth... make sure u have 30k savings in your bank acc at least... Problem is people always buy into hype believing it's a good investment while they themselves did not take the effort to study the idea of the project or etc. Later when VP time kenot flip, then emo Liao. Cash flow stuck on a stagnant piece of property. Time to earn more. |

|

|

Apr 13 2017, 11:17 AM

|

|

Senior Member

1,263 posts Joined: Oct 2016 |

For me currently was 12% house loan & 14% car loan. However recently bought new launched property which would wiped out additional 44% of my net salary. However consider that the property will only complete in 3-4years time hope my salary can cope up to reduce the ratio. And currently rental income was 11% of nett income.

|

|

|

Apr 13 2017, 11:17 AM

|

|

All Stars

10,188 posts Joined: Apr 2012 |

QUOTE(chiahau @ Apr 13 2017, 11:13 AM) Uptown punya boss sudah spoken. sapa boss sini.... sakit weh... lol.....Problem is people always buy into hype believing it's a good investment while they themselves did not take the effort to study the idea of the project or etc. Later when VP time kenot flip, then emo Liao. Cash flow stuck on a stagnant piece of property. Time to earn more. yeah... generally hype is everywhere... and most of them lazy to do some studies and research... if you ask me those who queue for those AK projects... mostly buy into the hype and the pricing.... and parents outdated knowledge + agent smooth talking add on to it.... and flipping... now is rolling... no such thing to flip upon VP nowadays... u have to roll till certain period only ur body is fully terbalik....  |

|

|

Apr 13 2017, 11:20 AM

|

|

Senior Member

1,263 posts Joined: Oct 2016 |

QUOTE(aaron1717 @ Apr 13 2017, 11:17 AM) sapa boss sini.... sakit weh... lol..... Sorry what is AK projects? Noob hereyeah... generally hype is everywhere... and most of them lazy to do some studies and research... if you ask me those who queue for those AK projects mostly buy into the hype and the pricing.... and parents outdated knowledge + agent smooth talking add on to it.... and flipping... now is rolling... no such thing to flip upon VP nowadays... u have to roll till certain period only ur body is fully terbalik.... This post has been edited by Rinth: Apr 13 2017, 11:21 AM |

|

|

Apr 13 2017, 11:21 AM

|

All Stars

23,688 posts Joined: Aug 2007 From: Outer Space |

some banks offering DSR up to 75%.

so yes, you can take use up your full 75% DSR for home loan only. |

|

|

Apr 13 2017, 11:21 AM

|

|

All Stars

14,082 posts Joined: Aug 2009 From: Malaysia |

QUOTE(aaron1717 @ Apr 13 2017, 11:17 AM) sapa boss sini.... sakit weh... lol..... Wa make fun of AK.yeah... generally hype is everywhere... and most of them lazy to do some studies and research... if you ask me those who queue for those AK projects... mostly buy into the hype and the pricing.... and parents outdated knowledge + agent smooth talking add on to it.... and flipping... now is rolling... no such thing to flip upon VP nowadays... u have to roll till certain period only ur body is fully terbalik.... Very dangerous line sia. Nanti kena tangkap and bash. AK king of affordable housing to help ppl |

|

|

Apr 13 2017, 11:28 AM

|

|

All Stars

10,188 posts Joined: Apr 2012 |

QUOTE(Rinth @ Apr 13 2017, 11:20 AM) Sorry what is AK projects? Noob here aset kayamas |

|

|

Apr 13 2017, 11:30 AM

|

|

All Stars

10,188 posts Joined: Apr 2012 |

QUOTE(chiahau @ Apr 13 2017, 11:21 AM) Wa make fun of AK. no la.. for own stay... they are definitely good to go ahead.... but more than 50% is investors... flippers.... they king of affordable housing meant for those to stay ma... haha.... but many buy for flip... for rental.... Very dangerous line sia. Nanti kena tangkap and bash. AK king of affordable housing to help ppl parents say dont own one now... cant own in the future... even dont stay also can rent ma.... so positive... |

|

|

Apr 13 2017, 11:40 AM

Show posts by this member only | IPv6 | Post

#68

|

|

Senior Member

2,094 posts Joined: Apr 2007 |

QUOTE(Michaelbyz23 @ Apr 12 2017, 11:37 PM) Thank you very much Sifu for your words of encouragement and constructive comment. Sure, welcome. Feel free to ask if you need any other info. Wealth of knowledge in these forums, but at the same time, lots of empty, rusted tin cans that are rattling quite loud. I'm sure you will be wise enough to filter those out and not let them deter you.Really exciting journey ahead awaits, lots of homeworks need to be done, and assess on risks as well. I've decided to put 60% of net income into mortgage, I'd rather take the calculated risk, than regret later too. All the best! |

|

|

Apr 13 2017, 11:43 AM

|

|

All Stars

14,082 posts Joined: Aug 2009 From: Malaysia |

QUOTE(aaron1717 @ Apr 13 2017, 11:30 AM) no la.. for own stay... they are definitely good to go ahead.... but more than 50% is investors... flippers.... they king of affordable housing meant for those to stay ma... haha.... but many buy for flip... for rental.... Can rent, bleed money only lor parents say dont own one now... cant own in the future... even dont stay also can rent ma.... so positive... Ownstay buy in hutan best. One day hutan become Bandar Utama and you can sell the property for millions Everyone has their own strategy but those who never learn to research first to kaput in few years time.... |

|

|

Apr 13 2017, 11:45 AM

|

|

All Stars

10,188 posts Joined: Apr 2012 |

QUOTE(chiahau @ Apr 13 2017, 11:43 AM) Can rent, bleed money only lor no la... not necessary best la... if u like condo... go city stay ma... alot ppl like condo also.... easier to manage... feel safer.... like the facilities provided.... but in term of appreciation... nothing much to talk about on condo....Ownstay buy in hutan best. One day hutan become Bandar Utama and you can sell the property for millions Everyone has their own strategy but those who never learn to research first to kaput in few years time.... |

|

|

Apr 13 2017, 12:01 PM

|

|

Junior Member

281 posts Joined: Aug 2016 |

Yes I would spend 60% of my nett income to home loan, if got opportunity.

Now 14% home, 12% car and 8% personal. So I have another 26% to spend to another home. |

|

|

Apr 13 2017, 12:47 PM

|

|

Senior Member

4,552 posts Joined: Jun 2009 From: Selangor / Sarawak / New York |

QUOTE(chiahau @ Apr 13 2017, 11:13 AM) Uptown punya boss sudah spoken. Now no dare to flip flip.. buy for own stay Problem is people always buy into hype believing it's a good investment while they themselves did not take the effort to study the idea of the project or etc. Later when VP time kenot flip, then emo Liao. Cash flow stuck on a stagnant piece of property. Time to earn more. QUOTE(Rinth @ Apr 13 2017, 11:17 AM) For me currently was 12% house loan & 14% car loan. However recently bought new launched property which would wiped out additional 44% of my net salary. However consider that the property will only complete in 3-4years time hope my salary can cope up to reduce the ratio. And currently rental income was 11% of nett income. Very well managed, keeping monthly commitment way below 40%. QUOTE(Megatronika @ Apr 13 2017, 12:01 PM) Yes I would spend 60% of my nett income to home loan, if got opportunity. Can start hunting again boss. Now 14% home, 12% car and 8% personal. So I have another 26% to spend to another home.  |

|

|

Apr 13 2017, 04:08 PM

|

|

Senior Member

7,343 posts Joined: May 2005 |

QUOTE(Kicimiao66cc @ Apr 12 2017, 09:21 PM) Enof lo Must be earning 20,000 nett salary, assuming you left 20% which is rm2000 every month for all you other expenses, no car loan i guess. |

|

|

Apr 13 2017, 05:13 PM

|

|

Senior Member

1,359 posts Joined: Aug 2013 |

QUOTE(selinix @ Apr 13 2017, 04:08 PM) Must be earning 20,000 nett salary, assuming you left 20% which is rm2000 every month for all you other expenses, no car loan i guess. 80% property (30% commercial 70% residential) 5% car 5% leisure 10% others expenses + saving. |

|

|

Apr 25 2017, 04:36 PM

|

Senior Member

765 posts Joined: Jan 2016 |

will not spend more than 60%..

This post has been edited by mafa2801: Apr 25 2017, 04:37 PM |

|

|

Apr 26 2017, 05:37 PM

|

Senior Member

888 posts Joined: Mar 2011 |

I will got more than 60% because year by year will get increment in salary and it will fall to maybe 40% of Bert salary goes to home loan. If wait for increment only buy a house the house price increase way faster. Also if I got few 100k saving I will take the risk

|

|

|

Apr 30 2017, 06:07 PM

|

Senior Member

6,562 posts Joined: Jan 2003 From: Kuala Lumpur |

for own stay? not a damn chance.

for investments? for sure, as long as the capital appreciation is good AND/OR rental can cover the installments and other costs |

| Change to: |  0.0558sec 0.0558sec

0.66 0.66

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 15th December 2025 - 05:41 AM |

Quote

Quote