QUOTE(Bonescythe @ Dec 17 2015, 09:45 PM)

Tats why i say u will think i bs you.. but i betul belum even 30..

Ok. We sidebet 6%

If 2016 got 6%, then how ? Haha

Central bank in every country manages the economy through monetary policy to control the money supply in the market. The basic tool used by central bank is through the interest rate. Increase interest rate when there is too much money in the market during the inflation and decrease interest rate when recession to stimulate the economic growth.

However during global financial crisis, in USA, the interest rate is zero percent and hence the conventional monetary policy of playing with interest rate is not effective. QE, quantitative easing policy was used. With confirmed economic growth, FED then only announced increase in the rate.

Domestic wise

Malaysia inflationrate is affected by the GST implemented in April and it has caused a cost push inflation. The ringgit has depreciated and it has increased the cost of input material imported from overseas. Again confirming a cost push inflation scenerio. People will be conservative in spending as future outlook is weak. Rightly, the interest rate should be reduced to encourage more spending.

Internationally, USA as expected raised the rate and this will affect the money supply in Malaysia market. With RM depreciation and US interest rates on the uptrend, the money may flow out of the country, increase the money supply. Interestingly China has offer to buy the Bond from Malaysia. If this is true the money supply through selling the bond to China will increaseve money supply

Oil prices outlook is on the down trend and Petronas has made a loss. This will affect government fiscal policy on spending. Budget 2016 - almost 80% income will be spent on the administration and sustaining. Very little left for spending to stimulate economy.

Tan Sri Zeti will retire in April 2016, judging on current BN ministers quality, my personal opinion is no one is more capable than her. The OPR will be decided by bank negara - her successor and the team.

Based on what I have mentioned above, I do not think 1Q next year will have any increase in OPR unless the US rate increase has caused a large out flow and China is not commiting on buying of Bond.

Malaysia GDP dropped last quarter and it has confirmed the country is experîencing slower economy growth. If the trend persists, interest rate will either maintain in 1Q and may even reduce in 2Q.

This is only my personal opinion and other members are welcome to discuss on the economic outlook.

This post has been edited by gsc: Dec 18 2015, 01:49 AM

Dec 14 2015, 07:52 PM

Dec 14 2015, 07:52 PM

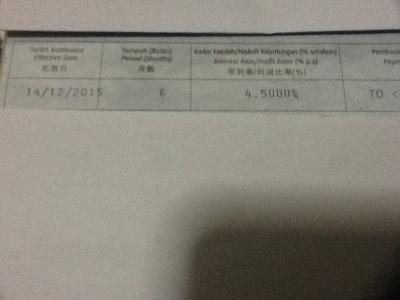

first time a chinaman bank being so generous.

first time a chinaman bank being so generous.

Quote

Quote

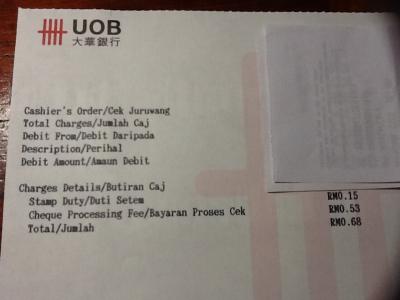

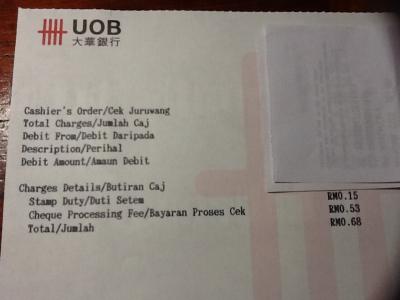

islamic banking is statement based? i tot it depends on bank whether fd statement based or not.

islamic banking is statement based? i tot it depends on bank whether fd statement based or not.

0.0257sec

0.0257sec

0.35

0.35

7 queries

7 queries

GZIP Disabled

GZIP Disabled